When Growth Turns Risky

Sarah was proud. After 35 years of saving, her 401(k) had $1.2 million—most of it in stocks. She felt ready to retire.

Then the market dropped. Her account fell to $850,000. Retirement now felt scary.

What happened? Sarah didn’t do anything wrong. But she forgot one big thing: what works while you’re growing your money might not work when you need to use it.

Why Risk Changes in Retirement

The Market Works Differently Now

When you’re working, market drops aren’t a big deal. You’re still putting money in. Bad markets = buying on sale.

But when you retire, you start taking money out. And if the market is down when you withdraw, those losses can stick—and may never recover.

Let’s say your portfolio drops 30%. To get back to where you started, you need a 43% gain. That’s tough—especially if you’re pulling out money each month.

The Timing Risk No One Talks About

Financial experts call this sequence risk. It means when bad returns happen matters more than if they happen.

Here’s a simple example:

- Investor A gets good returns (like +15%) early in retirement.

- Investor B gets bad returns (like −15%) early in retirement.

They both take out the same amount every year.

Investor B runs out of money much sooner—even if their average return is the same.

Adjusting Risk As You Age

The Old Rule of Thumb

You may have heard: “Put your age in bonds.” So if you’re 65, have 65% in bonds, 35% in stocks.

Today, that’s a bit outdated—but the idea is still true: as you get closer to retirement, you should take less risk.

Yet many people still hold 80% or 90% in stocks because “that’s what always worked.” It did—for growing your money. Now the goal is protecting it.

