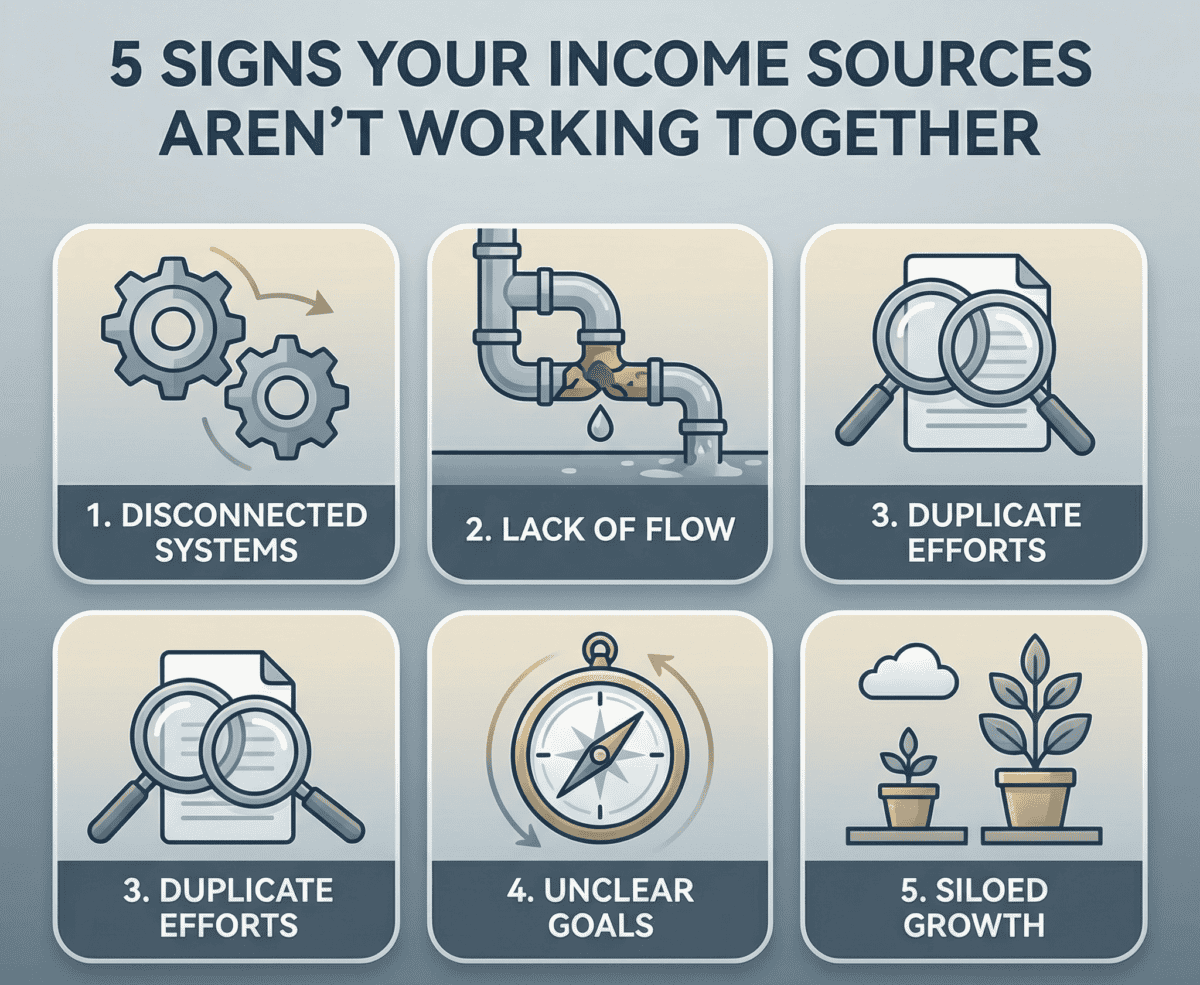

What Your 2025 Tax Return May Be Telling You

Your tax return isn’t just paperwork. It can serve as a report card on how your income sources worked together last year.

