Roth IRA conversions have become one of the most talked-about tax strategies in retirement planning, and for good reason. This powerful tool can potentially save you thousands of dollars in taxes during retirement while providing greater flexibility with your money. However, conversions aren’t right for everyone, and the timing can make a huge difference in the benefits you receive.

Understanding Roth conversions and whether they make sense for your situation could be one of the most valuable financial decisions you make. The strategy involves paying taxes today to avoid potentially higher taxes tomorrow, but the math isn’t always straightforward.

What Is a Roth IRA Conversion?

A Roth IRA conversion involves moving money from a traditional IRA, 401(k), or other tax-deferred retirement account into a Roth IRA. Understanding the key differences between a traditional IRA vs Roth IRA is essential before making any conversion decisions. When you make this conversion, you pay income taxes on the converted amount in the year you do the conversion, but the money then grows tax-free in the Roth IRA.

Unlike traditional retirement accounts, Roth IRAs don’t require you to take minimum distributions during your lifetime. This means your money can continue growing tax-free for as long as you live, and your heirs can inherit the account with significant tax advantages.

The conversion process is relatively simple from a procedural standpoint. You contact your IRA custodian and request the conversion. The converted amount is added to your taxable income for that year, and you pay regular income tax rates on it. There are no penalties for conversions, regardless of your age.

The Tax Benefits of Roth Conversions

The primary benefit of Roth conversions is implementing tax diversification strategies in retirement. Most people have the majority of their retirement savings in tax-deferred accounts like 401(k)s and traditional IRAs. This means every dollar they withdraw in retirement is taxed as ordinary income.

With Roth IRAs, qualified withdrawals are completely tax-free. This gives you flexibility to manage your tax bracket in retirement by choosing which accounts to withdraw from based on your other income and tax situation each year.

Example: Suppose you need $60,000 in retirement income. If all your money is in traditional accounts, you might need to withdraw $75,000 to net $60,000 after taxes. With Roth accounts, you could withdraw exactly $60,000 tax-free, or you could withdraw some tax-free Roth money and some taxable traditional money to optimize your tax bracket.

When Roth Conversions Make the Most Sense

Roth conversions are most beneficial when you can pay taxes at a lower rate today than you expect to pay in retirement. Several situations make conversions particularly attractive:

Lower Income Years: If you’re between jobs, recently retired, or have a temporary reduction in income, you might be in a lower tax bracket than usual. This creates an opportunity to convert at favorable tax rates.

Market Downturns: When your IRA balance is depressed due to market declines, you can convert more shares for the same tax cost. When the market recovers, all that growth happens tax-free in the Roth IRA, making effective investment portfolio management even more crucial.

Before Required Minimum Distributions: Once you turn 73, you must start taking required minimum distributions (RMDs) from traditional IRAs and 401(k)s. These distributions can push you into higher tax brackets and increase the taxation of your Social Security benefits, making Social Security tax planning essential.

High Future Tax Expectations: If you believe tax rates will be higher in the future, or if you expect to be in a higher tax bracket in retirement due to other income sources, paying taxes now at current rates can be beneficial.

The Roth Conversion Ladder Strategy

One sophisticated approach is the “Roth conversion ladder,” where you convert a portion of your traditional IRA each year over several years. This strategy helps you avoid large tax spikes while systematically moving money to tax-free status.

For example, instead of converting $200,000 all at once and paying taxes in the highest bracket, you might convert $40,000 per year for five years. This keeps you in lower tax brackets and reduces the overall tax cost of the conversions.

The ladder strategy works particularly well for people in their 50s and 60s who have time to spread conversions over multiple years before they need to access the money.

Potential Drawbacks and Risks

While Roth conversions offer significant benefits, they’re not without risks and drawbacks:

Immediate Tax Bill: The biggest drawback is the immediate tax cost. Converting $100,000 could result in a tax bill of $22,000-$37,000 or more, depending on your tax bracket.

Opportunity Cost: The money you pay in taxes can’t be invested for growth. You need to consider whether the tax-free growth in the Roth IRA will outweigh the lost investment opportunity of the tax payments.

Future Tax Uncertainty: Conversions are based on assumptions about future tax rates and your tax situation. If tax rates decrease or your retirement income is lower than expected, the conversions might not be as beneficial.

Impact on Other Benefits: Higher income from conversions can affect Medicare premiums, Social Security taxation, and eligibility for certain tax credits or deductions.

Strategic Timing for Conversions

The timing of Roth conversions can significantly impact their effectiveness:

Early in the Year: Converting early in the year gives you more time to see how the conversion affects your tax situation and make adjustments if needed.

After Market Declines: Converting when account values are down means you’re paying taxes on a lower amount, and all the recovery growth happens tax-free.

Before Social Security: Converting before you start receiving Social Security can help you avoid the complexities of Social Security taxation.

During Lower Income Years: Take advantage of years when your income is temporarily lower due to job changes, sabbaticals, or early retirement.

Tax-Loss Harvesting and Conversions

You can combine Roth conversions with tax-loss harvesting strategies to reduce the tax impact. If you have investments in taxable accounts that have lost value, you can sell them to realize losses that offset some of the income from Roth conversions.

This strategy requires careful planning and record-keeping, but it can significantly reduce the tax cost of conversions while helping you rebalance your portfolio.

Estate Planning Benefits

Roth IRAs offer superior benefits as part of your comprehensive estate planning strategy compared to traditional IRAs. Since Roth IRAs don’t have required minimum distributions during your lifetime, you can leave the entire account to your heirs if you don’t need the money.

