When a Trust Is Worth the Cost, When It Is Not, and the Five Questions to Ask Before You Decide

Subscribe to The Confident Retirement Brief for weekly planning insights.

Key Takeaways

- Pennsylvania probate fees are modest (5-1), so fear-based trust sales may not apply to you.

- Pennsylvania probate typically takes 9-18 months, which may or may not justify a trust’s cost.

- Evaluate your specific asset titling and family situation before deciding whether a trust adds real value.

- California and Florida probate horror stories don’t apply to Pennsylvania’s comparatively simpler probate process.

- Ask five specific questions about your assets, titling, and family before paying for a trust.

Do You Actually Need a Trust? A Plain-Language Guide for Pennsylvania Families

At some point, someone told you that you need a trust. Maybe it was a seminar. Maybe it was a well-meaning friend. Maybe it was an attorney who offered to create one.

The question nobody answered clearly was: do you actually need one?

The answer depends on your family, your assets, how those assets are currently titled, and what state you live in. In Pennsylvania, the answer may be different than what you have heard, because Pennsylvania probate works differently than most people assume.

This article walks through the real questions. Not the ones used to sell trusts. The ones that help you decide whether a trust adds genuine value for your specific situation.

What Probate Actually Looks Like in Pennsylvania

Most fear of probate comes from horror stories in other states. California and Florida probate can be expensive and slow. Pennsylvania is different.

Probate in Pennsylvania involves filing with the Register of Wills, notifying heirs and creditors, inventorying assets, paying debts and taxes, and distributing assets. The process typically takes 9 to 18 months, sometimes longer if contested.

Court and administrative fees vary by county but are relatively modest. Filing fees typically range from roughly $175 to $441, depending on the county and estate value. Allegheny County, for example, charges roughly $191 to $441 for estates up to $400,000.

The larger costs come from executor (personal representative) fees and attorney fees. Pennsylvania does not have a fixed statutory fee schedule. Fees must be “reasonable and just” under the law.

However, an informal guideline (sometimes called the Johnson Estate schedule) suggests roughly 5% on the first $100,000, tapering to 0.5% on amounts above $4 million. Attorney fees are often similar, running roughly 3% to 6% of the estate, depending on complexity.

For a relatively simple estate, total probate costs (executor plus attorney) might run roughly 6% of the estate value. For a $200,000 estate, that could mean roughly $12,000 in fees. For a $500,000 estate, roughly $30,000.

Pennsylvania also has a simplified process for small estates. If personal property (not including real estate) is under $50,000, a small estate process may apply, which could avoid formal probate entirely.

What Already Bypasses Probate Without a Trust

This is the section that could save you money. Many of your assets may already avoid probate through the way they are titled or designated.

Jointly held real estate with right of survivorship passes automatically to the surviving owner. No probate required.

Retirement accounts (IRAs, 401(k)s) with named beneficiaries pass directly to the beneficiary. No probate.

Life insurance with named beneficiaries passes directly. No probate.

Bank and brokerage accounts with payable-on-death (POD) or transfer-on-death (TOD) designations pass directly to the named person. No probate.

For many Pennsylvania families, once you account for jointly held property, retirement accounts with beneficiaries, life insurance, and accounts with POD or TOD designations, 80% to 90% of their assets may already bypass probate.

The question then becomes: does the remaining 10% to 20% justify the cost of creating and maintaining a trust?

When a Trust May Be Worth the Cost

For certain families and situations, a trust adds genuine value that proper titling alone cannot provide. Here are the most common situations where a trust may make sense.

Blended families. If you have children from a previous marriage and a current spouse, a trust (such as a QTIP or marital trust) could help ensure your spouse is cared for during their lifetime while protecting your children’s inheritance. Without a trust, a surviving spouse could change beneficiary designations and unintentionally (or intentionally) redirect assets away from stepchildren.

Minor children or grandchildren. Probate gifts to minors typically require court-appointed guardianship until the child turns 18. A trust allows you to set conditions, such as distributing funds at age 25 or in stages. This gives you control over when and how young beneficiaries receive assets.