Key Takeaways

- One income source can trigger unexpected taxes elsewhere – like IRA withdrawals making more Social Security taxable

- Income swings over ,000 year-to-year may indicate uncoordinated decisions that increase Medicare premiums

- The window between age 59½ and 73 offers low tax rates for strategic Roth conversions

- Tax surprises signal income sources aren’t coordinated – each source’s withholding assumes it’s your only income

- Compare your last three tax returns to spot coordination gaps before they repeat

Most people look at their return and see one number. Either they owe money or they’re getting a refund. Then they file it away and move on.

But your return may be showing you much more than that. It could reveal whether your Social Security, IRA withdrawals, investment gains, and other income sources helped each other or got in each other’s way.

The problem is that most people don’t know what to look for. This article gives you five specific signs. If you see any of them on your 2025 return, your income sources may not be coordinated.

The good news: if you spot these signs now, you have eight months left in 2026 to consider adjustments before similar patterns could repeat.

Why These Signs Matter

Studies on retirement income suggest that how families coordinate their income sources can influence long-term outcomes. Families who coordinate their sources may face different cost patterns than families who manage each source separately.

The difference often isn’t about making better investment choices. It’s about understanding how income sources may interact.

When one source triggers costs in another area, that may indicate a coordination gap. These patterns can show up on your tax return if you know what to look for.

For retirees: These signs may help you understand whether your current approach is working well or whether adjustments could be beneficial. Addressing patterns early may help prevent them from repeating.

For pre-retirees: If you’re 10-15 years from retirement, these signs can show you what patterns to be aware of. The patterns you see on your returns now may continue unless you adjust your approach.

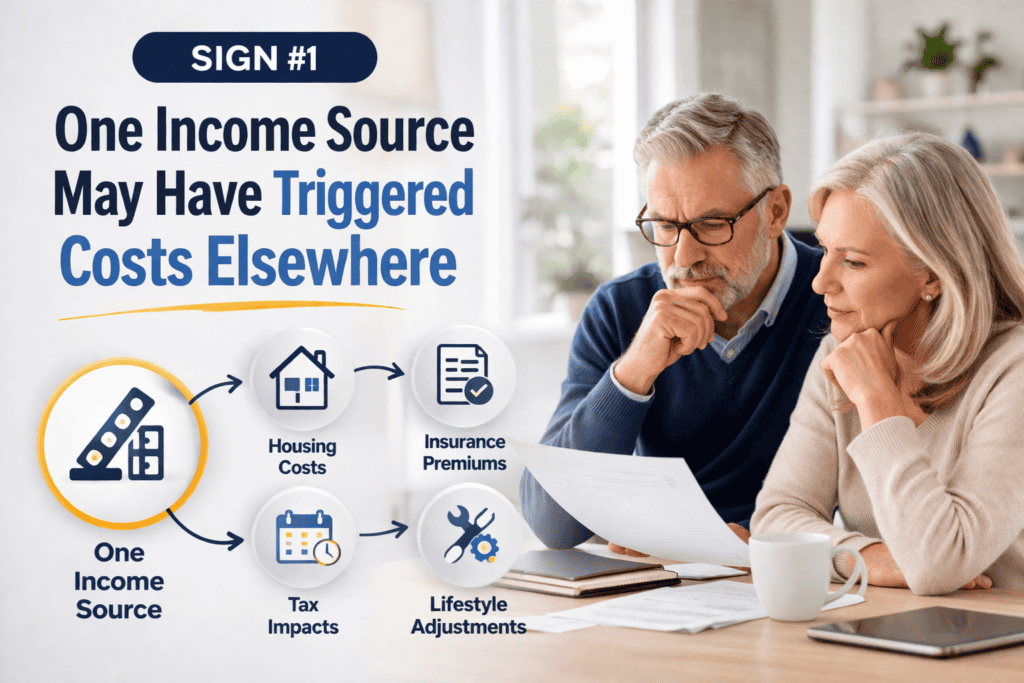

Sign #1: One Income Source May Have Triggered Costs Elsewhere

What to look for:

Compare your 2025 return to your 2024 return. Did more of your Social Security become taxable this year? Did your Medicare premiums increase? Did you move into a higher tax bracket?