Inherited Roth IRAs also provide tax-free growth and distributions for your beneficiaries, though they generally must be distributed within 10 years under current rules. This is still much more favorable than inherited traditional IRAs, where all distributions are taxable to the beneficiaries.

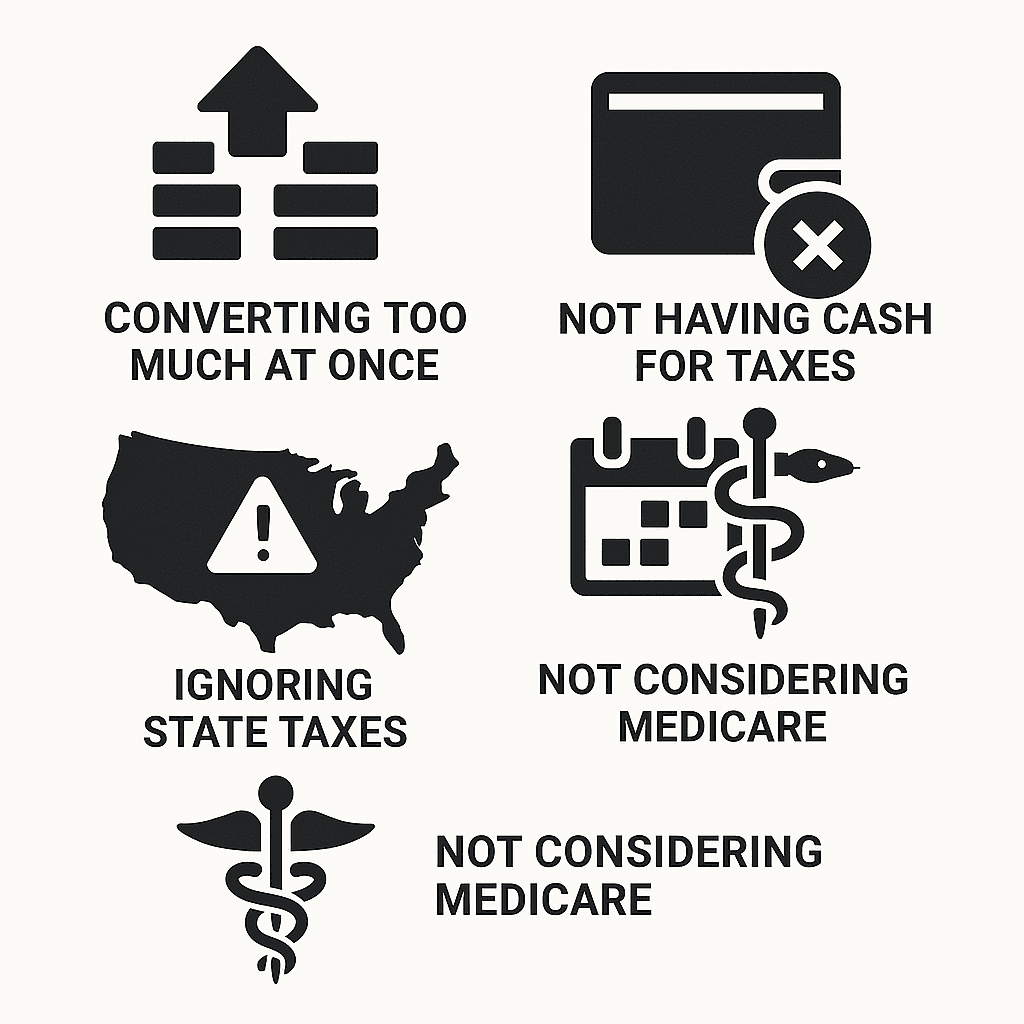

Common Mistakes to Avoid

Converting Too Much at Once: Large conversions can push you into higher tax brackets and increase the tax cost unnecessarily.

Not Having Cash for Taxes: Using retirement funds to pay conversion taxes eliminates much of the benefit and may trigger penalties if you’re under age 59½.

Ignoring State Taxes: Don’t forget about state income taxes on conversions. Some states don’t tax retirement income, which could affect the conversion decision.

Poor Timing: Converting at market peaks or during high-income years can increase the tax cost unnecessarily.

Not Considering Medicare: Large conversions can increase Medicare premiums two years later due to the income-based premium adjustments, requiring careful Medicare premium planning.

Working with Financial Professionals

Roth conversion strategies can be complex, especially when combined with other retirement and tax planning strategies. Consider working with fee-only financial planning professionals or tax professionals who can help you:

- Model different conversion scenarios

- Calculate the long-term tax implications

- Coordinate conversions with other comprehensive tax planning strategies

- Ensure compliance with all IRS rules and regulations

Is a Roth Conversion Right for Me?

Roth conversions aren’t right for everyone, but they can be extremely valuable for the right situations. The decision depends on your current tax situation, expected future tax rates, investment timeline, and estate planning goals.

If you’re in a lower tax bracket now than you expect to be in retirement, have cash available to pay the conversion taxes, and have time for the tax-free growth to compound, Roth conversions could save you significant money over your lifetime.

The key is to run the numbers for your specific situation and consider how conversions fit into your overall financial plan. Start with smaller conversions to test the strategy, and you can always increase the amounts in future years if the results are favorable.

Remember, Roth conversions are a long-term strategy. The tax-free growth and flexibility they provide become more valuable over time, making them potentially one of the most powerful tools in your retirement planning toolkit.

Ready to explore whether Roth conversions are right for your specific situation? Schedule a consultation with our team to discuss your retirement planning needs and develop a personalized strategy.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 9 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.