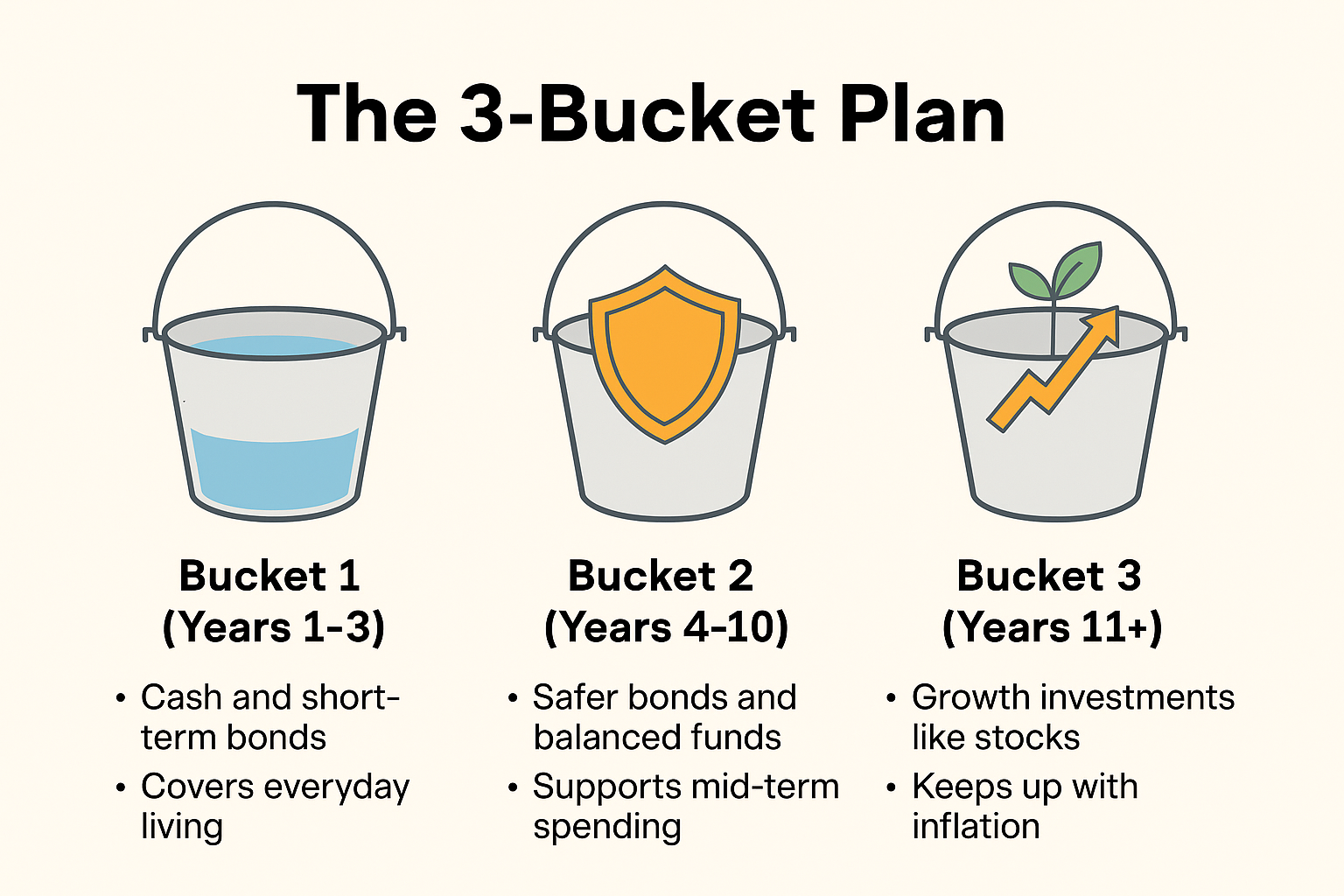

A Simpler Way to Think About Balance

The 3-Bucket Plan

Instead of picking between stocks and bonds, split your money by when you’ll need it:

- Bucket 1 (Years 1–3):

- Cash and short-term bonds

- Covers everyday living

- Bucket 2 (Years 4–10):

- Safer bonds and balanced funds

- Supports mid-term spending

- Bucket 3 (Years 11+):

- Growth investments like stocks

- Keeps up with inflation

This way, your future money can grow—but you don’t need to panic during a market drop today.

Are You Holding Too Much in Stocks?

Try This 3-Step Checkup

- Find your stock percentage.

Add up your 401(k), IRA, and other accounts. Is more than 70% in stocks? - Run a stress test.

Imagine the market drops 35% (like 2008). Could you still pay bills for 2–3 years without selling stocks? - Check your flexibility.

Could you delay spending or work part-time? Do you have other income like rental property or Social Security?

Warning Signs You’re Too Stock-Heavy

- Over 70% in stocks, less than 5 years from retirement

- No extra cash beyond emergency savings

- Relying only on investments for income

- Can’t pause spending if markets drop

- Worrying often about stock performance

A Balanced Example: The Johnsons

Tom and Linda, age 58, had $1.4 million—mostly in stocks. Their advisor helped them rebalance:

- 35% stocks

- 45% bonds

- 20% cash

When the market dropped 25%, their account only fell 12%. More importantly, they didn’t have to sell stocks to cover expenses. They let them recover.

Income-First vs. Growth-First

Instead of chasing returns, some retirees focus on steady income:

- 25–30% in dividend-paying stocks

- 40–50% in bond ladders or CDs

- 20–25% in cash and short-term savings

This mix helps reduce the chance of needing to sell when markets are down.

Don’t Panic—Shift Slowly

You don’t have to change everything today. Try this gradual transition:

- 10–5 years before retirement: Move from 80% stocks to 60%

- 5–1 year before retirement: Shift from 60% to 40–50%

- Early retirement: Keep 40–50% in stocks to help with inflation

Use new contributions and rebalancing—not panic selling.

Add Smart Diversification

You’re not limited to stocks and bonds. You might also consider:

- REITs (Real Estate Investment Trusts): for income

- TIPS (Treasury Inflation-Protected Securities): for inflation

- Commodities or gold: for protection in uncertain times

- International bonds: for global balance

Don’t Let Fear—or Ego—Lead You

Some investors love the growth game. Stocks become part of their identity. Slowing down can feel like “giving up.”

But retirement isn’t about ego. It’s about security. Balanced plans help you stay strong during downturns—and let you sleep at night.

What To Do This Month

Week 1: Take Inventory

- Gather statements

- See what % you have in stocks, bonds, and cash

Week 2: Stress-Test Your Plan

- Use a calculator to model a 30–40% drop

- Ask: Could I still retire? For how long?

Week 3: Make a New Plan

- Think about your goals

- Decide how much risk still makes sense

Week 4: Adjust Slowly

- Redirect new contributions to safer areas

- Schedule a quarterly review

- Talk to a fiduciary for advice (no product sales!)

Final Thought: Don’t Let Markets Choose Your Future

Your portfolio got you to retirement. Now it needs to get you through retirement. That takes a different strategy.

A balanced approach isn’t boring. It’s powerful. It protects you when others panic. And it gives you choices when others are forced to sell.

Want a Clear Picture of Your Risk?

We offer a simple, no-pressure portfolio review. We’ll help you see if you’re overexposed—and how to build a retirement plan that keeps you confident no matter what the market does next.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.