Nine Strategies That Could Add Thousands to Your Retirement Income

The Specific Moves Most Families Either Miss or Hear About Too Late

Key Takeaways

- Start RMDs at 73 or face a 25% penalty on missed withdrawals from traditional accounts.

- Reduce large retirement account balances before 73 to lower future mandatory taxable withdrawals.

- Target 2-3 specific strategies from the nine, not all, based on your income gap.

- Act before age-based deadlines close your window for certain retirement income strategies.

- RMDs are IRS-calculated, not optional—plan now to avoid forced high-tax withdrawals later.

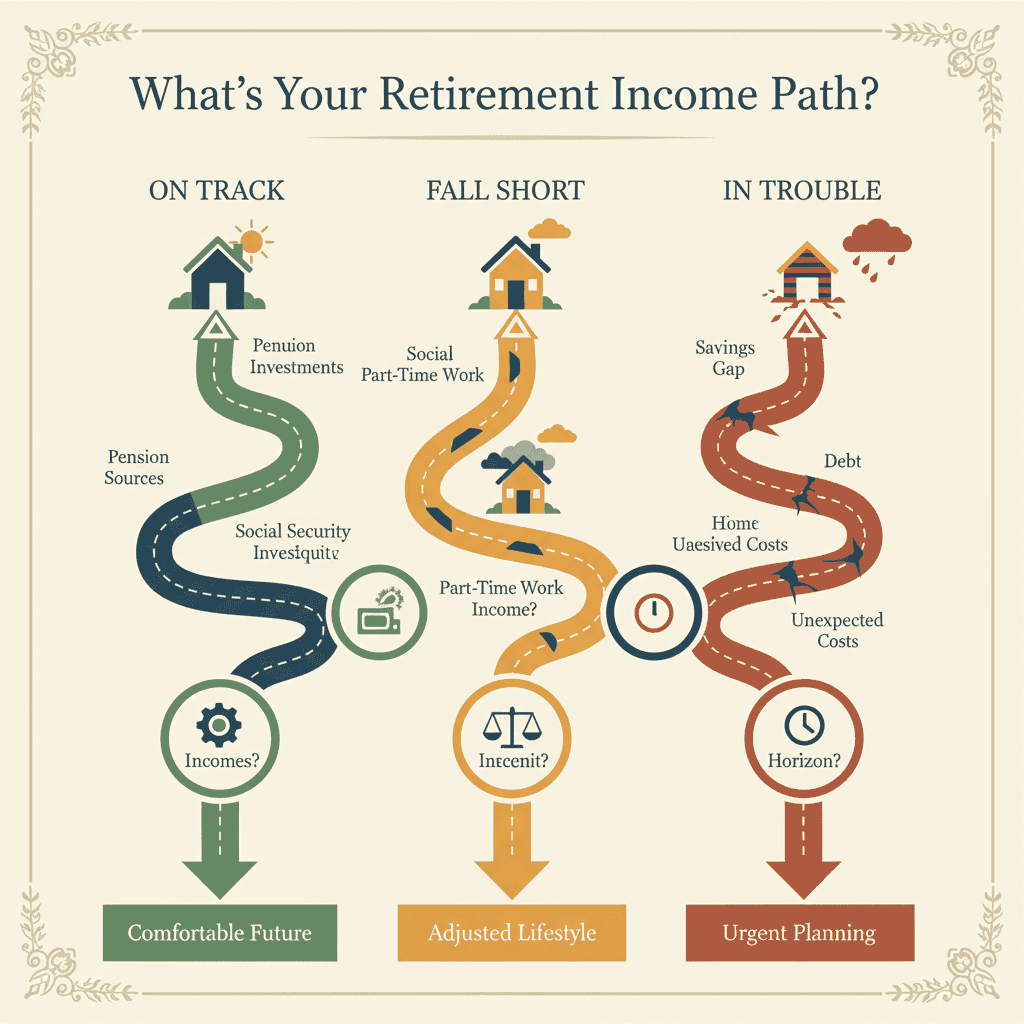

The Gap Is the Starting Point

If you have mapped your retirement income, you know one of three things. Your income covers your expenses. Your income falls a bit short. Or there is a real gap between what comes in and what goes out.

