They did everything right.

Saved consistently for thirty years. Stayed diversified. Didn’t panic during 2008 or 2020. Retired at 63 with a solid portfolio and a plan that looked great on paper.

Then markets dropped 18% in their first year of retirement.

Not a catastrophe—but enough that their $7,500 monthly withdrawals started eating into a shrinking base. By the time markets recovered two years later, their portfolio had lost ground it would never fully make up. Not because of bad investments. Because their income was structured in a way that required selling at the worst possible time.

They weren’t trying to time the market. But their plan was.

This happens more often than most people realize. And the simplest way to find out whether your plan has this same vulnerability takes about five minutes—ideally while markets are still calm.

What Market Timing Actually Looks Like in Retirement

When people hear “market timing,” they picture extreme behavior—selling everything before a crash, going all-in after a rally, constantly adjusting based on forecasts.

That’s not how it shows up in most retirement plans.

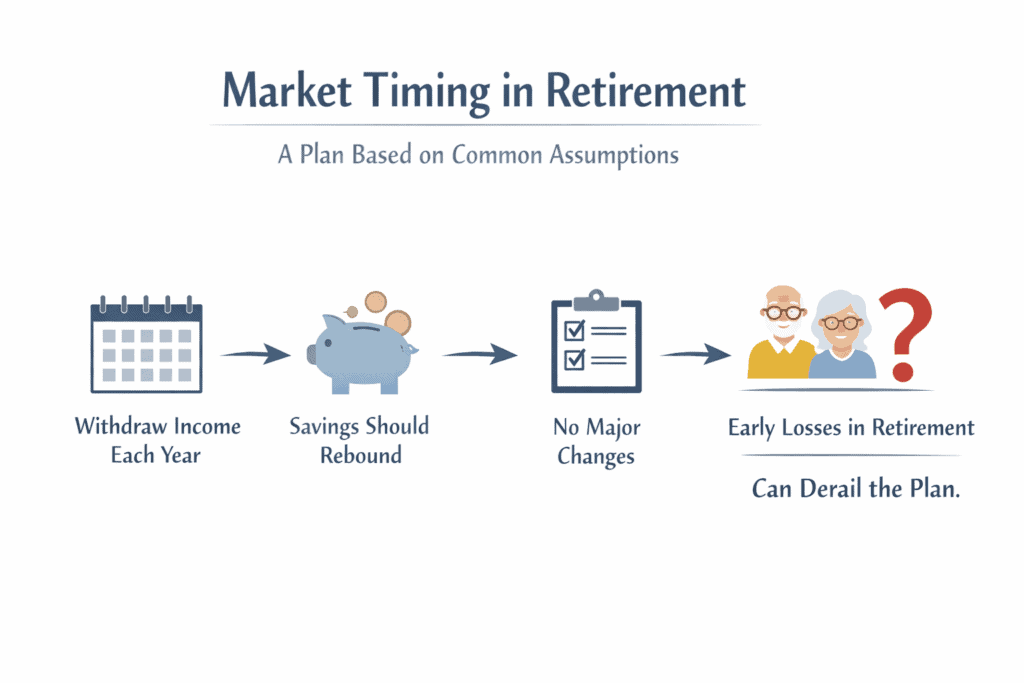

Instead, it’s embedded in assumptions that sound perfectly reasonable: “We’ll take income from investments each year and let the rest grow.” “The market usually recovers, so this should be fine.” “We won’t change anything unless something big happens.”

None of those statements are reckless. But together, they create a plan that only works if markets cooperate at the right times—especially in the first few years of retirement.

Why Retirement Changes the Math

During working years, time and new contributions smooth out volatility. A market drop is uncomfortable, but it doesn’t force action.

Retirement flips the equation.

Once withdrawals begin, you no longer control when money leaves the portfolio. Losses early on can permanently reduce future income. And recoveries don’t help if assets were already sold at depressed prices.

Here’s the math that makes this concrete: if you’re withdrawing $90,000 a year from a $1.5 million portfolio and markets drop 25%, you’re now pulling $90,000 from $1.125 million—an effective withdrawal rate of 8%. Even if markets bounce back 25% the following year, your portfolio doesn’t recover to where it started because you sold shares at the bottom.

This is why two people with identical portfolios can have dramatically different outcomes depending on when withdrawals happen and how income is sourced.

