Nobody calls their advisor when things are going well.

Markets are steady. Statements look fine. Nothing hurts.

So they do nothing.

And that’s exactly when the most valuable planning work can happen — but almost nobody does it.

Here’s the problem: by the time something forces you to look at your plan, your options have already shrunk. You’re reacting. You’re emotional. And the moves that would’ve been easy six months ago are now expensive, stressful, or off the table entirely.

Whether you’re already retired or counting down the last few working years, the calm window is the one that matters most.

And most people waste it.

Why “Everything Looks Fine” Is the Most Expensive Assumption in Retirement

When markets are calm and account balances look stable, your brain does something sneaky.

It tells you nothing needs attention.

But here’s what’s actually happening underneath the surface while things “look fine”:

- Your income strategy might depend on selling investments at prices that won’t last

- Your tax exposure is growing quietly because no one’s managing it

- Your spending power is shrinking because inflation didn’t stop just because the headlines calmed down

- Your portfolio risk hasn’t been updated since the day you set it — even though your life has changed

None of these problems announce themselves. They don’t show up on your statement. They don’t send you a letter.

They just silently get worse until something forces them into the open. And by then, fixing them costs real money.

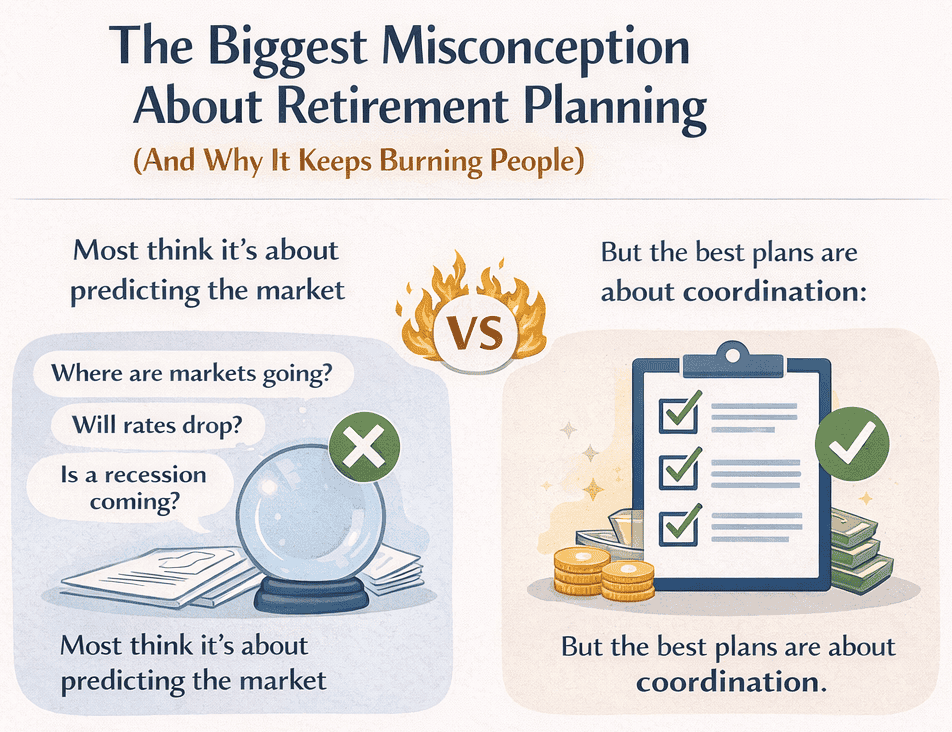

The Biggest Misconception About Retirement Planning (And Why It Keeps Burning People)

Most people think retirement planning is about predicting what’s coming next.

Where are markets going? Will rates drop? Is a recession coming?

That’s not planning. That’s guessing.

