What if the government forced you to sell stocks during a market correction?

Key Takeaways

- Starting at age 73, you must withdraw 3.8% from retirement accounts regardless of market conditions.

- Build 24-36 months of cash reserves outside IRAs to avoid forced selling during market downturns.

- Consider Roth conversions before age 73 to reduce future required distribution amounts permanently.

- Take strategic IRA withdrawals in your 60s to fill lower tax brackets before forced distributions begin.

- Missing required distributions triggers a 25% penalty on the amount you should have withdrawn.

That’s exactly what can happen when required minimum distributions collide with down markets. At age 73, you must withdraw money from your retirement accounts whether the market is up, down, or sideways. The IRS doesn’t care if your portfolio just dropped 15%.

You still owe the withdrawal. And that can create a permanent portfolio problem that compounds for years.

This correction is revealing who’s prepared for that reality and who isn’t. If you’re 58, you have 15 years to build structure before forced withdrawals begin. If you’re 68, you have 5 years. If you’re 75, the window closed, and this correction is showing whether you built the right foundation.

The Problem Most People Don’t See Coming

Here’s what catches people off guard: if you retire at 62 with $800,000 in your IRA and never touch it, letting it grow for 11 years, you could have $1.2 million by age 73.

That sounds good. Bigger number, more security. Except at 73, the IRS requires you to start taking money out.

Your first required minimum distribution on $1.2 million would be roughly $45,000. Every year. For the rest of your life.

Whether you need it or not.

If markets are up when you take that $45,000, it’s manageable. But if markets are down 15%, like during corrections, you’re selling more shares to generate the same dollars. You’re potentially locking in losses.

And those shares you sold? You don’t own them when markets recover. The impact can be lasting.

According to research from retirement planning software provider Income Lab, retirees who experience negative returns in the first three years after required distributions begin may have measurably worse outcomes than retirees who experience the same negative returns later. The forced selling during down markets can create effects that portfolios struggle to recover from.

Important Note on Examples and Projections

The following examples and calculations are hypothetical and for illustration purposes only. Actual market returns, timing, tax situations, and individual circumstances will vary significantly. There is no guarantee any strategy will achieve its objectives. Past performance does not guarantee future results.

THE POTENTIAL LIFETIME COST OF FORCED SELLING

In a hypothetical scenario, if you’re forced to sell $45,000 from a portfolio that’s down 15%, you might be selling roughly 60 more shares than you would if markets were flat.

Assuming a hypothetical 7% average annual return over 20 years, those 60 shares could potentially grow to approximately $232,000. Actual returns may be higher or lower and will vary based on market conditions.

This illustrates how forced selling during downturns could potentially reduce future portfolio growth. This isn’t primarily a market problem. It’s a structure problem that proper planning can help address.

What Forced Selling Can Look Like: A Hypothetical Example

Consider this hypothetical example: Barbara is 75 with $650,000 in her IRA. In February, before a correction, her account was $720,000. Markets dropped. Her required minimum distribution this year is $27,500, based on her December 31 balance last year.

In this scenario, Barbara doesn’t have cash reserves outside her IRA. Everything is in the retirement account. To get her $27,500, she must sell stocks from the $650,000 balance, not the $720,000 it was before the correction.

Here’s the math: $27,500 from a $650,000 account means selling 4.2% of her holdings. If markets were flat, she’d be selling 3.8%. That extra 0.4% means selling shares she wanted to keep. When markets recover, she participates with fewer shares.

If this pattern were to repeat over 3 years of volatile markets, Barbara could potentially lose $40,000 to $60,000 in portfolio value she might not recover. Not because she overspent. Not because she made bad investments. Because she didn’t have cash reserves to avoid forced selling during downturns.

The Tax Bracket Surprise: Another Hypothetical Scenario

Here’s another hypothetical example: David retired at 62 with $750,000 in his IRA. He lived off Social Security and some savings. He never touched his IRA.

His financial advisor at the time said, ‘Let it grow. You’ll thank me later.’

By age 73, David’s IRA had grown to $1.1 million. His first required distribution: $42,000. Combined with Social Security, his taxable income jumped to $68,000. He went from the 12% tax bracket to the 22% bracket.

That 10-percentage-point increase could mean David pays an extra $4,200 per year in federal taxes. Over 20 years, that could potentially total $84,000 in additional taxes.

According to research from Covisum, roughly 60% of retirees see their tax rate increase after required distributions begin. Many don’t plan for it. Many could potentially avoid it by taking smaller distributions in their 60s to fill up the lower tax brackets before the IRS requires larger withdrawals at 73.

In David’s case, the challenge wasn’t too much money. It was too much money in the wrong place at the wrong time.