All three situations benefit from the same question: is there a way to make the number better?

The answer, in most cases, is yes. Not through riskier investments or guesswork, but through specific planning strategies that are available right now. Some have deadlines.

Some only apply during certain ages. Many of them affect each other in ways most people do not realize until someone connects the dots.

This article covers nine of them. The goal is not to do all nine. It is to find which two or three fit your situation and act while the window is open.

A Term Worth Understanding First: Required Minimum Distributions (RMDs)

Several strategies in this article connect to something called Required Minimum Distributions, or RMDs. Here is what that means in plain language.

Starting at age 73, the IRS requires you to withdraw a minimum amount from your traditional retirement accounts (401(k), traditional IRA, 403(b)) each year. You do not choose the amount. The IRS calculates it based on your account balance and your age. The larger your accounts have grown, the larger the required withdrawal.

Every dollar that comes out is taxed as ordinary income. You cannot skip it. You cannot defer it. And if you miss it, the penalty is steep: 25% of the amount you should have taken.

This matters because several of the strategies below are designed to reduce the size of your future RMDs, giving you more control over your income and your tax bill in later years.

Strategy 1: Catch-Up Contributions (Age 50 and Older)

What It Is

If you are 50 or older, the IRS allows you to contribute more to your retirement accounts than younger workers. For 2026, the limits are:

401(k), 403(b), and most 457 plans: $24,500 base contribution, plus $8,000 in catch-up contributions, for a total of $32,500 per year.

Traditional and Roth IRAs: $7,500 base contribution, plus $1,100 in catch-up contributions, for a total of $8,600 per year. This is the first time the IRA catch-up amount has increased since 2006.

The Super Catch-Up (Ages 60 Through 63 Only)

If you are currently 60, 61, 62, or 63, a higher catch-up limit applies under the SECURE 2.0 Act. You may contribute up to $11,250 in catch-up contributions to your 401(k), for a total of $35,750 per year. That is $3,250 more per year than the standard catch-up.

This window is exactly four years. The moment you turn 64, the higher limit goes away.

Who This Is For

Anyone 50 or older who is still working and has room in their budget to save more. The super catch-up is especially valuable for people in their early 60s who feel behind on savings. Many people in this age range spent their peak earning years paying for college tuition, helping aging parents, or rebuilding after a career change. The super catch-up exists partly because Congress recognized this reality.

A Note for Higher Earners

Starting in 2026, if your wages exceeded $150,000 in 2025, your 401(k) catch-up contributions must go into a Roth account (after-tax) rather than a traditional pre-tax account. This is a new SECURE 2.0 rule. The contributions will not reduce your current tax bill, but the money grows and comes out tax-free. If your employer’s plan does not offer a Roth 401(k) option, you may not be able to make catch-up contributions at all until the plan adds one.

What It Could Mean

Hypothetical scenario: A 61-year-old worker contributing the super catch-up maximum of $35,750 per year for three years (ages 61, 62, and 63) contributes approximately $107,250. At a 22% federal tax rate, the tax savings on pre-tax contributions could be roughly $23,595 over those three years. The contributions themselves, plus any growth, could add meaningfully to retirement income.

This is for illustrative purposes only. Actual limits, deductions, and growth rates vary by individual. Consult your plan administrator and tax professional.

