The Comfort (and Danger) of Cash

Cash feels safe. It doesn’t bounce like the stock market. It’s always there when you need it. That’s why so many retirees love it.

But here’s the catch: too much cash can silently shrink your wealth. It doesn’t grow. Inflation quietly eats away at it. And without growth, your money may not last as long as you do.

So how much cash should you keep in retirement? Let’s break it down in a way that feels clear, actionable, and comforting.

Why Retirees Love Cash

Cash makes you feel in control:

- Stable: It doesn’t change overnight.

- Simple: No fees, no fine print.

- Liquid: You can use it right away, no selling involved.

After decades of saving, cash feels like a reward—proof that you’ve made it. But as with many things in life, too much of a good thing can work against you.

The Quiet Risk of Holding Too Much Cash

1. Inflation Shrinks Your Power

Inflation is sneaky. At just 4%, it cuts your buying power by 20% in 5 years.

If you have $200,000 sitting in cash earning nothing, you could lose $40,000 of value just by waiting.

2. Missed Growth

Over the past 30 years:

- Stocks averaged 8–10% annually.

- Bonds averaged 3–5%.

- Cash? Usually less than 1%.

That gap matters. Say you keep $250,000 in cash instead of investing in a conservative bond fund averaging 4%. You miss out on $10,000/year in potential growth.

3. Longevity = Bigger Risk

The average 65-year-old couple today has a 50% chance that one spouse will live to age 90. That’s 25 years of retirement. Holding too much in cash means you’ll be forced to make trade-offs later—cutting travel, healthcare, or legacy goals.

