Planning for your child’s or grandchild’s education remains one of the most impactful financial gifts you can provide. But with college costs continuing their relentless climb—and recent legislative changes expanding your options—the strategy landscape has evolved significantly.

Updates to 529 plans, combined with expanded definitions of qualified expenses and new Roth IRA rollover provisions, have fundamentally altered the risk-reward equation. Let’s examine both 529 savings plans and prepaid tuition options through this updated lens.

Understanding 529 Plans: More Flexible Than Ever

A 529 plan functions as a tax-advantaged investment account where your contributions grow tax-free and withdrawals remain tax-free when used for qualified education expenses. But the definition of “qualified” has expanded considerably beyond traditional college costs.

What Actually Qualifies as Education Expenses?

K-12 Education:

- Tuition at public, private, or religious elementary and secondary schools (up to $10,000 annually per beneficiary)

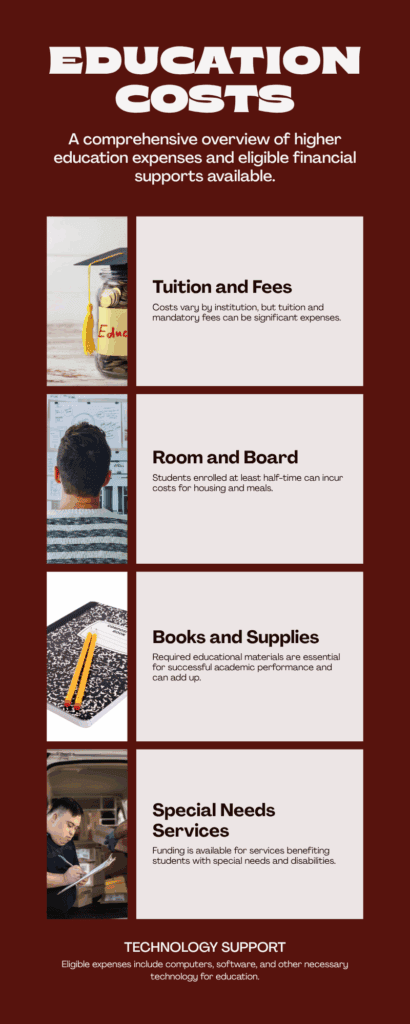

Higher Education Costs:

- Tuition and mandatory fees at eligible institutions

- Room and board for students enrolled at least half-time

- Required books, supplies, and equipment

- Special needs services for special needs beneficiaries

Technology and Equipment:

- Computers, related equipment, and software used for educational purposes

- Internet access and related services during enrollment years

- Printers and other peripheral devices designed for computer use

- Educational software (but not equipment primarily for entertainment)

Student Loan Payments:

- Up to $10,000 lifetime limit per beneficiary for qualified student loan repayments

- Includes loans for the beneficiary or their siblings

Apprenticeship Programs:

- Fees, books, supplies, and equipment for registered apprenticeship programs

The Game-Changing Addition: Roth IRA Rollovers

Starting in 2024, unused 529 funds gained a revolutionary new option that eliminates the “overfunding” fear entirely. Under specific conditions, you can roll up to $35,000 (lifetime limit) from a 529 plan into the beneficiary’s Roth IRA without penalties or taxes.

Key Requirements:

- The 529 plan must have been open for at least 15 years

- Only contributions made at least 5 years prior can be rolled over

- Annual rollover amounts limited by Roth IRA contribution limits ($7,000 in 2025)

- The beneficiary must own the receiving Roth IRA

- Normal Roth income limits don’t apply to these rollovers

Strategic Impact: This provision transforms 529 plans from education-only accounts into flexible wealth-building vehicles that can support both education and retirement goals.

Prepaid Tuition Plans: Guaranteed Protection with Trade-offs

Prepaid plans allow you to purchase future tuition at today’s prices, providing inflation protection specifically for tuition costs at participating institutions.