The Timing Mistake: A Third Hypothetical Example

Consider Susan, age 76 in this hypothetical scenario. She has $450,000 in her IRA and $180,000 in a regular taxable investment account. Both accounts hold similar stocks. When a correction hits, both drop about 12%.

Susan needs her $17,000 required distribution. She takes it from her IRA, because that’s where required distributions come from. Makes sense, right?

Actually, she could have taken that $17,000 from her taxable account instead. Here’s why: both accounts are down 12%. But only the IRA has required distributions every year for the rest of her life.

By taking from the IRA when it’s down, she’s selling more shares than necessary. She could have preserved those IRA shares and sold from the taxable account instead.

Over 15 years of retirement, if this decision pattern were repeated during multiple corrections, it could potentially cost Susan approximately $22,000 in lost growth. She’s following the rule correctly but missing a strategic opportunity.

Important Context: These hypothetical scenarios illustrate what can happen during market corrections when proper structure isn’t in place. In stable or rising markets, required minimum distributions are typically more manageable. Many retirees never experience corrections during their first few years of required distributions. The key is building structure that protects you regardless of what market conditions you encounter.

What Actually Happens at Age 73

At 73, something fundamental changes in your retirement plan. For the previous 8, 10, or 15 years of retirement, you decided when to take money from your IRA. How much.

When. For what purpose. All your choices.

At 73, the IRS steps in. They determine the minimum you must withdraw each year using tables that estimate how long you’ll live. For most people, the first required distribution is roughly 3.8% of the account value.

That percentage increases each year as you age. By 80, it’s closer to 5%. By 85, it reaches 6.8%.

Miss your required distribution, and the penalty is 25% of the amount you should have withdrawn. Miss a $30,000 distribution, and you could owe the IRS $7,500 plus the taxes you would have paid anyway.

Your autonomy changes. The government now controls part of your financial life. And market corrections don’t change the requirement. You still owe the money.

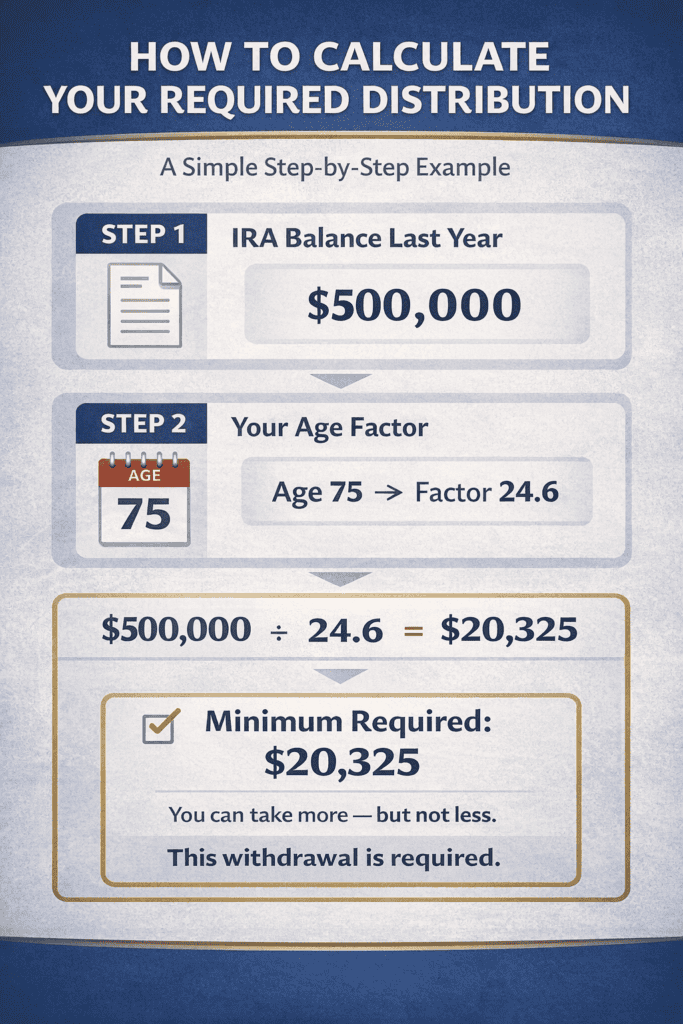

HOW TO CALCULATE YOUR REQUIRED DISTRIBUTION

Hypothetical example:

Your IRA balance on December 31 last year: $500,000

Your age this year: 75

IRS life expectancy factor at 75: 24.6

Calculation: $500,000 ÷ 24.6 = $20,325

You must withdraw at least $20,325 this year. You can take more, but not less. This is required, not optional.

How to Protect Yourself Before Age 73

The scenarios above aren’t inevitable. They can happen when people don’t build the right structure before age 73. Here’s what protection could look like, and which move may matter most based on your age.

