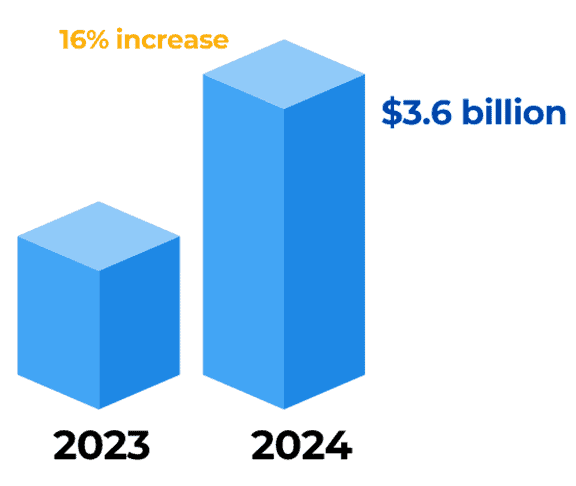

In 2024, the GivingTuesday Data Commons estimates that U.S. donors contributed approximately $3.6 billion—an increase of 16% compared to 2023. But beyond the headlines, what really matters for families is how to turn giving into a structured legacy and tax‑sensitive strategy.

Why This Matters to Your Family

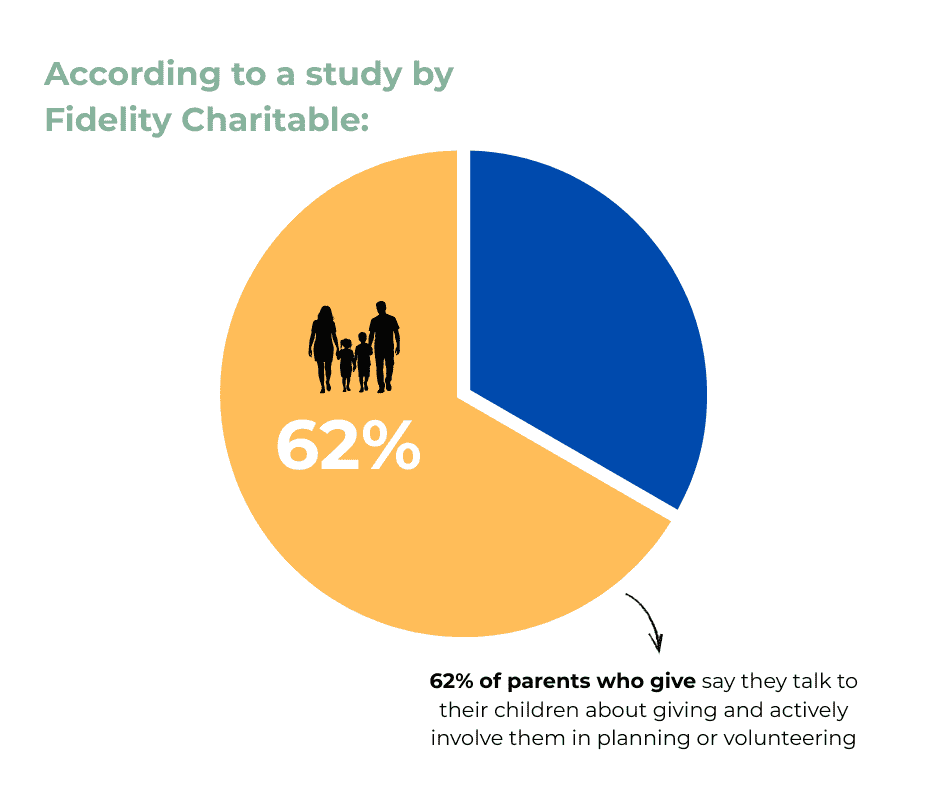

Many parents and grandparents say they want to pass down more than wealth—they want to pass down values. According to a study by Fidelity Charitable, 62% of parents who give say they talk to their children about giving and actively involve them in planning or volunteering.

That means there’s a gap: intention is high, participation is stronger—but structured family legacy gave habits often lag.

Smart Ways to Involve the Family

Choose Causes Together

Invite each family member to research a charity and present why it matters. Use this as a platform for values discussion—not just donations.

Use a Donor‑Advised Fund (DAF)

A DAF allows you to make an immediate charitable gift (and take the deduction), but decide later which charities receive the funds. You can appoint younger family members as successor advisors for decades.

Donate Appreciated Investments

Instead of cash, consider gifting appreciated stock or mutual fund shares. Benefits:

- You avoid capital gains on the appreciation.

- You receive a deduction based on full market value (if you itemize).

- The charity benefits from the pre‑tax growth. This strategy is especially relevant for taxable accounts and clients who itemize.

Want to Lower Your Taxes and Do Good? Use Your RMDs

If you’re over age 70½ (for many IRA holders), you can leverage a Qualified Charitable Distribution (QCD):

- Transfer up to $100,000/year directly from your IRA to a qualified charity.

- It counts toward your Required Minimum Distribution (RMD).

- It does not increase your taxable income.

- It can reduce the impact of Medicare IRMAA surcharges and taxable Social Security benefits.

For Pennsylvania residents: Because the state doesn’t tax Social Security retirement benefits, combining a QCD with your tax‑planning may offer a double benefit—reducing your federal taxable income while preserving favorable state tax treatment.

How to Time Giving for Maximum Tax & Legacy Impact

Charitable giving can serve more than emotion—it can be a strategic lever:

- In high‑income years or those involving a business sale/stock liquidation.

- When you’re executing Roth conversions and want to offset taxable income.

- To bunch deductions in alternating years if you don’t itemize annually.

- To support legacy/capital planning by gifting to family foundations or trusts.

Ideal steps: accelerate donations in years of higher taxes or large one‑time events; involve younger family members in selections and succession planning.

Quick Year‑End Giving Tips

- Start early—appreciated assets and stock gifts can take 5–10 business days to settle.

- Check for matching gifts via employers or community programs.

- Use a DAF for flexibility and involving the next generation.

- Talk with your advisor about integrating QCDs with RMDs, and about where the tax deduction benefits you most.

Align Charitable Giving With Tax Strategies

Charitable giving doesn’t have to be an after‑thought. With thoughtful planning, you can align your values, reduce taxes, involve your family, and leave a legacy that matters.

Whether it’s via a DAF, QCD, appreciated asset donation, or simply starting the conversation with your children—now is the time to turn generosity into a meaningful tradition and a strategic part of your financial plan.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.