How global bond shifts may be silently impacting your retirement security (and how to protect yourself)

Tom and Susan Thought They Were Ready to Retire

They’d saved for thirty years, built what looked like a solid nest egg, and even booked a celebratory cruise to Alaska. But during what should have been a routine check-in with their advisor, one quiet comment stopped them cold:

“We need to talk about what’s happening in Japan’s bond market.”

Japan? They’d never invested in Japan. How could something happening on the other side of the world possibly threaten their retirement?

The answer surprised them—and it might surprise you too.

What’s Happening in Japan (And Why It Matters Here)

After decades of keeping interest rates near zero, Japan’s central bank just changed course. Japanese government bonds—which investors ignored for years because they paid almost nothing—are now yielding over 4% on 40-year bonds for the first time in history.

Think about that for a second. For decades, big institutional investors around the world parked their money in U.S. Treasuries because Japanese bonds were basically worthless. Now, suddenly, Japan looks attractive again.

So what happens? Money starts flowing back to Japan. And when trillions of dollars shift direction, it doesn’t happen quietly.

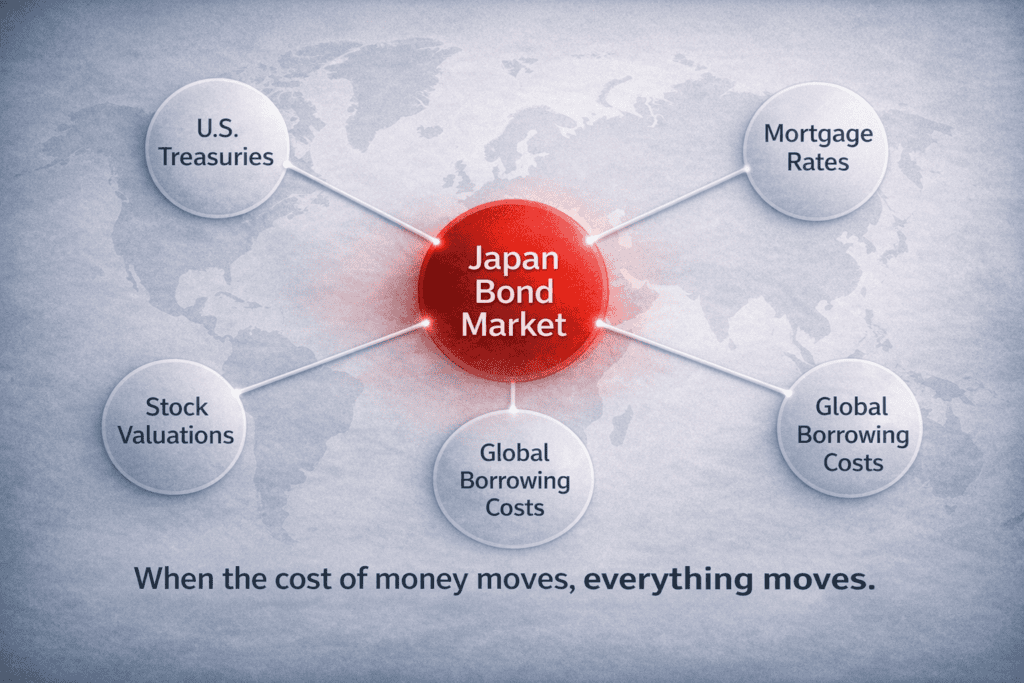

How This Touches Your Retirement (Even If You’ve Never Owned a Japanese Bond)

Here’s the ripple effect: When global investors leave U.S. bonds, our government has to offer higher yields to attract new buyers. That pushes U.S. interest rates up. Higher rates mean bond prices fall—especially on longer-term bonds many retirees depend on for “safe” income.

At the same time, rising rates create stock market volatility. And inflation can stay stubborn longer than expected. All of this hits retirement portfolios differently depending on where you are in your financial life.

If you’re still working and saving: Higher rates might help you earn more on CDs or money markets, but your bond funds could be quietly losing value. You might need to adjust your risk exposure sooner than planned.

If you’re within five years of retirement: Those bond funds you’ve counted on for stability might be worth less than you thought. That could mean your retirement income isn’t as secure as it looked six months ago.

If you’re already retired and drawing income: Rising rates put pressure on fixed-income strategies. Your purchasing power erodes faster with inflation. And if you’re forced to sell bonds that have dropped in value to pay for living expenses, you lock in losses you can never recover.

No matter where you are, understanding these shifts matters more than most people realize.

