For many investors, the surprise wasn’t that technology stocks fell over the past several weeks.

It was how much their “diversified” portfolio moved with them.

Artificial intelligence did not disappear. Innovation did not stop. What changed were expectations. Investors began reassessing how quickly heavy AI spending would translate into earnings, and as those expectations adjusted, stock prices followed. Because a small group of large technology companies represents a significant portion of major indexes, the impact reached far beyond a few individual stocks.

That gap — between how diversified a portfolio appears and how diversified it actually behaves — is worth examining.

How Diversification Can Narrow Over Time

Most investors today use index funds in some form: S&P 500 funds, total market funds, growth-oriented ETFs, target-date funds. These hold many companies. However, most major indexes are market-cap weighted, meaning the larger a company becomes, the more of it you own automatically.

When a small group of companies performs exceptionally well, their market value increases, their weight inside the index increases, and your exposure increases — even if you make no changes. Success increases concentration.

Over several strong years, a portfolio can become meaningfully dependent on a handful of companies without any deliberate decision by the investor. That is not a flaw in index investing. It is simply how the structure works. The recent tech decline exposed that structure.

Why This Matters More in Retirement

When you are accumulating wealth, volatility is part of the process. You are contributing regularly and typically have time to recover from downturns. Retirement changes the dynamic.

Once withdrawals begin, timing matters. Losses early in retirement carry greater long-term impact, and selling during a downturn can permanently affect portfolio longevity.

Consider a simplified example. Assume a $1,000,000 portfolio with a $50,000 annual withdrawal. If concentrated exposure leads to a 15% decline, the portfolio falls to $850,000. That same $50,000 withdrawal now represents nearly 6% instead of 5%.

The higher withdrawal rate increases long-term strain — and if markets recover slowly or leadership shifts for several years, that strain compounds. Each year spent withdrawing at an elevated rate digs a deeper hole, making full recovery progressively harder even when markets eventually turn.

This is sequence-of-returns risk. Concentration increases it.

The Risk Is Not Innovation

Artificial intelligence may continue to influence productivity and corporate growth for years. But markets do not price potential alone — they price expectations. When expectations are high, prices reflect that optimism. If earnings take longer than anticipated, valuations adjust, even if the long-term outlook remains intact.

The concern is not whether AI succeeds. The concern is whether a retirement portfolio has become overly dependent on one theme continuing to lead. Innovation can drive growth. Overexposure can increase fragility.

A Practical Way to Evaluate Your Exposure

Review your largest holdings. Across all accounts — IRAs, 401(k)s, brokerage accounts — identify your ten largest positions. You may find that the same companies appear in multiple funds. Different fund names do not always mean different exposure.

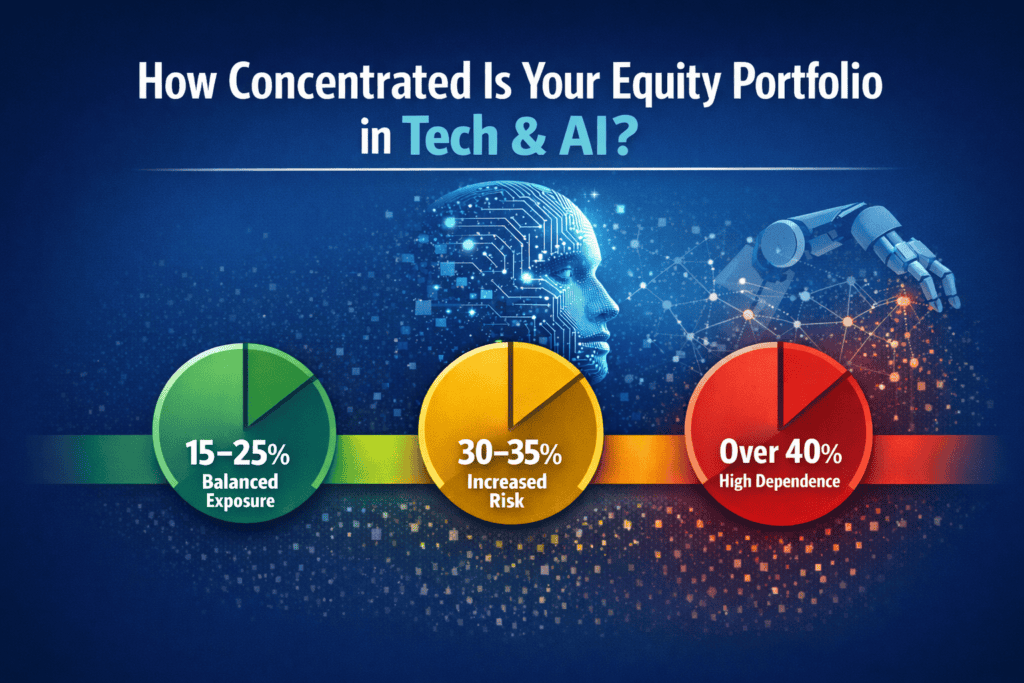

Estimate sector concentration. Determine roughly what percentage of your equity portfolio is tied to large-cap technology and AI-related companies. There is no universal correct number, but general risk-awareness markers can help: 15–25% in one sector is common in diversified portfolios; once exposure moves beyond 30–35%, dependence on that sector increases; above 40%, portfolio performance may be heavily influenced by that single area. The important question is whether your exposure reflects intention or drift.