The retirement plans that actually hold up over 20 or 30 years aren’t built on predictions. They’re built on coordination:

- Which accounts you pull from and in what order

- How your income sources work together instead of against each other

- How your tax picture changes year by year — not just this April

- How your risk level matches the cash flow you actually need

When something goes wrong in the market, coordination is the first thing that breaks. People start making one-off decisions — sell this, move that, delay something else — and suddenly the whole plan is a pile of disconnected reactions.

Calm markets are the only time you can step back and make sure all the pieces still fit together.

Small Adjustments Now vs. Expensive Fixes Later

Here’s what nobody tells you about retirement planning:

The moves that save you the most money are boring.

A slightly better withdrawal sequence. A modest tax adjustment. A small shift in where your income comes from next year versus this year.

None of that makes for an exciting conversation. But over a 20-year retirement, those small adjustments compound into tens of thousands of dollars in taxes you didn’t pay, premiums you didn’t trigger, and income you didn’t lose to bad timing.

And here’s the key — these adjustments are only easy to make when things are calm. Once markets drop or a surprise tax bill hits, your options narrow fast and the emotional pressure to “do something” leads to worse decisions, not better ones.

Think about it like this: you don’t wait for a storm to check the roof. You check it on a sunny day when you can actually see what needs fixing.

What’s Quietly Changed (Even If Your Plan Hasn’t)

If your retirement plan was built — or last reviewed — more than a year or two ago, the world around it has shifted in ways that matter:

Interest rates aren’t where they were. Bonds, CDs, and fixed income behave differently now than when many plans were designed. If your income strategy was built in a low-rate world, it might not fit the current one.

Inflation changed the math. Prices went up and stayed up. Your spending assumptions from 2021 or 2022 are probably understating what you actually need — and that gap gets wider every year you don’t adjust.

Tax rules are shifting. The 2017 tax cuts are scheduled to sunset in 2026. SECURE 2.0 changed RMD timelines. IRMAA brackets haven’t kept pace with income growth. If no one’s modeled how these changes hit your specific situation, you’re flying blind.

Healthcare costs keep climbing. Medicare premiums, supplemental coverage, out-of-pocket costs — they’re all moving faster than general inflation. If your plan assumes flat healthcare expenses, it’s lying to you.

None of these changes require you to panic. But all of them require you to look.