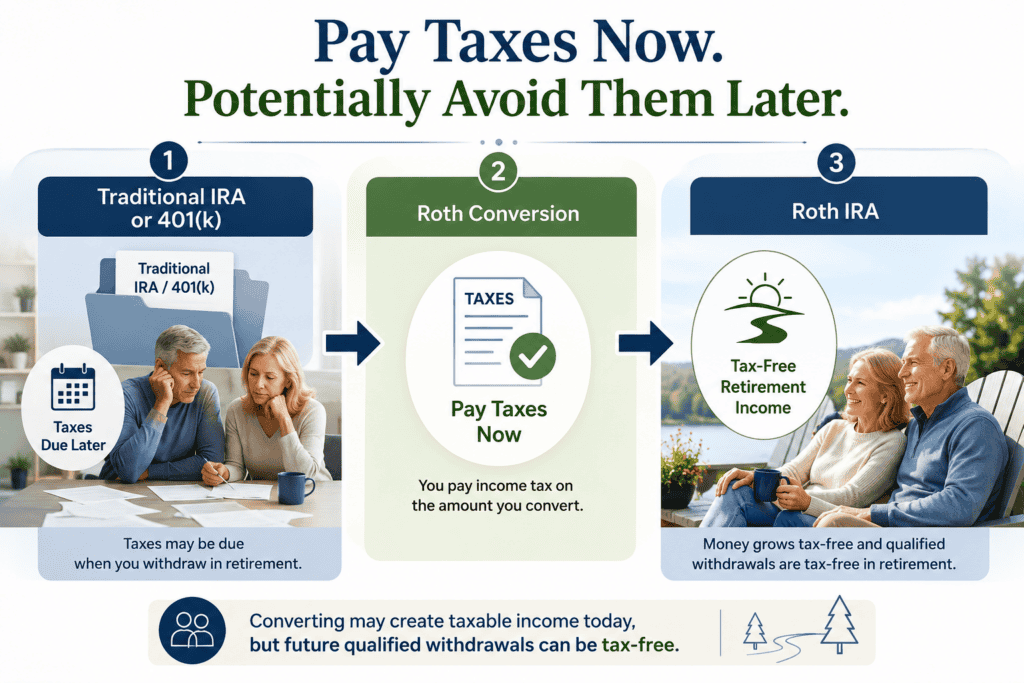

Strategy 2: Roth Conversions (Available at Any Age)

What It Is

Moving money from a traditional IRA or 401(k) into a Roth IRA. You pay income tax on the amount you convert now. In return, the money grows tax-free from that point forward and comes out tax-free in retirement.

Roth accounts are also not subject to Required Minimum Distributions during your lifetime. That means the IRS cannot force you to withdraw money you do not need, giving you more control over your income and tax bracket.

Who This May Be For

Anyone whose taxable income is temporarily lower than it may be in the future. This could happen during a job change, a sabbatical, the early years of retirement before Social Security starts, or any year when your income drops below its usual level.

The strategy is most commonly discussed for the years between retirement and age 73, when RMDs begin. During this window, many people find themselves in a lower tax bracket than they were while working. Converting some traditional IRA funds to Roth during these lower-income years could mean paying tax at 12% or 22% now, rather than paying at a potentially higher rate later when RMDs push income up.

However, Roth conversions are not limited to retirees. A pre-retiree at age 55 who takes a year off, changes careers, or has a low-income year for any reason could use that year to convert at a favorable rate.

Important: Being in a lower bracket after retirement is not automatic. If you have a pension, Social Security, and investment income, your bracket could remain high. The key is to look at your actual taxable income for the year and compare it to the bracket thresholds before deciding how much to convert.

Why the Timing May Be Especially Favorable Right Now

The One Big Beautiful Bill Act made the current federal tax brackets permanent. The seven rates (10% through 37%) are no longer set to expire. That means you can plan conversions with unusual clarity about what rate you will pay. Rates could always change under a future Congress, but for now, the rules are known and stable.

For Pennsylvania residents, there is an added advantage. Pennsylvania does not tax retirement account distributions, including Roth conversions done during retirement. The tax cost of a conversion for a PA resident is primarily federal.

The 2026 Federal Tax Brackets Worth Knowing (Married Filing Jointly)

10% on taxable income up to approximately $24,550. 12% from approximately $24,550 to $100,500. 22% from approximately $100,500 to $201,050. 24% from approximately $201,050 to $403,550.

These brackets are approximate and based on 2026 IRS guidance. Individual results depend on filing status, deductions, and other factors. Consult a qualified tax professional.

