Imagine being forced to pay taxes on money you never wanted to withdraw from your retirement accounts. For millions of Americans with traditional 401(k)s and IRAs, this isn’t a hypothetical scenario – it’s a reality that begins at age 73. Required Minimum Distributions (RMDs) force you to withdraw money from your tax-deferred retirement accounts and pay taxes on it, whether you need the income or not.

This mandatory withdrawal system can create significant tax burdens and disrupt carefully planned retirement planning strategies. However, understanding RMDs and planning for them in advance can help you minimize their impact and even turn them into opportunities for more effective retirement planning.

What Are Required Minimum Distributions?

Required Minimum Distributions are mandatory annual withdrawals from tax-deferred retirement accounts that begin when you reach age 73. The IRS requires these distributions because they want to collect taxes on money that has been growing tax-deferred for decades.

| Account Type | Subject to RMDs? |

|---|---|

| Traditional IRA | Yes |

| Traditional 401(k) | Yes |

| 403(b) | Yes |

| 457(b) Plan | Yes |

| Traditional TSP (Thrift Savings Plan) | Yes |

| SEP-IRA | Yes |

| SIMPLE IRA | Yes |

Notably, Roth IRAs are not subject to RMDs during the account owner’s lifetime, making them valuable for estate planning and tax management.

How RMDs Are Calculated

The amount you must withdraw each year is based on your account balance and your life expectancy according to IRS tables. The calculation uses your account balance as of December 31 of the previous year, divided by a distribution period from the IRS Uniform Lifetime Table.

For example, if you’re 75 years old with a $500,000 IRA balance, your distribution period is 24.6 years. Your RMD would be approximately $20,325 ($500,000 ÷ 24.6). This amount is fully taxable as ordinary income.

The distribution period decreases each year, meaning your RMDs increase as a percentage of your account balance as you age. This ensures that most of your tax-deferred savings will be distributed (and taxed) during your lifetime.

The Tax Impact of RMDs

RMDs are taxed as ordinary income, which means they’re subject to the same tax rates as your salary or wages. This can create several tax challenges that require comprehensive tax planning services:

Higher Tax Brackets: Large RMDs can push you into higher tax brackets, especially when combined with Social Security, pension income, and other retirement income sources.

Social Security Taxation: RMDs count as income for determining whether your Social Security benefits are taxable. Higher RMDs can cause up to 85% of your Social Security to become taxable, making effective Social Security planning crucial.

Medicare Premium Surcharges: High income from RMDs can trigger Income-Related Monthly Adjustment Amounts (IRMAA), increasing your Medicare Part B and Part D premiums. This requires careful Medicare planning considerations.

State Tax Implications: Most states that have income taxes also tax RMDs, though some states provide partial or complete exemptions for retirement income.