How They Work:

- Purchase tuition “credits” or “units” based on current pricing

- Credits cover the same percentage of tuition regardless of future increases

- Typically limited to in-state public institutions

- May offer refund options for non-participating schools

Benefits:

- Inflation hedge: Protection against tuition increases that often exceed general inflation

- No market risk: Returns tied to tuition inflation, not investment performance

- Predictable outcomes: Know exactly what percentage of tuition you’re covering

Limitations:

- School restrictions: Usually limited to in-state public colleges

- Incomplete coverage: Typically covers tuition only, not room, board, or other expenses

- Portability challenges: Reduced value if used at non-participating institutions

- Residency requirements: Many plans require contributor or beneficiary state residency

Strategic Analysis: Which Option Fits Your Goals?

| Factor | 529 Savings Plans | Prepaid Tuition Plans |

|---|---|---|

| Flexibility | Maximum school choice | Limited to participating schools |

| Expense Coverage | All qualified expenses | Tuition only |

| Market Risk | Yes (with growth potential) | No (guaranteed tuition coverage) |

| Portability | Full nationwide use | Reduced value out-of-state |

| Roth Option | $35,000 lifetime rollover | Not available |

Choose 529 Savings Plans If:

- Flexibility matters: You want maximum school choice and expense coverage

- Growth potential appeals: You’re comfortable with market risk for higher potential returns

- Comprehensive planning: You want to cover all college costs, not just tuition

- Roth rollover potential: You see value in the retirement savings backup option

Choose Prepaid Plans If:

- Risk aversion: You prefer guaranteed outcomes over market volatility

- State loyalty: You’re confident about in-state public school attendance

- Tuition focus: You plan to handle other expenses through different savings

- Inflation concern: You want specific protection against tuition increases

The Hybrid Approach: Best of Both Worlds

Many sophisticated savers combine both strategies:

Example Structure:

- Prepaid plan covering 50-75% of anticipated tuition costs

- 529 savings plan for remaining tuition, room, board, and other expenses

- Provides inflation protection while maintaining flexibility and growth potential

Example Application: The Rodriguez Strategy

Maria and Thomas have 8-year-old twins in Texas. Their approach:

Prepaid Component:

- Purchased 3 years of tuition through Texas’s prepaid plan

- Cost: $45,000 total ($22,500 per child)

- Covers most tuition at University of Texas system schools

529 Savings Component:

- Monthly contributions: $400 per child ($9,600 annually)

- Target: Cover remaining tuition, room, board, and graduate school

- Backup: Roth rollover option reduces overfunding risk

Their reasoning: The prepaid portion provides tuition security while the 529 component offers growth potential and flexibility. If the children choose different paths, they can redirect strategies accordingly.

Financial Impact Analysis: Updated Numbers

The expanded 529 benefits significantly improve the risk-reward calculation:

- Previous concern: “What if we save too much and pay penalties?”

- Current reality: Excess funds can become tax-free retirement savings

Example scenario: $100,000 in unused 529 funds

- Old system: 10% penalty plus taxes on earnings

- New system: $35,000 can transfer to Roth IRA penalty-free, remainder available for other family members’ education

This change makes aggressive 529 funding much more attractive, especially for families with multiple potential beneficiaries.

State-Specific Considerations

Tax Benefits Vary by State:

- Some states offer deductions for any 529 plan contributions

- Others require using their specific state plan

- Several states provide tax credits instead of deductions

Examples of generous state benefits:

| tate | Benefit Type | Annual Limit | Additional Features |

|---|---|---|---|

| New York | Tax Deduction | $20,000 (married) | Full state income deduction |

| Indiana | Tax Credit | $5,000 | 20% credit on contributions |

| Colorado | Tax Deduction | No limit | Full contribution deduction |

Research your state’s specific incentives—they can add immediate “returns” of 5-7% on contributions.