A family member with special needs. A child or adult with a disability who receives government benefits (Medicaid, SSI) could lose those benefits if they inherit money outright. A special needs trust preserves their eligibility while still providing for their care. Setup costs typically range from $2,000 to $10,000, but the protection is often essential.

Real estate in more than one state. If you own property in Pennsylvania and another state, your estate could face probate in both states (called ancillary probate). A trust that holds both properties avoids this entirely.

Privacy concerns. Probate records are public in Pennsylvania. Anyone can look up the details of an estate that goes through probate. A trust keeps the transfer of assets private.

Incapacity planning. A revocable living trust allows a successor trustee to manage your assets if you become unable to do so, without the need for a court-appointed guardian. This can be faster, less expensive, and less intrusive than the guardianship process.

Medicaid and long-term care planning. An irrevocable Medicaid asset protection trust (IMAPT) may help protect assets from nursing home spend-down. But Pennsylvania imposes a five-year lookback: any assets transferred to such a trust within five years of applying for Medicaid may result in penalties. This means the trust must be funded well in advance. A revocable trust does not provide Medicaid protection because the assets are still considered yours.

When a Trust Probably Is Not Needed

This is the section most trust seminars skip. For many Pennsylvania families, a trust adds cost and complexity without meaningful benefit.

A trust is probably unnecessary if your situation looks like this: you are a married couple where everything passes to the surviving spouse and then equally to adult children. Your major assets (home, retirement accounts, life insurance, bank accounts) already have joint titling, beneficiary designations, or POD/TOD designations. You own real estate in only one state.

You have no blended family, minor beneficiaries, or special needs considerations. And your estate value is low enough that probate costs would be less than the cost of creating and maintaining a trust.

A revocable living trust in Pennsylvania typically costs $1,500 to $7,000 to create, depending on complexity. For an estate where most assets already bypass probate, the probate costs on the remaining assets may be lower than the trust setup cost.

COST COMPARISON: PROBATE vs. TRUST IN PENNSYLVANIA

$50,000 estate: Estimated probate fees roughly $1,500 to $3,000. Trust setup cost roughly $5,000. Probate is likely less expensive.

$200,000 estate: Estimated probate fees roughly $6,000 to $12,000. Trust setup roughly $5,000. Trust may begin to pay off.

$500,000 estate: Estimated probate fees roughly $15,000 to $30,000. Trust setup roughly $5,000. Trust likely saves $10,000 to $25,000.

Wondering if a trust actually makes sense for your Pennsylvania family? Skip the guesswork — schedule a conversation with Langan Financial Group to review your specific assets, titling, and goals before spending money on estate planning you may not need.

$1,000,000 estate: Estimated probate fees roughly $30,000 to $60,000. Trust setup roughly $5,000. Trust is strongly cost-effective.

These figures are illustrative and assume assets subject to full probate. Actual costs vary by complexity, executor choices, and whether assets already bypass probate. Calculations assume combined executor and attorney fees of roughly 3% to 6% of estate value.

The important thing to notice: these estimates assume all assets go through probate. If 80% of your assets already bypass probate through titling and designations, the actual probate cost applies only to the remaining 20%. A $500,000 estate where $400,000 bypasses probate may have only $100,000 subject to probate fees, bringing the cost down to roughly $3,000 to $6,000, which may be less than creating a trust.

What About Pennsylvania’s Inheritance Tax?

Pennsylvania does not have an estate tax (it phased out in 2005). But it does have an inheritance tax, and the rates depend on who receives the assets.

Transfers to a surviving spouse: 0%. No tax. Joint property passing to a surviving spouse is generally exempt.

Transfers to children and grandchildren (lineal heirs): 4.5%.

Transfers to siblings: 12%.

Transfers to other beneficiaries (nieces, nephews, friends): 15%.

A revocable living trust does not avoid the Pennsylvania inheritance tax. The assets are still considered yours during your lifetime, and the tax applies regardless of whether they pass through probate or through a trust. However, executor fees, attorney fees, and debts of the estate are deductible before computing the inheritance tax.