If yes, consider what changed. Did you take larger IRA withdrawals? Sell investments? Receive different distribution amounts?

Hypothetical scenario:

Consider a couple with $45,000 in Social Security and $35,000 in other income. Total: $80,000. In this scenario, about 50% of their Social Security might be taxable. They’re in the 12% tax bracket.

They take an additional $15,000 from their IRA for a home repair. The repair is necessary and the decision is reasonable.

However, that $15,000 could push them over a threshold. In this example, 85% of their Social Security might now be taxable instead of 50%. Their taxable income wouldn’t increase by just $15,000. It could increase by approximately $30,750.

That extra $15,750 in taxable income could result in roughly $1,890 in additional federal tax. The IRA withdrawal itself was appropriate for their needs. But the timing and amount may not have been coordinated with their other income sources.

Why this matters:

When one source triggers taxation or surcharges on another source, you may be paying more than necessary. Not because you made an error. Because the pieces may not have been coordinated.

For retirees: If this pattern appeared in 2025, it could repeat in 2026 unless you consider adjustments. You might take the withdrawal from a different source. Or spread it across two years. Or time it differently relative to other income.

For pre-retirees: This is why testing can be valuable. If you’re in your early 60s before required distributions start, you may be able to test how different withdrawal amounts affect Social Security taxation and other costs. This learning may be easier now than after 73 when distributions become mandatory.

Sign #2: Your Income Swings Significantly Year to Year

What to look for:

Review your last three tax returns. Look at your adjusted gross income. Is it within $10,000 each year? Or does it swing by $20,000 or more?

If your income varies significantly without major life changes like retirement, job loss, or selling a business, this may indicate isolated decision-making.

Hypothetical scenario:

Consider a retiree whose income over three years was: 2023 at $65,000, 2024 at $95,000, and 2025 at $70,000.

Why the swing? In 2024, she took a large IRA distribution to purchase a car and took capital gains from rebalancing. Each decision was appropriate for her needs.

But they weren’t coordinated. That high-income year could trigger higher Medicare premiums for 2026 and 2027.

If she had spread those withdrawals and gains across two years, her income might have stayed more stable. Medicare premiums might have stayed lower. Same financial needs met with potentially different cost patterns.

Why this matters:

Volatile income can create volatility in other areas. Tax brackets may change. Medicare premiums may fluctuate.

Social Security taxation may vary. Each year may feel different even though your actual needs stay consistent.

Some research on retirement income patterns suggests that more stable income approaches may be associated with more predictable long-term costs.

For retirees: Consider your spending needs for 2026. If large expenses are coming, think about whether to spread the funding across multiple years or multiple sources rather than taking one large withdrawal from one account.

For pre-retirees: While working, your income is often stable by default. One W-2. When you retire, you’ll have multiple income sources with different timing options. Consider now how you might maintain income consistency even with more complexity.