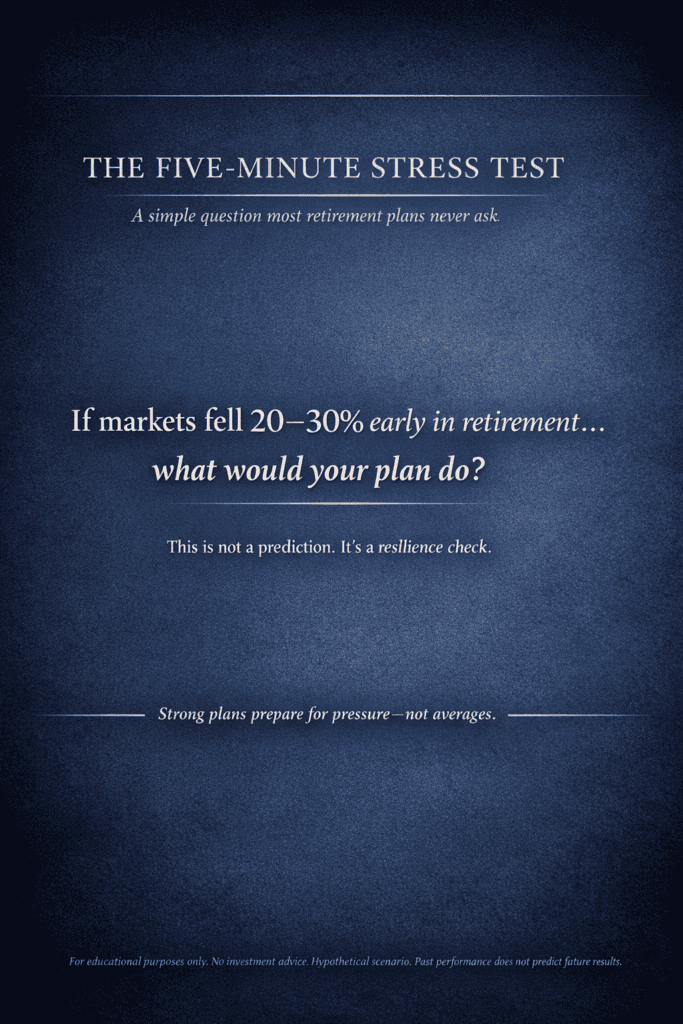

The Five-Minute Stress Test

Here’s the simplest way to evaluate whether your plan carries more timing risk than you think:

What would happen if markets declined 20–30% in the first two years of your retirement?

This isn’t a prediction. It’s a stress test. You’re not asking whether markets will fall—only whether your plan is resilient if they do.

If your honest answer sounds like “We’d probably keep withdrawing anyway” or “We’d have to sell investments” or “We’d hope it recovers quickly”—then market timing is playing a larger role than intended.

If you can say, “We’d shift to these specific accounts and reduce pressure on the portfolio for 18–24 months”—that’s a plan built for reality, not just averages.

Four Warning Signs Your Plan May Be Timing-Dependent

Market timing risk usually appears through patterns, not single decisions. These are the four most common ones we see.

1. Income requires selling investments regardless of conditions

If your regular income comes primarily from selling investments—without regard to what markets are doing—timing matters whether you want it to or not.

Picture this: you’re pulling $8,000 a month from a portfolio that just dropped 25%. You’re not just withdrawing income—you’re locking in losses and shrinking the base that needs to recover. Without alternative income sources or a plan for where withdrawals come from during downturns, you’re effectively betting that markets won’t stay down for long.

2. The plan assumes early retirement years will be “normal”

Many retirement projections rely on long-term average returns. Averages are useful, but they hide something critical: the order of returns matters more than the average itself.

A plan that assumes stable or positive returns in years one through five is more fragile than it appears. If those early years deliver below-average returns—which happens roughly half the time—the entire trajectory shifts. This is sequence-of-returns risk, and it’s the most common form of hidden market timing in retirement plans.

3. There’s no clear income sequencing strategy

Many families know how much income they plan to take, but not where it comes from under different conditions. If you can’t clearly answer which accounts get tapped first, how sources change in a down market, and how taxes and timing interact with withdrawals—then income decisions are defaulting to convenience rather than strategy.

That defaulting doesn’t feel like market timing. But it creates it—often increasing market exposure at the worst possible moment.

4. The plan hasn’t been reviewed since conditions changed

Interest rates, inflation, and market behavior don’t need to shift dramatically to affect timing risk. Small changes can alter how bonds behave, how long cash reserves last, and how much pressure falls on equities. A plan built for 2021’s conditions may quietly depend on assumptions that no longer apply—increasing its reliance on favorable timing without anyone noticing.

Why Calm Markets Are Exactly When You Should Check

It feels counterintuitive, but the best time to examine timing risk is when nothing feels urgent.

When markets are volatile, people focus on immediate outcomes and decisions get emotionally charged. During calm periods, you can focus on structure and resilience. Adjustments can be incremental. Options are still available. There’s no pressure to “do something.”

That’s when the most valuable improvements get made—not during the storm, but before it.

What Flexibility Actually Looks Like

The goal isn’t to eliminate market exposure. Every retirement plan is influenced by markets to some degree, and that’s normal.

The goal is to reduce the consequences of bad timing. That comes from flexibility: multiple income sources so you’re not forced to sell in a downturn, cash or short-term reserves that buy time, adaptive withdrawal strategies that adjust to conditions, and tax-aware sequencing that coordinates decisions across accounts.

Even modest flexibility—enough reserves to cover 18–24 months of income without touching equities—can dramatically change outcomes. It doesn’t require predicting markets. It simply requires acknowledging that you can’t.

The Conversation Worth Having Now

Many families quietly worry about this, even when everything looks fine on paper. That concern is reasonable.

Identifying timing risk doesn’t mean making dramatic changes. Often it means clarifying where income comes from in different scenarios, adjusting withdrawal flexibility, and rebalancing risk relative to what you actually need the money to do. Small refinements made during calm periods prevent large problems later.

If you’re not sure where your income would come from during a two-year downturn, that’s the conversation worth having now—while there’s still time to have it on your terms.

Because the goal of retirement planning isn’t to get the timing right. It’s to make timing matter less.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.