Federally, the 2026 estate and gift tax exemption is $15,000,000 per person. The annual gift exclusion is $19,000 per person per year. For the vast majority of Pennsylvania families, federal estate tax is not a factor.

The Ongoing Costs of Maintaining a Trust

Creating a trust is not a one-time event. There are ongoing responsibilities.

If you name a professional or bank as trustee, they typically charge 1% to 2% of trust assets per year. Even a family member serving as trustee has responsibilities and may expect compensation.

Irrevocable trusts must file a separate IRS Form 1041 if gross income exceeds $600. Trust tax brackets are compressed: the top 37% federal rate kicks in at only $14,650 of undistributed trust income. Pennsylvania taxes trust income similarly to individual income.

There may also be costs for annual accountings, record-keeping, and the critical step most people forget: funding the trust. A trust only avoids probate for assets that are actually transferred into it. An unfunded trust (one where accounts were never retitled in the trust’s name) provides no probate benefit at all.

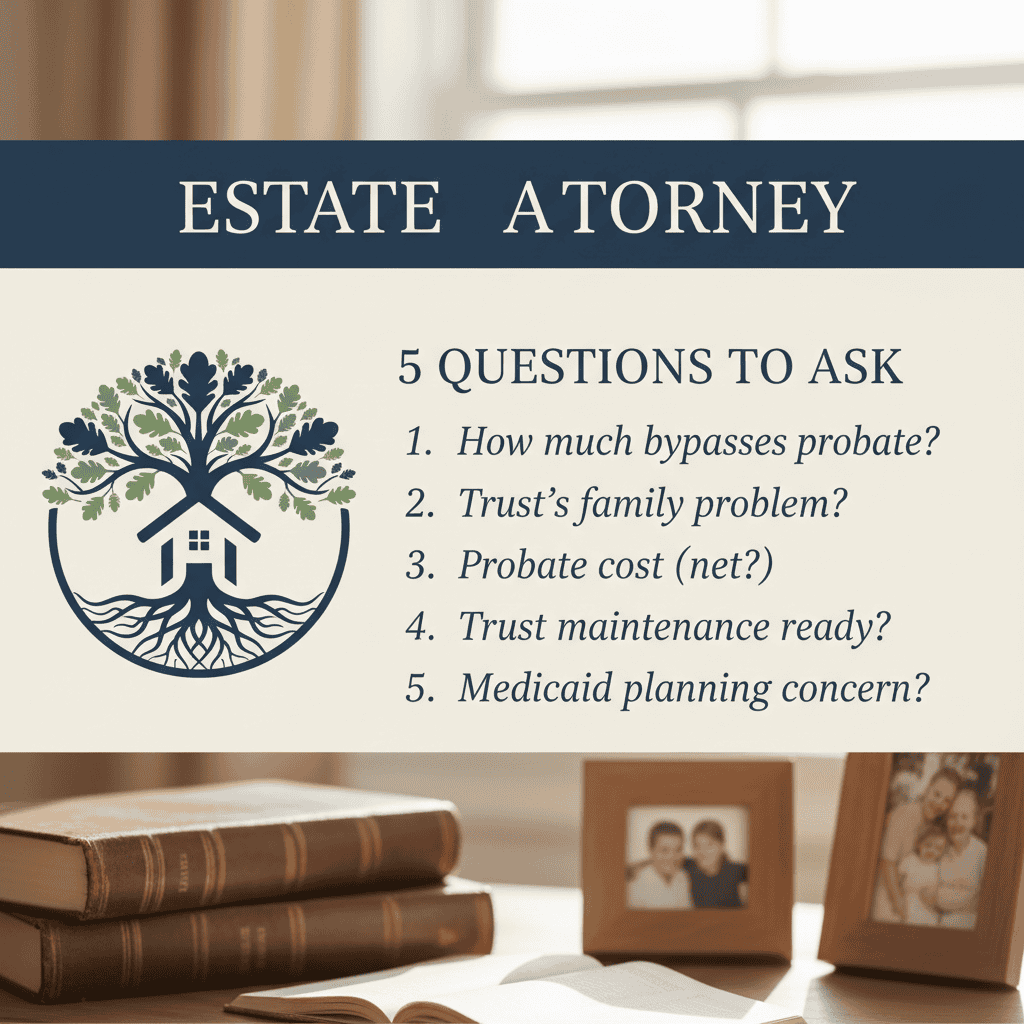

Five Questions to Ask Before Meeting With an Estate Attorney

If you are considering a trust, these five questions can help you walk into the meeting informed rather than sold.