Strategy 3: The Backdoor Roth IRA (For Higher Earners)

What It Is

If your income is too high to contribute directly to a Roth IRA, there is a two-step workaround that remains legal under current law. In 2026, direct Roth IRA contributions phase out between $153,000 and $168,000 for single filers, and between $242,000 and $252,000 for married couples filing jointly.

The backdoor process works like this. First, you contribute to a traditional IRA without taking a tax deduction (up to $7,500, or $8,600 if 50 or older). Second, you convert that traditional IRA to a Roth, ideally within a few days. Since you already paid tax on the money, the conversion is largely tax-free.

The Trap to Watch For

If you have other pre-tax IRA balances (like a rollover IRA from a previous employer), the IRS uses something called the “pro-rata rule.” It treats all of your traditional IRAs as one combined pool. You cannot isolate just the new contribution for conversion. A portion of the conversion becomes taxable based on the ratio of pre-tax to after-tax money across all your IRAs.

The fix: if your employer’s 401(k) plan accepts incoming rollovers, you may be able to roll your pre-tax IRA balances into the 401(k) before doing the backdoor Roth. That removes the pre-tax money from the calculation.

Who This May Be For

Pre-retirees with household income above the Roth IRA contribution limits who want to build tax-free savings. This strategy works best with professional guidance to navigate the pro-rata rule.

The One Big Beautiful Bill Act did not restrict backdoor Roth conversions. Congress considered eliminating this strategy in 2021 but did not. As of 2026, it remains available.

Strategy 4: Delaying Social Security (Available From Age 62 to 70)

What It Is

For every year you delay claiming Social Security past your full retirement age (67 for anyone born in 1960 or later), your benefit increases by 8% per year, up to age 70. That increase is set by federal law, adjusts for inflation, and is guaranteed for life.

Claiming at 62, the earliest possible age, permanently reduces your benefit by approximately 30% compared to full retirement age.

Who This May Be For

Anyone who has not yet claimed and has the financial ability to wait. The decision is most important for the higher-earning spouse in a married couple, because the survivor benefit is based on the higher earner’s check. If the higher earner claims early, the surviving spouse is permanently locked into that lower amount.

For pre-retirees in their late 50s: you are not making this decision yet, but you are building the structure that will determine your options. If you can fund the first few years of retirement from savings while delaying your claim, the payoff over a long retirement could be substantial.

What It Could Mean

Hypothetical scenario: A worker with a full retirement age benefit of $2,800 per month at age 67 could receive approximately $1,960 at age 62 (30% reduction) or approximately $3,472 at age 70 (24% increase). The difference between claiming at 62 versus 70 is approximately $1,512 per month, or about $18,144 per year, for the rest of their life.

These figures are approximate and based on general Social Security Administration formulas. Actual benefits depend on individual earnings history. Visit ssa.gov/myaccount for your personal estimate.

Strategy 5: Tax Bracket Management (Most Powerful Before Age 73)

What It Is

Deliberately managing your taxable income each year to stay within a target tax bracket, or to “fill up” a lower bracket before RMDs push you into a higher one.

How to Actually Do It

Here is the step-by-step process.

Step 1: Pull your most recent tax return. Find your taxable income on line 15 of Form 1040.

Step 2: Look at which federal tax bracket you fell into (use the brackets listed under Strategy 2 above).

Step 3: Calculate how much room you have before the next bracket begins. For example, if you are married filing jointly with taxable income of $85,000, you are in the 12% bracket, which ends at approximately $100,500. That means you have roughly $15,500 of space before crossing into 22%.

Step 4: Consider withdrawing that $15,500 from a traditional IRA, paying 12% federal tax on it, and either spending it, moving it to a Roth, or putting it in a taxable account. If you do nothing, that money stays in the IRA, grows larger, and eventually comes out as an RMD at whatever your bracket is then, which could be 22% or higher.

Who This May Be For

Wondering if you’re leaving retirement income on the table? These nine strategies have specific age-based deadlines — and some windows close sooner than most families expect. Schedule a conversation with Langan Financial Group to explore which two or three moves make the most sense for your situation.

Anyone in a transition year where income is temporarily lower than usual. The first year of retirement. The years between leaving work and claiming Social Security. Any year before RMDs begin at 73.