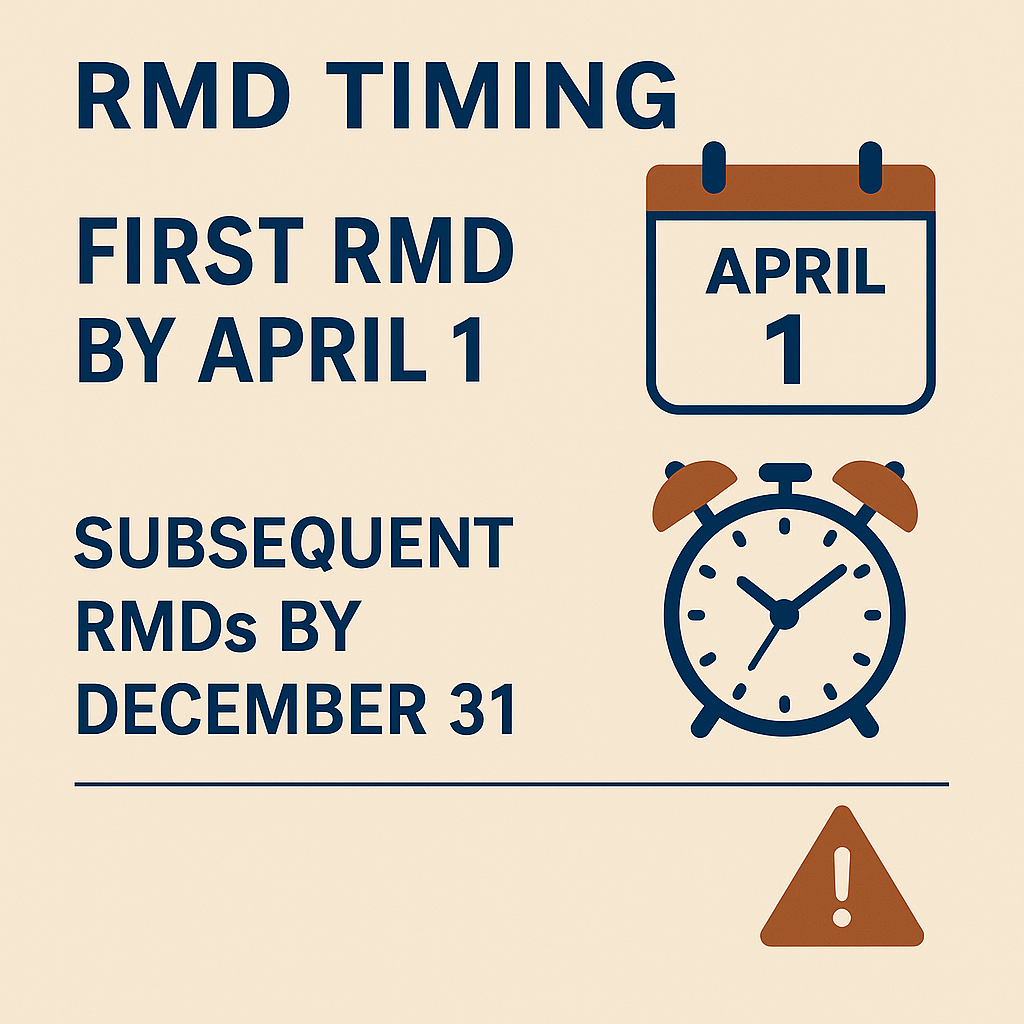

The Timing Challenge

The timing of your first RMD is particularly important. You must take your first RMD by April 1 of the year after you turn 73.

However, if you delay your first distribution until the following year, you’ll need to take two RMDs in that year – potentially creating a significant tax spike.

For subsequent years, RMDs must be taken by December 31. Missing the deadline results in a steep penalty: 25% of the amount you should have withdrawn, reduced to 10% if you correct the error promptly.

Strategies to Minimize RMD Impact

While you can’t avoid RMDs entirely, several strategies can help minimize their tax impact:

Roth Conversions Before Age 73: Converting traditional IRA money to Roth IRA conversions before you’re subject to RMDs reduces the balance subject to future RMDs. You pay taxes on the conversion now but eliminate future RMDs on that money.

Qualified Charitable Distributions: If you’re charitably inclined, you can donate up to $100,000 annually directly from your IRA to qualified charities. This counts toward your RMD but isn’t included in your taxable income.

Tax-Loss Harvesting: If you have taxable investment accounts, implementing tax-loss harvesting strategies can offset some of the tax impact from RMDs.

Asset Location Strategy: Keep tax-efficient investments in taxable accounts and tax-inefficient investments in tax-deferred accounts to minimize the tax drag from RMDs through effective portfolio management.

The Roth Advantage

This is where Roth accounts shine. Roth IRAs don’t have RMDs during the owner’s lifetime, giving you complete control over when and how much you withdraw. Understanding the differences between traditional vs Roth IRAs provides several advantages:

Tax-Free Growth: Money in Roth accounts can continue growing tax-free for your entire lifetime.

Estate Planning Benefits: You can leave larger amounts to heirs since you’re not forced to withdraw money.

Tax Management: Without RMDs, you have more control over your taxable income in retirement.

Social Security Optimization: Roth withdrawals don’t count as income for Social Security taxation purposes.

Planning Ahead: The Years Before RMDs Begin

The years between retirement and age 73 present unique opportunities for tax planning:

Lower Tax Bracket Years: If your income is lower in early retirement, consider Roth conversions to move money out of accounts subject to future RMDs.

Bridge Strategies: Use taxable accounts and Roth accounts for early retirement income while allowing traditional accounts to grow, but plan for the eventual RMD impact.

Healthcare Considerations: Large RMDs can affect Medicare premiums, so factor this into your healthcare cost planning.

The Qualified Charitable Distribution Strategy

For charitably minded individuals, Qualified Charitable Distributions (QCDs) offer a powerful way to satisfy RMDs without increasing taxable income. Here’s how it works:

- You can donate up to $100,000 annually directly from your IRA to qualified charities

- The donation counts toward your RMD requirement

- The distribution isn’t included in your taxable income

- You can’t also claim a charitable deduction for the gift

This strategy is particularly valuable for people who don’t itemize deductions but want to make charitable gifts while minimizing the tax impact of RMDs.

Multiple Account Considerations

If you have multiple IRAs, you can calculate the total RMD across all accounts but take the entire distribution from just one account if you prefer. This flexibility can help with investment management and tax planning.

However, 401(k) and other employer plan RMDs must be calculated and taken separately from each account. You can’t aggregate RMDs across different types of accounts.