1. How much of my estate already bypasses probate? Make a list of every major asset and note whether it has a beneficiary designation, is jointly titled, or has a POD/TOD designation. If most of your assets already avoid probate, the cost-benefit calculation for a trust changes significantly.

2. What specific problem would a trust solve for my family? “Avoiding probate” is a benefit, but it may not be the most important one. If you have a blended family, minor heirs, a special needs beneficiary, or multi-state property, those are specific problems a trust addresses. If none of those apply, the answer may be that a trust is not needed.

3. What would probate actually cost for my estate, given what already bypasses it? Ask the attorney to estimate probate costs on only the assets that would go through probate, not the full estate. Compare that to the cost of creating and maintaining a trust.

4. Am I prepared for the ongoing maintenance a trust requires? Retitling assets, filing trust tax returns, keeping records, and updating the trust when circumstances change are all ongoing responsibilities. If those feel manageable, a trust may work. If they feel burdensome, the trust could go unfunded and provide no benefit.

5. Is Medicaid planning a concern for our family? If nursing home costs or long-term care are a concern, understand that a revocable trust does not protect assets from Medicaid spend-down. Only an irrevocable trust, funded at least five years before applying, may help. This requires planning well in advance and involves tradeoffs (you give up control of the assets).

The Bottom Line on Trusts for Pennsylvania Families

A trust is a useful tool for certain situations. It is not the right answer for everyone.

If your estate is simple, your assets are properly titled, and your beneficiary designations are current, a well-drafted will and a regular review of your designations may be all you need.

If your family is blended, your heirs include minors or individuals with special needs, you own property in multiple states, or long-term care is a concern, a trust may add real value worth the cost.

The best approach is to understand your own situation first. Our free Trust Decision Guide for Pennsylvania Families walks you through an asset inventory, a situation checklist, and a cost comparison so you can evaluate this clearly before spending time or money on legal consultations.

And regardless of whether you need a trust, every family needs current beneficiary designations, a durable power of attorney, a healthcare directive, and a will. Those documents cost far less than a trust and cover the needs that matter most.

Worth Sharing

If you know someone who was told they need a trust and is not sure whether that is true, this article may help them evaluate the decision clearly. Forward it or share the link.

Not Sure Whether a Trust Makes Sense for You?

We help families evaluate their estate structure as part of a coordinated retirement plan. No cost. No obligation. No pressure to create legal documents you may not need.

Schedule a Complimentary Conversation

Curious how Pennsylvania probate might affect your estate plan? Subscribe to The Confident Retirement Brief and get weekly plain-language insights to help you make smarter, more confident planning decisions — on your terms.

717-288-1880

Related: The Retirement Plan That Works for Two People But Breaks for One

Subscribe to The Confident Retirement Brief for weekly planning insights.

About Langan Financial Group

Langan Financial Group provides personalized retirement planning, investment management, and income coordination for individuals and families in central Pennsylvania and beyond. Located at 1863 Center St., Camp Hill, PA 17011. langanfinancialgroup.com/get-started-today | 717-288-1880

DISCLOSURE: This article is provided for informational and educational purposes only and does not constitute investment advice, financial planning advice, tax advice, or legal advice. Trust and estate planning decisions should be made in consultation with a qualified estate planning attorney and tax professional. Langan Financial Group does not provide legal services and does not draft trust or estate documents.

All cost estimates are approximate and based on published ranges for Pennsylvania as of 2026. Actual costs vary by estate complexity, county, and attorney. Pennsylvania inheritance tax rates, federal estate tax exemptions, and Medicaid rules referenced are current as of 2026 and subject to change by legislation.

The five-year Medicaid lookback period referenced applies to Pennsylvania as of the date of publication. Individual results will vary based on specific circumstances. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC.

Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.