Why It Works

You are paying tax now at a known, lower rate instead of paying later at a potentially higher rate. The savings come not from avoiding tax, but from choosing when to pay it.

Tax bracket thresholds are approximate. Consult a qualified tax professional before making withdrawal or conversion decisions.

Strategy 6: Withdrawal Sequencing (Every Year of Retirement)

What It Is

Choosing which accounts to draw from, and in what order, to reduce the total taxes paid across retirement. Most retirees have at least three types of accounts: pre-tax (traditional IRA, 401(k)), after-tax (brokerage accounts), and tax-free (Roth IRA). The order you tap them affects your annual tax bill, your Medicare premiums, the size of your future RMDs, and how long your savings last.

Who This Is For

Every retiree with more than one type of account. The common default is taxable first, then pre-tax, then Roth. That is often reasonable, but it is not always the most efficient path.

For retirees: if you have been drawing from one account type without looking at how it affects your broader tax picture, a sequencing review may be worthwhile. In some years, taking a small amount from pre-tax accounts even when you do not need to could reduce future RMDs and lower your long-term tax bill.

For pre-retirees: the accounts you contribute to now determine the options you have later. If nearly everything is in pre-tax accounts, you may face large RMDs and limited flexibility at 73. Building a Roth balance before retirement could give you a tax-free option you control.

What the Research Suggests

Vanguard’s Advisor Alpha framework estimates that tax-aware withdrawal strategies may add meaningful value over a multi-decade retirement compared to a default approach. The benefit compounds over time because each year’s tax savings can remain invested.

Strategy 7: Health Savings Account as a Retirement Tool (For Those With Eligible Plans)

What It Is

If you are enrolled in a high-deductible health plan (HDHP), you may contribute to a Health Savings Account. The HSA is the only account in the tax code with a triple tax benefit: contributions may be tax-deductible going in, growth is tax-free, and withdrawals are tax-free when used for qualified medical expenses.

For 2026, contribution limits are $4,400 for individual coverage and $8,750 for family coverage. If you are 55 or older, you may add $1,000 more per year.

The Strategy Most People Miss

Many people use their HSA like a checking account, spending it on medical bills as they come. The alternative: pay medical expenses out of pocket now, let the HSA grow for years, and reimburse yourself tax-free later. There is no time limit on reimbursement. A receipt from 2026 could be reimbursed in 2040.

After age 65, you can withdraw HSA funds for any purpose, not just medical expenses. Non-medical withdrawals after 65 are taxed as ordinary income, similar to a traditional IRA. But for medical expenses, which are one of the largest costs in retirement, HSA withdrawals remain completely tax-free at any age.

Who This May Be For

Pre-retirees between 55 and 64 who are still on an employer health plan with a high-deductible option. If you can afford to pay current medical costs from other funds and let the HSA grow, it could become a meaningful source of tax-free income in retirement, specifically for healthcare costs.

HSA eligibility ends when you enroll in Medicare (generally at age 65). You may still use existing HSA funds after enrolling in Medicare, but you can no longer contribute.

Strategy 8: Qualified Charitable Distributions (Age 70 and a Half and Older)

What It Is

A Qualified Charitable Distribution (QCD) allows anyone age 70 and a half or older to send money directly from their IRA to a qualifying charity. The amount counts toward the year’s Required Minimum Distribution. It is excluded from taxable income entirely.

Not deducted. Excluded. It never appears as income on the tax return.

The 2026 QCD limit is approximately $111,000 per person (indexed annually for inflation).

Who This Is For

Any retiree age 70 and a half or older who gives to charity and also takes distributions from an IRA. If you currently take a distribution, pay tax on it, and then donate some of that money, a QCD does the same thing with a lower tax bill.

What It Could Mean

Hypothetical scenario: A retiree who takes a $30,000 required distribution and gives $8,000 to their church could send that $8,000 as a QCD instead. Their taxable income drops from $30,000 to $22,000. At a 22% federal rate, that could reduce federal taxes by approximately $1,760.