Consider a scenario. If large-cap technology declined another 20–25%, how would your total portfolio respond? Would your withdrawal rate increase? Would you need to sell those holdings to fund spending? Would you feel pressure to alter your strategy? If you are unsure, that signals an opportunity to review structure — not a reason to react.

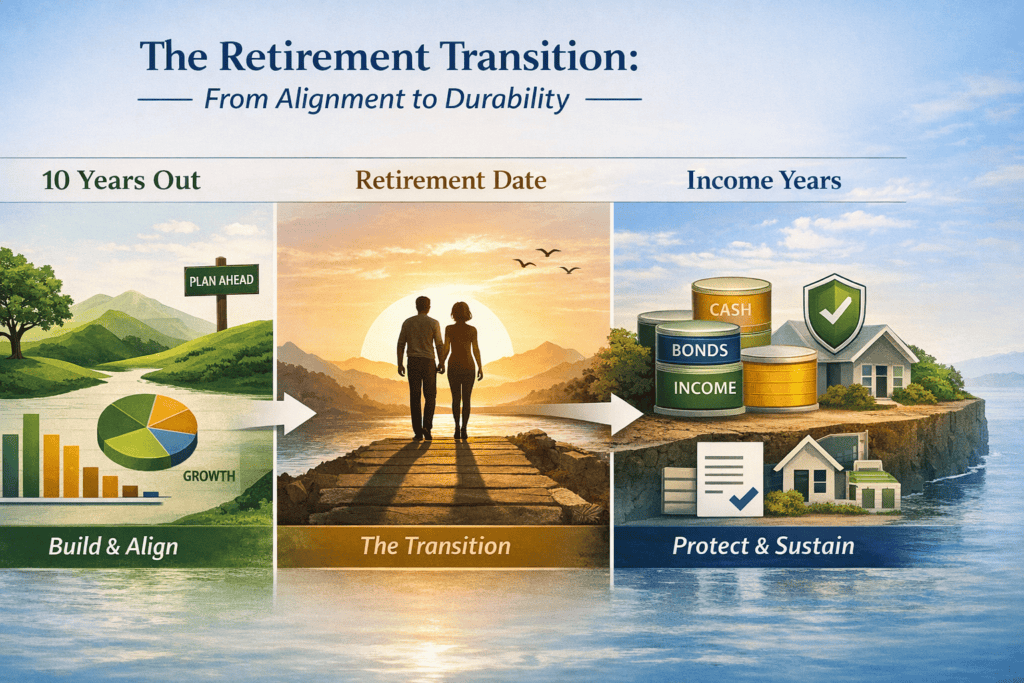

What Pre-Retirees Should Be Considering

If retirement is within the next five to ten years, you have flexibility. This is the period when alignment matters most.

You may want to rebalance deliberately — if recent performance pushed allocations beyond your intended targets, bringing them back in line can reduce unintended concentration. You may want to review long-term assumptions. If planning projections assume continued dominance from a narrow group of stocks, adjusting expectations modestly may improve resilience. And you may want to diversify by economic driver, because true diversification considers what drives earnings, not just how many funds you own.

What Retirees Should Be Considering

If you are already drawing income, the priority is durability.

Do you have sufficient cash or short-term fixed income to avoid selling equities during sector downturns? If one area declines, can income come temporarily from other sources? Does your current allocation reflect how the portfolio is being used today — not how it was built years ago?

Retirement portfolios are structured to endure cycles. They are not structured to depend on a single theme performing well indefinitely.

A Measured Perspective

The recent technology decline does not indicate the end of innovation. It does not require dramatic changes. But it does provide a useful checkpoint.

Market leadership rotates. Valuations adjust. Expectations evolve. A well-constructed retirement plan anticipates those shifts.

The key question is not whether technology rebounds quickly. The key question is whether your plan remains stable if it does not.

Remember the investor who was surprised by how much a “diversified” portfolio moved with tech. The goal of intentional structure is to make sure you are never caught off guard by your own portfolio.

If this review raises questions about exposure, income sustainability, or allocation drift — that is valuable information. Sound retirement planning is rarely about reacting to headlines. It is about making sure your portfolio reflects your plan, not the market’s latest theme.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.