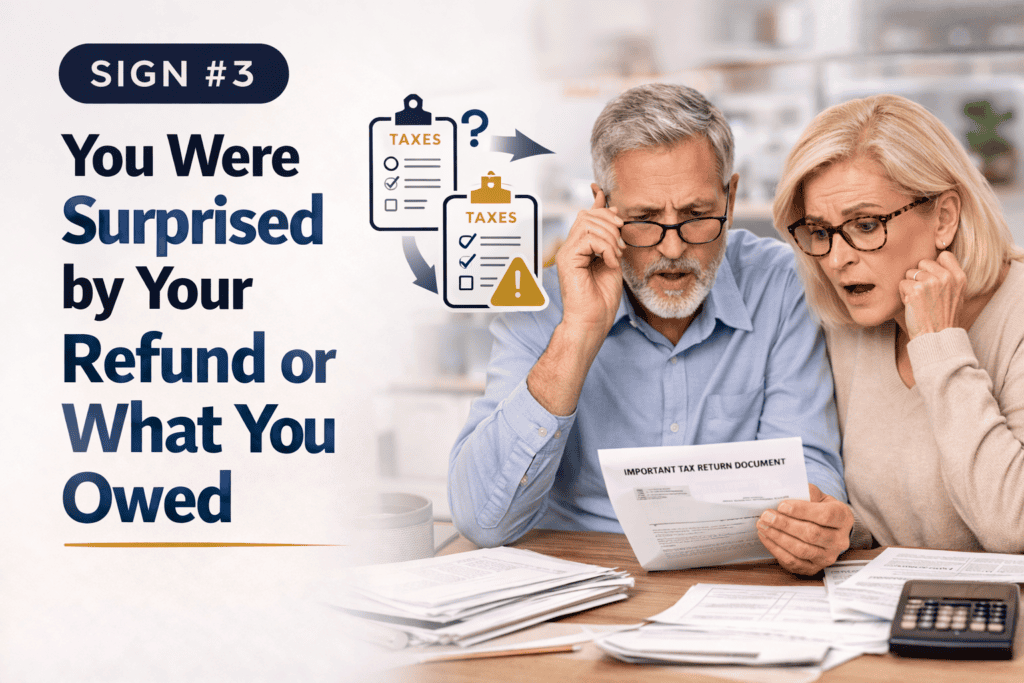

Sign #3: You Were Surprised by Your Refund or What You Owed

What to look for:

Think back to when you finished your return. Were you expecting a refund but owed money? Or expecting to owe but got a refund? Did the amount surprise you?

Significant surprises may mean your withholding and estimated payments didn’t match your actual tax situation. This gap often comes from income sources interacting in unexpected ways.

Hypothetical scenario:

Consider a 66-year-old expecting a small refund. She withholds from her pension. She makes estimated payments on IRA withdrawals. She’s attentive to her taxes.

She files and owes $4,200. Unexpected. What happened?

She sold some stock mid-year to help her daughter. Long-term capital gain of $25,000. That gain pushed more of her Social Security into taxation.

It also moved some income into the 22% bracket. She calculated taxes on the gain itself but didn’t account for how it might affect other income sources.

✓ Wondering if your income sources are coordinated or creating hidden costs? Take our 5-minute Retirement Income Assessment to see how your Social Security, IRAs, and investments stack up—and discover potential coordination gaps while there’s still time to address them.

Why this matters:

Surprises may indicate you’re not seeing how sources interact. You might be calculating each piece separately. Social Security withholding assumes that’s your only income.

IRA withholding assumes that’s your only income. Investment gains get added without adjusting for potential interactions.

For retirees: If you were surprised in 2025, use that as information. Review what actually happened. Consider adjusting your withholding or estimated payments for 2026 based on your actual experience.

For pre-retirees: While working, taxes are straightforward. Employer withholds. You file.

Done. In retirement, you may be managing withholding across multiple sources. This is where surprises can happen.

Learning how withholding works across different account types now may help.

Sign #4: You Manage Each Income Source Separately

What to look for:

This sign isn’t on your return. It’s in your process. Ask yourself: When I decided to take Social Security, did I consider how it might affect IRA withdrawal strategy?

When I took IRA distributions, did I think about Medicare thresholds? When I sold investments, did I consider Social Security taxation?

If the answer is no, you may be managing in isolation. Each decision might be appropriate. But they may not be connected.