Same gift. Same church. One phone call to the IRA custodian.

Because the QCD reduces adjusted gross income (not just taxable income), it may also help keep you below IRMAA thresholds for Medicare premium surcharges.

This is for illustrative purposes only. Actual savings depend on your tax rate, income, and deduction situation. QCDs must go directly from the IRA custodian to the qualifying charity. Consult a qualified tax professional.

Strategy 9: The New Senior Bonus Deduction (2025 Through 2028 Only)

What It Is

The One Big Beautiful Bill Act created a new federal tax deduction for anyone age 65 or older. It provides up to $6,000 for individual filers ($12,000 for married couples filing jointly). This is on top of the standard deduction and the existing age-related additional deduction.

Who This Is For

Anyone 65 or older with modified adjusted gross income below $175,000 (individual) or $250,000 (joint). The full deduction applies below $75,000 (individual) or $150,000 (joint). It phases out gradually above those levels.

What It Could Mean

For a qualifying married couple over 65, total available deductions in 2026 could include: the standard deduction of approximately $32,200, the existing age-related additional deduction of approximately $3,200, and the new senior bonus deduction of $12,000. That totals approximately $47,400 in income that would not be subject to federal tax.

Why the Deadline Matters

This deduction is temporary. It expires after the 2028 tax year. That means there are three tax years to use it: 2026, 2027, and 2028.

How It Works With Other Strategies

The senior bonus deduction can work alongside Roth conversions and tax bracket management. If the deduction lowers your taxable income, it creates additional room within your current bracket to take income or convert IRA funds at a lower rate. Coordinating all three over the next three years is the kind of planning that could produce measurable long-term results.

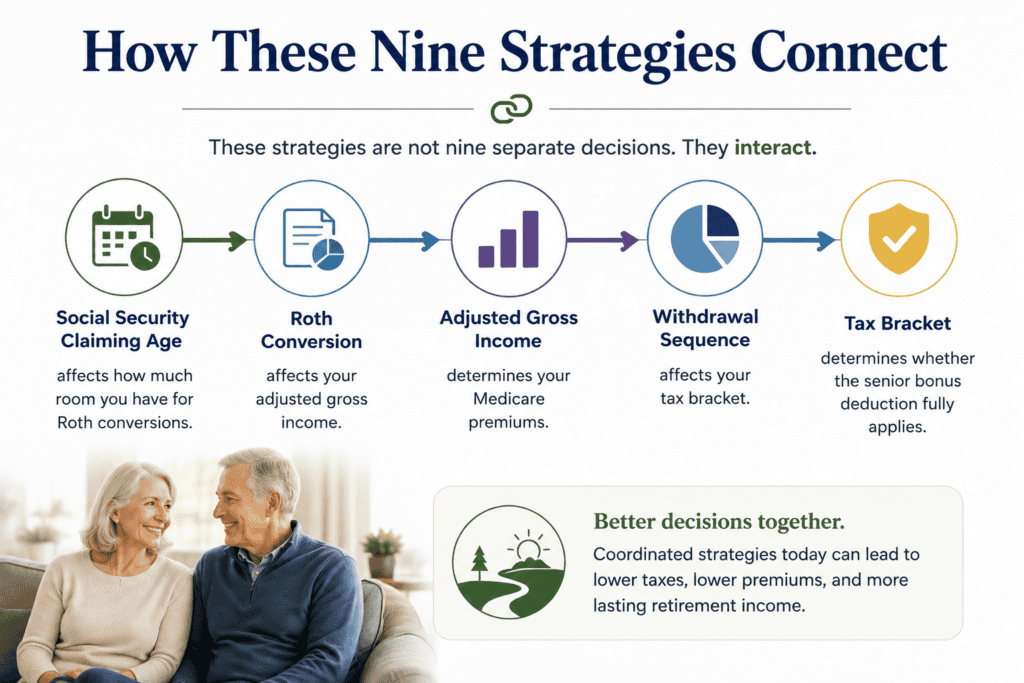

How These Nine Strategies Connect

These strategies are not nine separate decisions. They interact. Your Social Security claiming age affects how much room you have for Roth conversions.