Working Past Age 73

If you’re still working at age 73 and participating in your employer’s 401(k), you may be able to delay RMDs from that specific 401(k) until you retire. This exception doesn’t apply to IRAs or 401(k)s from previous employers.

This “still working” exception can be valuable for high earners who want to continue accumulating retirement savings and delay the tax impact of RMDs.

Estate Planning and Inherited Accounts

When you die, your beneficiaries will generally need to take distributions from inherited retirement accounts. The rules vary depending on the beneficiary’s relationship to you and when you died, but most non-spouse beneficiaries must now distribute inherited accounts within 10 years.

This makes the RMD conversation even more important for estate planning. Reducing the size of traditional retirement accounts through lifetime distributions or Roth conversions can reduce the tax burden on your heirs.

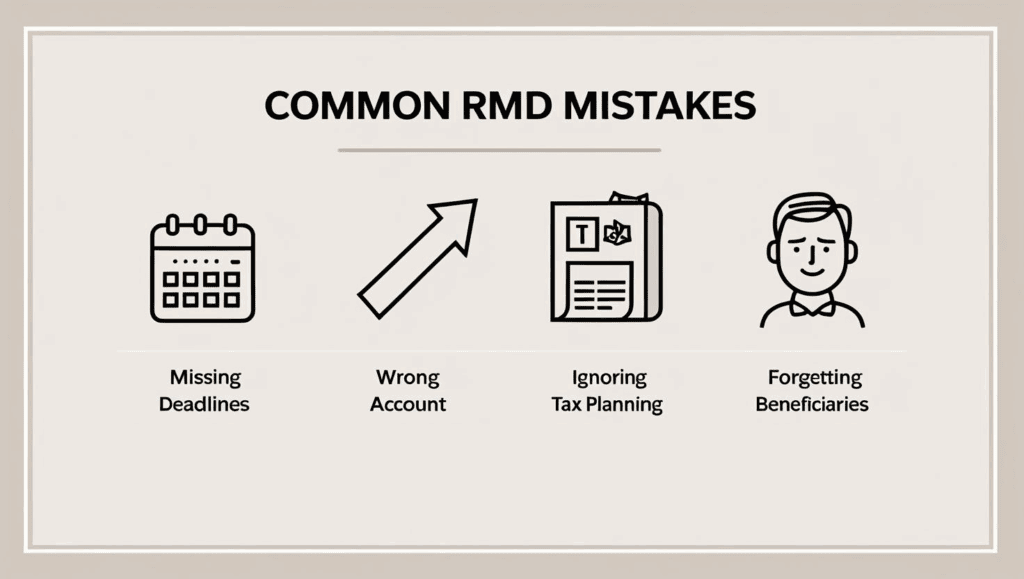

Common RMD Mistakes to Avoid

Missing the Deadline: The 25% penalty for missing RMDs is severe. Set up reminders or automatic distributions to avoid this costly mistake.

Taking RMDs from the Wrong Account: Make sure you’re taking RMDs from the correct accounts and in the correct amounts.

Ignoring Tax Planning: Don’t just take the minimum required – consider whether taking more in low-tax years might be beneficial for your overall tax strategy.

Forgetting About Beneficiaries: If you inherit retirement accounts, you’ll also have RMD requirements that may be different from your own accounts.

The Psychology of Forced Distributions

Many retirees find RMDs psychologically challenging because they represent a loss of control over their money. You’ve spent decades accumulating wealth, and suddenly the government is forcing you to withdraw it.

Reframing RMDs as part of your overall retirement income strategy can help. The money was always going to be taxed eventually – RMDs just force the timing. By planning ahead, you can ensure that RMDs fit into your overall financial plan rather than disrupting it.

Professional Planning Help

RMD planning involves complex interactions between taxes, investments, estate planning, and retirement income needs. Consider working with a fee-only financial advisor or tax professional who can help you:

- Calculate projected RMDs and their tax impact

- Develop strategies to minimize RMD taxes

- Coordinate RMDs with your overall retirement income plan

- Implement Roth conversion strategies before RMDs begin

How Do I Get the Most Out of My Required Minimum Distributions?

Required Minimum Distributions force you to pay taxes on money you might prefer to leave invested, but they don’t have to derail your retirement plans. With proper planning and strategic thinking, you can minimize their impact and ensure they fit smoothly into your overall retirement income strategy.

The key is to start planning before RMDs begin. Once you’re 73, your options become more limited. By understanding RMDs and planning for them in advance, you can maintain more control over your retirement finances and potentially save thousands of dollars in taxes over your lifetime.

Ready to develop a comprehensive strategy for managing your Required Minimum Distributions? Contact our team to schedule a consultation and create a personalized plan that minimizes the tax impact of RMDs while maximizing your retirement income efficiency.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 9 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.