Not everyone needs to make a move before April 15.

But some people absolutely should and most of them don’t realize it until the window has already closed.

The challenge usually isn’t complexity. It’s knowing whether this is simply a filing year, or a coordination year.

There’s a meaningful difference between the two. Filing years are maintenance. Coordination years are opportunities. And the way you tell them apart doesn’t require a CPA or a financial plan — it requires about 10 minutes and the right questions.

Here’s how to think through it.

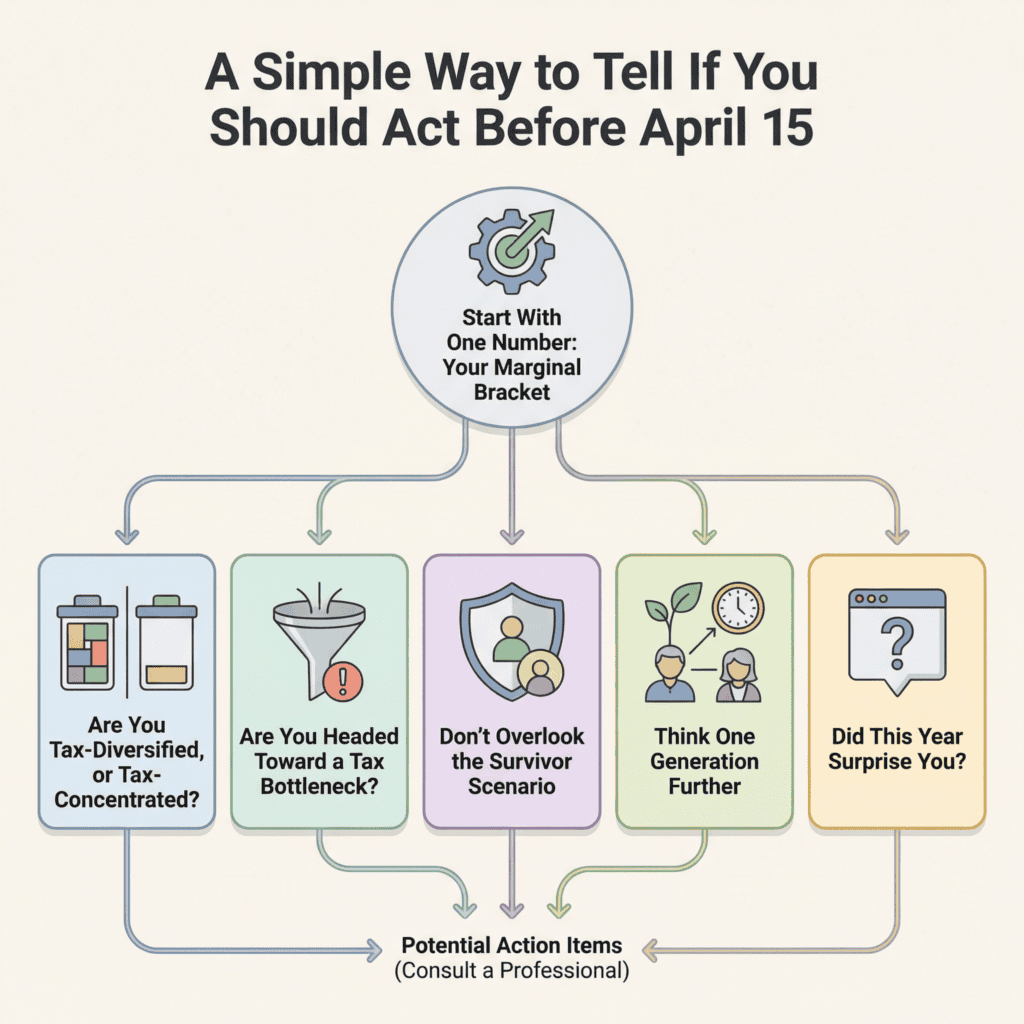

Start With One Number: Your Marginal Bracket

Forget the refund. Forget total tax paid.

The number that matters is your top marginal rate, the bracket your last taxable dollar landed in.

Now ask: Is this lower than where I expect to be in five to ten years?

If the answer is yes, or even “I’m not sure”, that’s the first signal worth paying attention to.

Current marginal rates remain below long-term historical averages. Future tax policy is genuinely uncertain. You don’t have to assume rates will rise to recognize that today’s bracket is worth understanding and, when appropriate, using deliberately.

Many retirees look back on the early years of retirement, before Social Security began, before Required Minimum Distributions kicked in, and wish they had been more intentional with that window. At the time, income felt lower than it would “really” be. In hindsight, it was their most flexible tax period.

That window doesn’t stay open indefinitely. And unused bracket space doesn’t carry forward.

Are You Tax-Diversified, or Tax-Concentrated?

Look at where your retirement assets actually sit.

Are most of them in tax-deferred accounts, traditional IRAs, 401(k)s, SEP-IRAs? If so, almost all of your future retirement income will be both mandatory and fully taxable. That’s not a crisis, but it is a constraint.