Your Roth conversion affects your adjusted gross income. Your adjusted gross income determines your Medicare premiums. Your withdrawal sequence affects your tax bracket.

Your tax bracket determines whether the senior bonus deduction fully applies.

The families who get the most value from these strategies are not the ones who do each one alone. They are the ones who see how the pieces connect and coordinate the timing.

That coordination is what a retirement income plan is for. Not a prediction about markets. Not a pie chart. A deliberate, annually reviewed strategy for how every dollar of income arrives, when it arrives, and how it interacts with every other dollar.

Where to Start

You do not need to understand all nine strategies to take action this week. You need to find which one or two matter most for your situation.

If you are between 50 and 59: Check whether you are making catch-up contributions to your 401(k) and IRA. If not, the extra room is there.

If you are between 60 and 63: Call your plan administrator and ask whether the super catch-up is available in your plan. One call confirms it.

If your income dropped this year for any reason: Ask whether your current income level creates a Roth conversion opportunity.

If your income is above the Roth IRA limits: Ask a tax professional about the backdoor Roth and whether the pro-rata rule applies to you.

If you are between retirement and age 73: Check how much room you have in your current tax bracket and whether filling it now could reduce future RMDs.

If you are 65 or older: Confirm with your tax professional that the new senior bonus deduction is reflected in your tax plan for 2026, 2027, and 2028.

Curious how your retirement income picture stacks up against these strategies? Discover which approaches may help close your income gap before age-based deadlines narrow your options. Reach out to Langan Financial Group to discuss your situation and get a clearer view of what’s still possible.

If you are over 70 and a half and give to charity: Ask your IRA custodian about QCDs before your next distribution.

And if more than one of these applies, that is the signal that a coordinated planning conversation could be the most valuable hour you spend this year.

Langan Financial Group

Clear guidance. Coordinated planning. Calm decisions.

Schedule a Complimentary Conversation

langanfinancialgroup.com/get-started-today | 717-288-1880

DISCLOSURE: This article is provided for informational and educational purposes only and does not constitute investment advice, financial planning advice, tax advice, or legal advice. All investing involves risk, including potential loss of principal. Past performance is not a guarantee of future results.

Hypothetical scenarios are for illustrative purposes only and do not represent any specific individual’s financial situation. Actual results will vary based on individual circumstances including income levels, tax rates, account balances, and other factors. All contribution limits, tax brackets, and thresholds referenced are for the 2026 tax year unless otherwise noted, and are based on IRS Notice 2025-67 and related IRS guidance.

Limits are subject to annual adjustment. Tax law provisions referenced, including the Senior Bonus Deduction under the One Big Beautiful Bill Act, are subject to change by future legislation. The Senior Bonus Deduction is temporary and applies to tax years 2025 through 2028.

SECURE 2.0 Act provisions, including super catch-up contribution limits and mandatory Roth catch-up requirements for participants with prior-year FICA wages exceeding $150,000, are subject to IRS guidance and individual plan adoption. The 8% delayed retirement credit is set by federal law and applies to benefits claimed after full retirement age up to age 70; it is not an investment return. Social Security benefit estimates are approximate and based on general SSA formulas; actual benefits depend on individual earnings history and claiming decisions.

QCD limits are indexed annually for inflation; the 2026 limit referenced is approximate. Vanguard Advisor Alpha research is cited for educational purposes and does not guarantee specific outcomes. Pennsylvania state tax treatment of retirement income is based on current law and subject to change.

HSA contribution limits are from IRS Revenue Procedure 2025-19. HSA eligibility requires enrollment in a qualifying high-deductible health plan. Backdoor Roth IRA strategies involve the pro-rata rule and require careful tax planning; the strategy remains legal as of May 2026 but could be restricted by future legislation.

Please consult a qualified financial, tax, or legal professional before making any financial decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser.

Langan Financial Group and Cambridge are not affiliated.

Copyright 2026 Langan Financial Group. All rights reserved. | 1863 Center St., Camp Hill, PA 17011