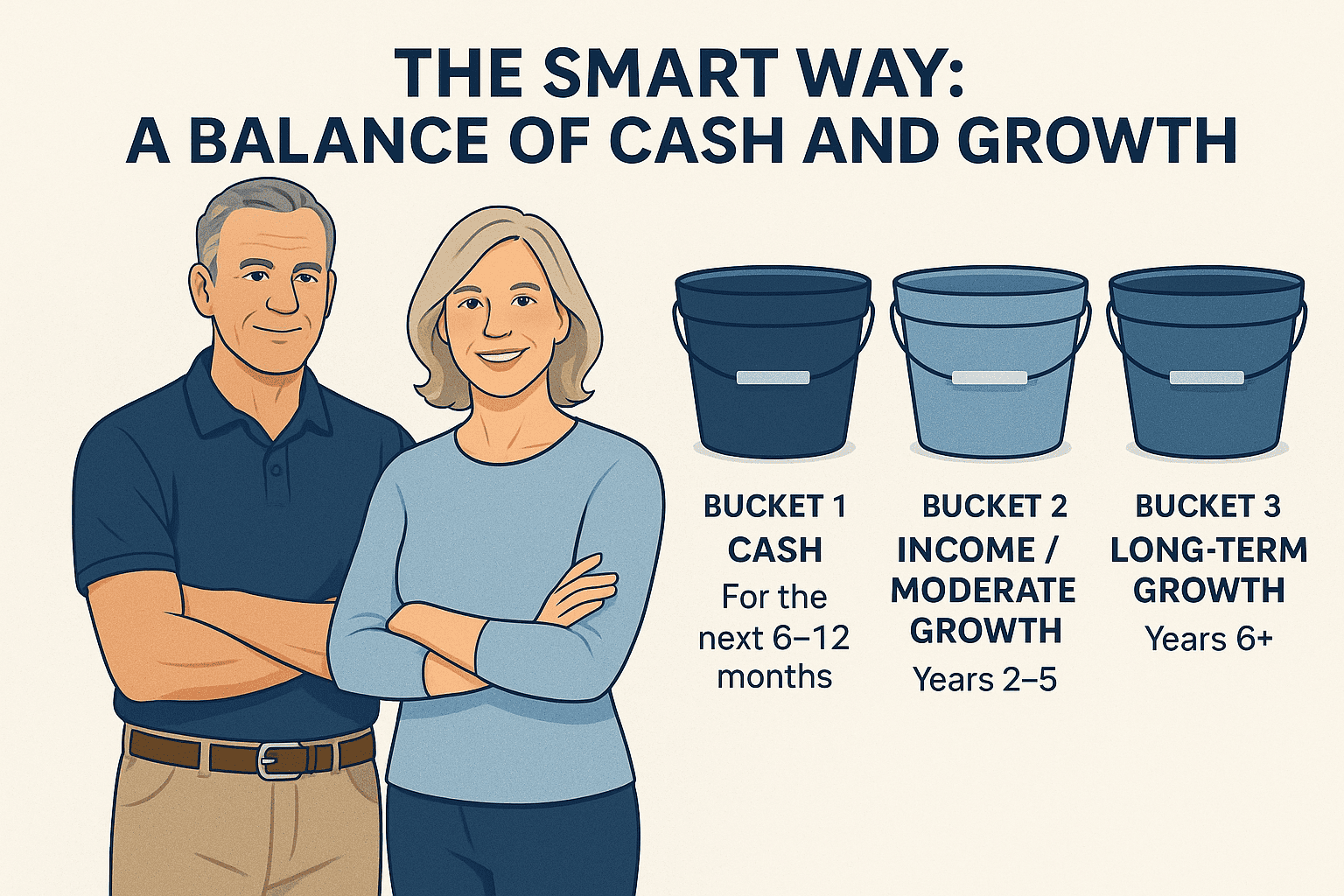

The Smart Way: A Balance of Cash and Growth

Rule of Thumb

Keep 6 to 12 months of core living expenses in cash—think housing, food, utilities, healthcare premiums.

Better: The 3-Bucket System

- Bucket 1 – Cash

For the next 6–12 months. Savings, money markets, or short-term CDs. - Bucket 2 – Income/Moderate Growth

Years 2–5. Bonds, bond ladders, conservative funds. These create stable, regular income. - Bucket 3 – Long-Term Growth

Years 6+. Stocks, ETFs, dividend payers. These fight inflation and support your lifestyle over time.

This approach reduces stress, improves predictability, and gives you the confidence to spend without fear.

The Emotional Side of Cash

Cash isn’t just a number—it’s a feeling.

- Security: “I can see it in my account.”

- Fear: “What if the market drops?”

- Guilt: “I spent my whole life saving—I don’t want to run out.”

That’s normal. At LFG, we help retirees align logic and emotion—so you feel at peace with your plan.

Hypothetical Example #1

Janet, age 68, kept $300,000 of her $800,000 portfolio in cash. She said, “I just want to be safe.”

But with inflation running at 4%, she lost $12,000 of purchasing power each year. Over 10 years, that’s $120,000—gone.

How to help her:

- Keep $100,000 in cash

- Move $200,000 into a bond ladder earning 4%

- Build a “retirement paycheck” from her investments

Now she can be earning $8,000/year in interest and feels just as secure.

Hypothetical Example #2

Ken and Laura, both 62, had $1 million. They were about to retire and planned to hold $400,000 in cash “just in case.”

How to help them create a 3-bucket system:

- $100,000 in cash (Bucket 1)

- $400,000 in income funds and short-term bonds (Bucket 2)

- $500,000 in stocks and dividend ETFs (Bucket 3)

With this structure, they can feel safe—but they don’t have to sacrifice long-term growth. When markets dipped, they have no need to sell stocks.

What NOT to Do with Cash

- Leave it all in checking: Regular checking accounts often pay 0%. A high-yield savings or money market account could earn 4–5% instead.

- Cashing out during downturns: Don’t panic and sell investments to load up on cash. That locks in losses and limits recovery potential.

- Forget to replenish: Don’t wait until the cash runs out to refill Bucket 1. Have a system.

FAQs: What Retirees Want to Know

Q: Should I keep more cash in volatile markets?

A: Yes, slightly more—but stick to your long-term strategy. Don’t overreact.

Q: What if I need a big expense like a car or surgery?

A: That’s why we recommend a cash reserve. Keep some “big-ticket” cushion if you have planned expenses.

Q: What if I like cash because I hate seeing losses?

A: Use the 3-bucket system. You don’t need to watch stocks daily if your short-term needs are fully covered.

Cash Audit Checklist

Use this to check if your cash balance is in the right zone:

- I know my monthly living expenses

- I have 6–12 months in high-yield savings

- I have a cash reserve for one-time big expenses

- I’ve allocated the rest of my money for income and growth

- I’m not holding cash “just because it feels safe”

If You’re 5–10 Years From Retirement…

Start shifting into the 3-bucket model now:

- Review your total cash holdings

- Use new savings to build up Bond Bucket (2)

- Set cash goals by category: emergency, everyday, extras

- Talk to a fiduciary to stress-test your plan

Bottom Line: Don’t Let Cash Hold You Back

Cash can make you feel safe—but too much holds you back.

The right amount of cash:

- Helps you sleep at night

- Covers emergencies

- Keeps you from selling in a panic

- Lets the rest of your money grow for the long haul

Want to Know If You’re Holding Too Much Cash?

Our simple, no-pressure retirement review shows you how to align comfort and growth—so you can spend confidently without worrying about running out.

Let’s turn your savings into a retirement plan that actually works for your life.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.