True flexibility in retirement comes from having assets spread across three buckets:

- Tax-deferred (traditional IRA, 401k) — taxed when withdrawn

- Tax-free (Roth IRA, Roth 401k) — withdrawn tax-free in retirement

- Taxable (brokerage accounts) — subject to capital gains rates, with more control over timing

When you have meaningful balances across all three, you can adjust your taxable income intentionally each year, pulling from whichever bucket makes the most sense given your bracket, Medicare thresholds, and other income sources.

When everything is concentrated in tax-deferred accounts, that flexibility disappears. To illustrate why that matters: a 64-year-old couple with $1.8 million entirely in traditional IRAs could face Required Minimum Distributions of $70,000–$90,000 or more annually by their mid-70s, before factoring in Social Security or investment income. That income stacks. And once it begins, it’s very difficult to reverse.

If most of your savings are tax-deferred today, April may be the easiest point in the year to start improving the balance.

Are You Headed Toward a Tax Bottleneck?

This is where many retirement tax plans quietly go sideways.

Income doesn’t arrive in neat, isolated streams, it stacks. Ordinary income fills your bracket first. Social Security taxation thresholds apply next, potentially making a larger portion of your benefit taxable. Long-term capital gains layer on top of that. And your total income from this year will determine Medicare premiums two years from now.

Now project forward. At age 73, will you have Social Security, RMDs, investment income, and potentially pension payments all arriving at once?

If so, there’s a reasonable chance those streams will push you into a higher bracket than you’re in today, and keep you there for the rest of your life.

That’s a tax bottleneck. And the best time to reduce the pressure is before the bottleneck forms, not after.

Early retirement years, when income is more flexible and brackets are less full, are typically the most efficient time for gradual coordination. Waiting until RMDs begin doesn’t eliminate the options, but it meaningfully narrows them.

Don’t Overlook the Survivor Scenario

This is one of the least-discussed planning considerations in retirement, and one of the most consequential.

What happens financially when one spouse passes away?

The surviving spouse doesn’t just lose a partner. They lose a tax filing status. Brackets compress from married filing jointly to single, which means the same level of income gets taxed at higher marginal rates. RMDs don’t shrink proportionally. Medicare premiums remain income-based. In many cases, a surviving spouse ends up paying significantly more in taxes on the same or less income.

Coordinating income now, while both spouses are alive and filing jointly with wider brackets, can meaningfully reduce the long-term tax burden for whoever survives. This is especially important for households where most retirement assets are held in tax-deferred accounts.

It’s a scenario that’s worth modeling, and it’s easier to address with options than without them.

Think One Generation Further

Here’s a question most people haven’t considered: What happens to your IRA after you’re gone?

Under current law, most non-spouse beneficiaries are required to withdraw inherited IRAs within 10 years. For adult children who inherit during their own peak earning years, those withdrawals may be taxed at their highest marginal rates, potentially 32% or higher.

That’s a generational tax multiplier. Money you spent decades building and protecting can lose a significant portion of its value in a relatively short window simply because of when and how it’s transferred.

Leaving large traditional IRA balances untouched may feel tax-efficient in the short run. But gradual conversion or coordination during your lifetime can reduce the long-term burden, for you and for those you’re planning to leave something to.

April planning isn’t only about this year’s return. It’s about the financial structure you’re building and eventually passing on.

Did This Year Surprise You?

Finally, take a direct look at what your return actually showed.

Did you owe significantly more than expected? Did Medicare premiums increase with no obvious explanation? Was more of your Social Security taxable than it was the prior year? Did a single financial decision, a distribution, a sale, a conversion, ripple into multiple areas you didn’t anticipate?

If so, that’s not a failure. It’s information.

And information, acted on, leads to better outcomes. Information ignored leads to the same surprise again next year.

Small adjustments, updating withholding on IRA distributions or Social Security, revisiting your income mix, thinking one bracket ahead, can prevent larger issues from compounding over time.

A Simple Rule of Thumb

If two or more of the areas above raised questions, this probably isn’t a “file and move on” year.

It’s a coordination year.

Not because something is wrong. But because flexibility still exists, and flexibility is the one resource in retirement tax planning that doesn’t automatically replenish.

Between ages 55 and 70, retirement tax planning tends to be proactive. You have bracket space to work with, Roth conversion windows to consider, and income you can shape. Between ages 73 and 85, it becomes increasingly reactive, income is more fixed, RMDs are mandatory, and the levers that once seemed optional are harder to reach.

April 15 sits in the middle of that transition. It’s an annual checkpoint with a natural deadline attached to it.

Most people file and move on.

Thoughtful investors file and then ask one more question: Are we shaping our future income structure intentionally, or just letting it happen to us?

If that question doesn’t have a clear answer yet, that’s not a problem. It’s a signal that the review is worth having while options are still on the table.

Wondering which of these areas applies to your situation? We’re happy to take a look. Schedule a complimentary conversation with our team — no obligation, just a clearer picture.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.