The Mechanics (Without the Jargon)

Bonds work like a seesaw. When interest rates go up, bond prices go down. The longer the bond’s maturity, the harder it falls. So yes, rising rates mean better income if you’re buying new bonds—but they also mean immediate losses if you need to sell what you already own.

Now picture a massive wave of global capital suddenly deciding Japan looks better than the U.S. That seesaw doesn’t just tilt—it slams down hard.

That’s what’s happening right now.

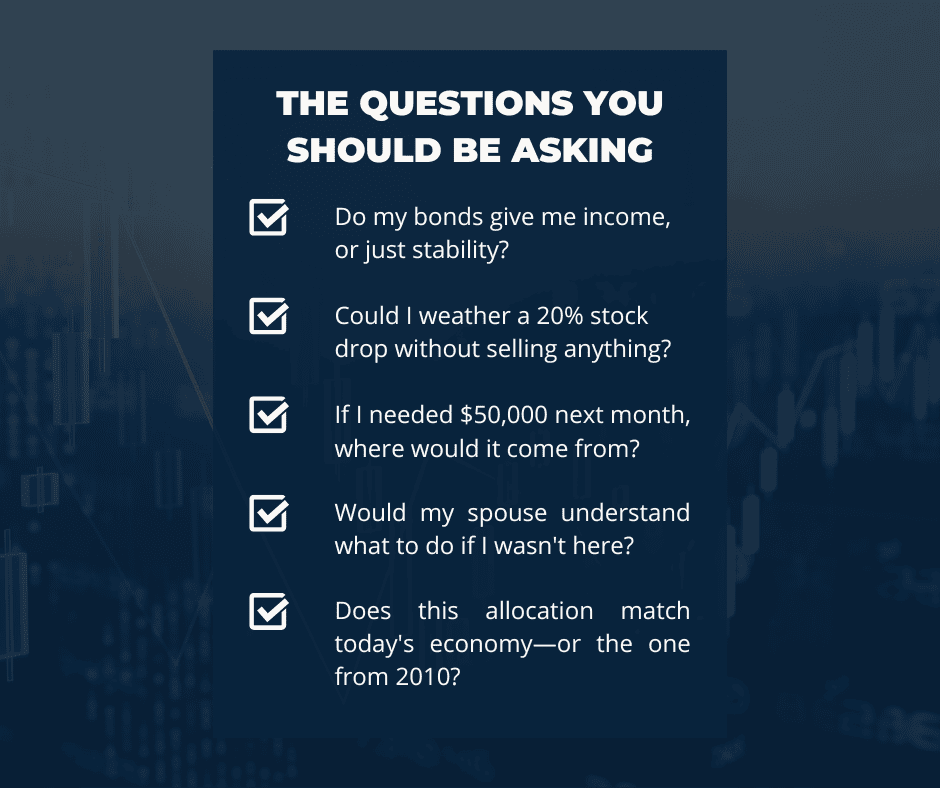

Three Things You Should Do This Month

- Review your bond exposure. Ask your advisor a simple question: What’s my bond duration? Are we holding long-term bonds that could drop significantly if rates keep rising?

- Stress-test your plan. What happens to your income if rates go up another percentage point? What if your bond holdings drop 10%? Your plan should be able to handle both scenarios without derailing your retirement.

- Look at income alternatives. Laddered CDs, short-term Treasuries, and inflation-protected securities (TIPS) might make more sense right now than traditional bond funds. The goal is matching your investment income to your actual spending needs—not just owning bonds because that’s what you’ve always done.

The Real Risk Nobody Talks About

Imagine your monthly budget depends on steady income from your portfolio. Food costs more than it did last year. Gas costs more. Healthcare costs more. Your portfolio is down 8%, but you still need to take out money to live.

So you withdraw a little extra to cover the gap. Then a little more next month. Before you know it, you’re eating into principal at exactly the wrong time—when your assets are already depressed.

This is what happens when global rate changes ripple through a retirement plan that wasn’t built to handle them.

Want to Know How Exposed You Really Are?

We’re offering something we call a Retirement Risk Checkup—a no-cost, plain-English review of your portfolio’s exposure to rising interest rates and the global bond shifts happening right now.

You’ll get a stress test of your current bond holdings, an inflation impact analysis, and a simple checklist of steps you can take immediately to protect yourself.

You’ve worked too hard and saved too long to let something happening 7,000 miles away derail your retirement. Let’s make sure your plan can handle whatever comes next.

Request your checkup here

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal, financial, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.