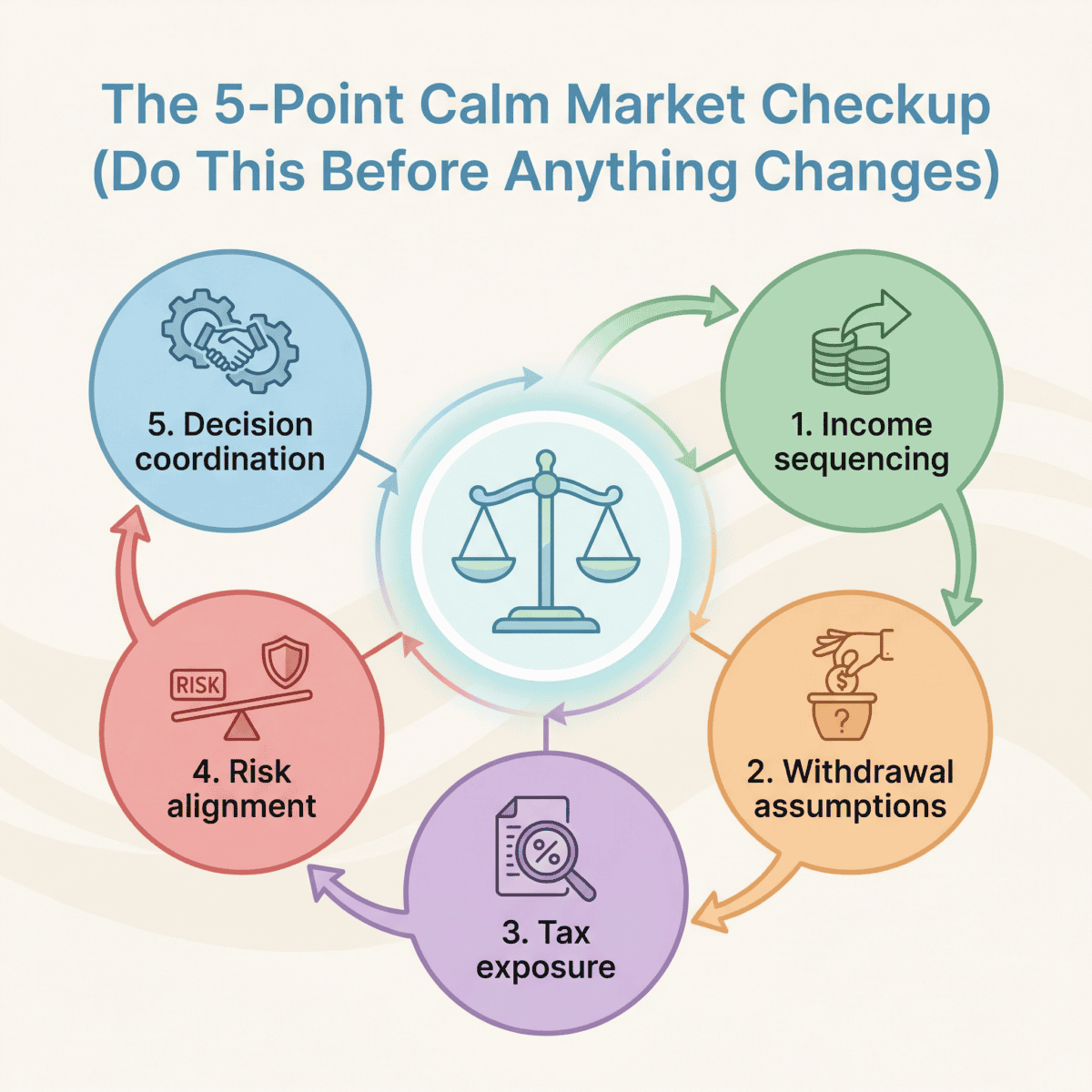

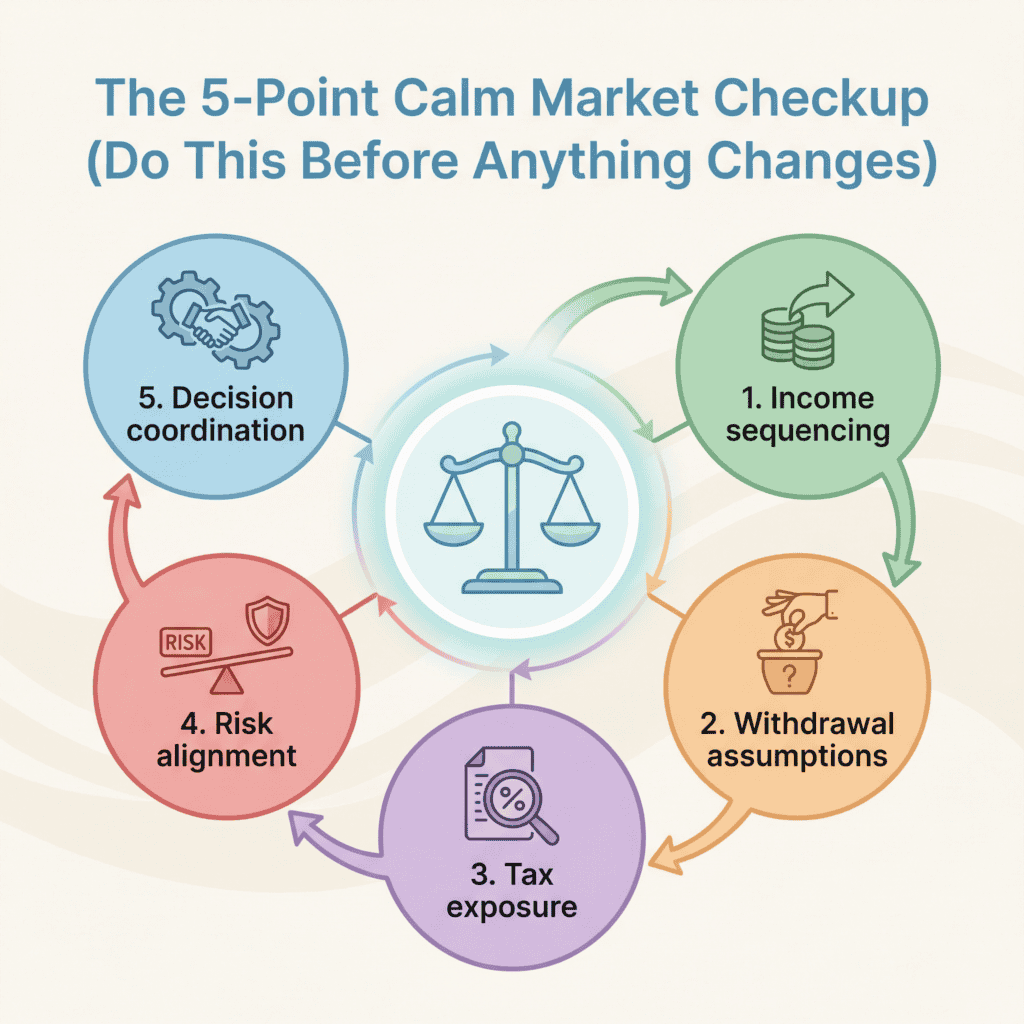

The 5-Point Calm Market Checkup (Do This Before Anything Changes)

You don’t need a full overhaul. You need a focused review. Here are the five things worth looking at while the window is still open:

1. Income sequencing — are you pulling from the right accounts in the right order? The order you draw from taxable, tax-deferred, and tax-free accounts has a massive impact on how long your money lasts and how much you keep. Most people just pull from whatever’s convenient. That’s not a strategy — it’s a default.

2. Withdrawal assumptions — would your plan survive a bad year right now? If markets dropped 25% next quarter, would you have to sell investments to cover expenses? If yes, that’s a vulnerability you can fix right now while prices are stable. If you’re pre-retirement, the question is the same — but the timeline is longer and the fixes are easier.

3. Tax exposure — do you know what your tax picture looks like for the next 3-5 years? Not just this year. The next several. Where will your RMDs land you? Are you on track to trip an IRMAA bracket? Is there a Roth conversion window you’re missing? This is the kind of modeling that only happens when someone sits down and runs the numbers across multiple years.

4. Risk alignment — does your portfolio still match how you actually use your money? What felt right at 58 might not fit at 66. What worked before you started drawing income might be too aggressive — or too conservative — now that you are. Calm markets give you the clarity to answer this without fear skewing the picture.

5. Decision coordination — are all the pieces talking to each other? Social Security timing, withdrawal order, tax strategy, Medicare planning, investment allocation — these aren’t five separate decisions. They’re one interconnected system. If they were planned at different times by different people (or not planned at all), there are almost certainly gaps.

Why the People Who Feel Most Confident Didn’t Get Lucky

There’s a pattern with the retirees and pre-retirees who feel genuinely secure about their money.

It’s not that they timed the market. It’s not that they had more to start with. It’s not that they found some secret investment.

They used the quiet stretches to get their plan right.

They reviewed when nothing was wrong. They made adjustments when it was easy. They asked hard questions when there was no pressure to answer them quickly.

That’s not luck. That’s discipline.

And the window to do it is open right now — while things are calm, while options are wide, and while the next storm is still on the horizon instead of at the front door.

The only question is whether you’ll use it or waste it.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.