Hypothetical scenario:

Consider a couple who delays Social Security to 70 for maximum benefits. Reasonable decision. They take $50,000 annually from IRAs to cover expenses while waiting. Also reasonable.

But they didn’t connect the two decisions. When Social Security starts at 70, their IRA withdrawals might need adjustment. They don’t change their approach.

Total income increases. Tax bracket may increase. Social Security taxation may increase.

Medicare premiums could increase two years later.

Two appropriate decisions that weren’t coordinated with each other.

Why this matters:

Retirement income is a system. Social Security may affect IRA strategy. IRA withdrawals may affect Medicare costs.

Investment gains may affect Social Security taxation. These connections exist whether we plan for them or not.

Studies on financial decision-making suggest that people often optimize individual pieces without considering the whole system.

For retirees: The next time you make a decision about one income source, pause. Ask: How might this affect my other income sources? Could this trigger costs elsewhere? A few minutes of thinking about connections may help prevent unintended consequences.

For pre-retirees: While you’re still working, consider building the habit of systems thinking. If you’re contributing to retirement accounts, think about how those accounts might interact in retirement. If you’re building a taxable investment account, consider how gains might stack with other income later.

Sign #5: You’re in the Low-Income Window But Not Testing Anything

What to look for:

Look at your effective tax rate. Divide your total federal tax by your total income. If you’re between 59½ and 73 and this number is below 12-15%, you may be in what some call the testing window.

Now ask: Am I doing anything strategic with this lower rate? Am I considering Roth conversions? Am I testing different withdrawal approaches? Or am I just taking what I need and nothing more?

Hypothetical scenario:

Consider a 63-year-old who retires with $750,000 in traditional IRAs. She delays Social Security until 67. For four years, she takes $45,000 from taxable accounts to live on.

Her effective tax rate: 7%. She’s in the 12% bracket with room available. She doesn’t take action with her IRAs during this time.

At 67, Social Security starts. At 73, required distributions begin. Her effective rate could increase to 16% or higher. She’s now taking distributions she must take, at rates that may be higher than what she could have managed earlier.

She had four years of lower rates. She didn’t use them strategically.

Why this matters:

The years between retirement and required distributions may offer significant planning flexibility. You can access accounts without penalty. Distributions aren’t mandatory yet. Tax rates are often lower than working years and may be lower than they’ll be after 73.

Some retirement planning research suggests that thoughtful use of this window may influence long-term tax outcomes.

For retirees in this window: If your 2025 return shows a low effective rate and you’re not considering strategic actions, you have eight months left in 2026. Consider whether partial Roth conversions or other strategies might make sense for your situation before this window narrows.

For pre-retirees approaching this window: Understand that this window may exist. It’s not automatic. It may require intentional action. Families who benefit from it often recognize it early and plan accordingly.