Advanced Planning Strategies

Gift Tax Optimization

529 plans offer unique gift tax advantages:

- Annual exclusion: $18,000 per person, per beneficiary in 2025

- Five-year averaging: Contribute up to $90,000 at once ($180,000 for married couples) without gift tax consequences

- Estate planning benefit: Removes assets from your estate while maintaining control

Multi-Generational Approach

Consider funding multiple generations simultaneously:

- Grandparents fund 529s for grandchildren

- Parents focus on maximizing employer 401(k) matches

- Creates tax-efficient wealth transfer while building education funds

Scholarship Coordination

If beneficiaries receive scholarships:

- Can withdraw equivalent amounts penalty-free (earnings still taxable)

- Remaining funds available for graduate school

- Excess funds eligible for Roth rollover

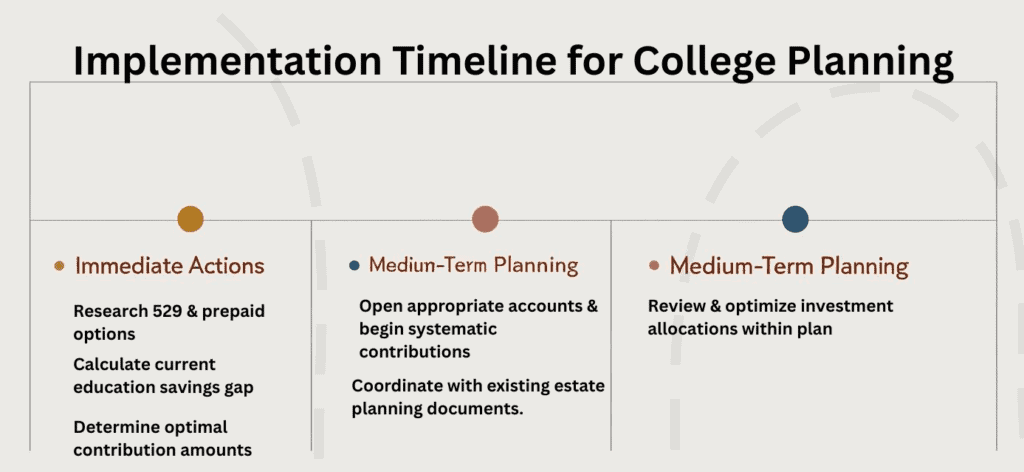

Implementation Timeline and Action Steps

Immediate Actions (Next 30 Days):

- Research your state’s 529 and prepaid options

- Calculate current education savings gap

- Determine optimal contribution amounts based on other financial priorities

Medium-term Planning (3-6 Months):

- Open appropriate accounts and begin systematic contributions

- Coordinate with existing estate planning documents

- Review and optimize investment allocations within plans

Ongoing Management:

- Annual contribution reviews to maximize tax benefits

- Rebalance investments as education timeline approaches

- Monitor for legislative changes affecting plan benefits

Common Implementation Mistakes to Avoid

For 529 Plans:

- Overly conservative investments for young beneficiaries

- Ignoring state tax benefits when choosing plans

- Failing to coordinate with overall financial planning

For Prepaid Plans:

- Not understanding transfer policies for out-of-state schools

- Overlooking inflation in non-tuition expenses

- Assuming all state schools participate equally

For Both:

- Starting too late to maximize compound growth

- Not considering multiple beneficiaries within the same family

- Ignoring financial aid implications (though generally minimal)

Looking Forward: The New Education Savings Paradigm

The combination of expanded 529 qualified expenses and Roth rollover options has created a new paradigm for education savings. These accounts now function as flexible family wealth-building tools rather than single-purpose education funds.

Key shift: Instead of asking “What if we save too much?” families can now ask “How can we optimize long-term wealth building while ensuring education funding?”

This philosophical change makes aggressive education savings much more attractive, especially for families who value financial flexibility and multi-generational wealth transfer.

Whether you choose 529 savings plans, prepaid tuition, or a combination of both, start with your family’s specific circumstances and values. The “perfect” strategy is one you’ll fund consistently while sleeping well at night, knowing you’re providing educational opportunities without compromising other financial priorities.

The expanded options available today ensure that money saved for education will find productive uses, whether funding a college degree, supporting career training, or providing a head start on retirement savings. That’s a powerful foundation for any family’s financial future.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.