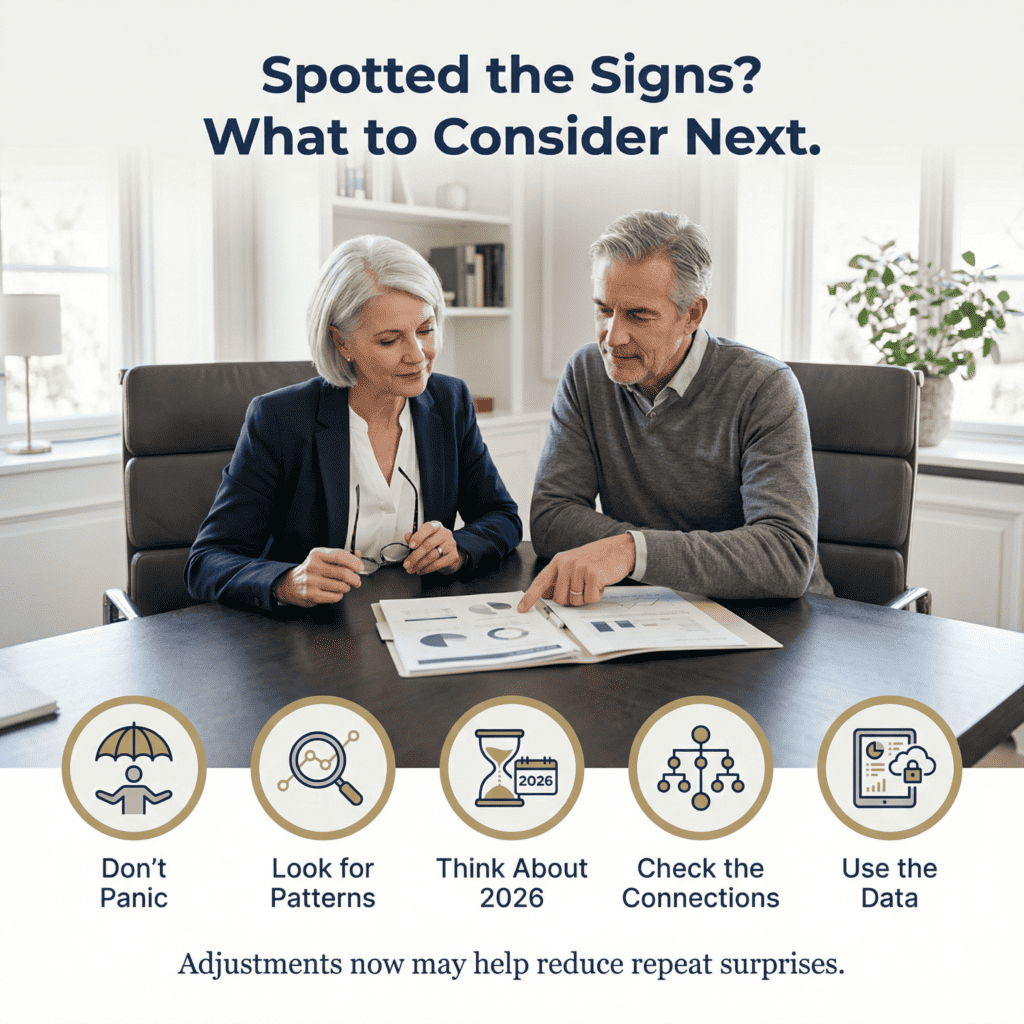

What to Consider If You Spotted Any of These Signs

If you saw one or more of these signs on your 2025 return, it’s not a crisis. It’s information.

📅 Spotted one or more of these signs on your 2025 return? Schedule a 20-minute Income Coordination Review to identify where your sources might be working against each other—and explore strategies to help them work together before patterns repeat in 2026.

Families who navigate retirement well aren’t necessarily the ones who never face coordination challenges. They’re often the ones who spot patterns early and consider adjustments.

Here’s what you might consider:

Don’t panic. Coordination challenges are often addressable. You’re not locked into the pattern.

Look at the pattern, not just one year. If this happened once, it might be situational. If it’s happened multiple years, it may be structural.

Think about 2026 differently. You have eight months remaining. That’s time to consider adjustments to withholding, withdrawal timing, or testing different approaches.

Consider how decisions connect. The next time you make a decision about one income source, pause and think about how it might affect the others.

Your 2025 return showed you what happened when all your income sources came together. If they didn’t work well together, similar patterns could repeat in 2026 unless you consider changes.

The good news: you’re not guessing. You have data. Your return may be showing you exactly where potential coordination gaps exist. That’s a useful starting point.

Thoughtful adjustments now may help reduce the likelihood of these patterns repeating. That’s what coordination can mean. Not perfect planning. Just helping income sources work together rather than creating unintended consequences.

If you spotted multiple signs on your 2025 return, a second opinion conversation may help you understand what’s happening and what adjustments might be worth considering. We help families understand how their income sources may interact and identify potential opportunities to improve coordination while there’s still time and flexibility.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.