Strategy #1: Build Cash Reserves Outside Your Retirement Accounts

This is often the most important move. According to research from the American College of Financial Services, retirees with 24 to 36 months of spending in cash outside their IRAs had 30% fewer forced selling events during market downturns.

Here’s why it can matter: when a correction hits after 73 and you owe a required distribution, you could take that money from your cash reserves instead of selling stocks. The requirement is satisfied, but you’re not potentially locking in market losses.

If Barbara from the earlier hypothetical example had $80,000 in a savings account outside her IRA, she could have taken her $27,500 distribution from cash, left her stocks alone, and let her portfolio potentially recover. Instead, she sold stocks at a loss and gave up potential future growth.

Priority by age: If you’re 55 to 70, this could be your highest priority. Consider building cash reserves now in regular savings or money market accounts, not inside your IRA.

Strategy #2: Consider Roth Conversions Before the Deadline

Money in Roth IRAs doesn’t have required distributions. Ever. Converting traditional IRA money to Roth before age 73 reduces the balance that will be subject to forced withdrawals.

Here’s a hypothetical example: Say you’re 68 with an $800,000 IRA. If you do nothing, your first required distribution at 73 would be roughly $30,000. But if you convert $100,000 to Roth over the next 5 years at $20,000 per year, your IRA at 73 is only $700,000. Your first required distribution drops to $26,500.

Cost: You pay taxes on the $100,000 you convert. If you’re in the 12% bracket, that’s $12,000 in conversion taxes over 5 years.

Potential benefit: Lower required distributions for the rest of your life. According to research from Ed Slott and Company, strategic Roth conversions during low-tax years could potentially reduce lifetime tax bills by 15% to 25% for some households. For someone with $800,000 in retirement accounts, that could represent $120,000 to $200,000 in potential tax savings, though individual results will vary significantly.

During corrections, conversions may become more valuable. If your IRA dropped 10% and you convert $50,000, you pay tax on $50,000 but you’re converting shares that might be worth $55,000 once markets potentially recover.

Priority by age: If you’re 65 to 72, this becomes more urgent. You’re potentially in your lowest-tax years, and the window closes at 73.

Strategy #3: Consider Taking Distributions Before You’re Required To

This may sound counterintuitive, but taking money from your IRA in your 60s, even when you don’t need it, can sometimes produce better long-term outcomes than waiting until 73 when the IRS forces you.

Remember David from our earlier hypothetical, who let his IRA grow from $750,000 to $1.1 million and ended up in a higher tax bracket? If David had taken $25,000 per year from his IRA between ages 65 and 73, filling up the 12% tax bracket even though he didn’t need the money, his IRA at 73 would have been $850,000 instead of $1.1 million.

His first required distribution would have been $32,000 instead of $42,000. He could have potentially stayed in the 12% bracket. Potential tax savings over 20 years: approximately $84,000, though actual results depend on many factors.

Research from financial planner Michael Kitces suggests that intentional distributions during the retirement-to-73 window, filling up lower tax brackets even when you don’t need the money, can sometimes produce better after-tax outcomes than letting the IRA grow untouched.

Priority by age: If you’re 62 to 70 and already retired, this strategy may be worth considering. If you’re still working in your 50s, waiting until retirement when your tax bracket drops may make more sense.

Already Past 73? Here’s How to Potentially Minimize the Impact

If you’re already taking required distributions, the planning window closed. But you still have tactical decisions that can matter during corrections.

Tactic #1: Choose Which Account to Pull From If you have multiple IRAs, you can take your total required distribution from whichever account makes the most sense. If one IRA is down 15% and another is down only 5%, consider taking the full distribution from the one that’s down less. You’re required to take the money, but you get to choose which shares you sell.

Tactic #2: Consider Timing Your Distribution Strategically Required distributions must be completed by December 31, but you can take them in January or November. During correction years, waiting until later in the year may give your portfolio more time for potential recovery. If markets dropped in March but stabilized by October, you might be selling at better prices.

The risk is waiting too long and forgetting. The penalty is severe. But if you’re organized, timing can potentially help.

Tactic #3: Build Reserves Going Forward Even after 73, you can build cash reserves. If you don’t need your full required distribution for spending, consider putting the excess in a savings account outside your IRA. Over 2 to 3 years, you build a buffer.

Then when the next correction hits, you can potentially take your required distribution from that cash buffer instead of selling stocks. You’re building the structure you wish you’d had before 73.

Tactic #4: Consider Qualified Charitable Distributions Once you’re 70½, you can send up to $100,000 annually (indexed for inflation, may be higher in current year) from your IRA directly to charity. This counts toward your required distribution but doesn’t show up as taxable income. If you’re charitably inclined and your distribution pushes you into a higher tax bracket, this could potentially save thousands in taxes. According to research from Fidelity Charitable, roughly 23% of donors over 70 use this strategy, though many don’t maximize it.

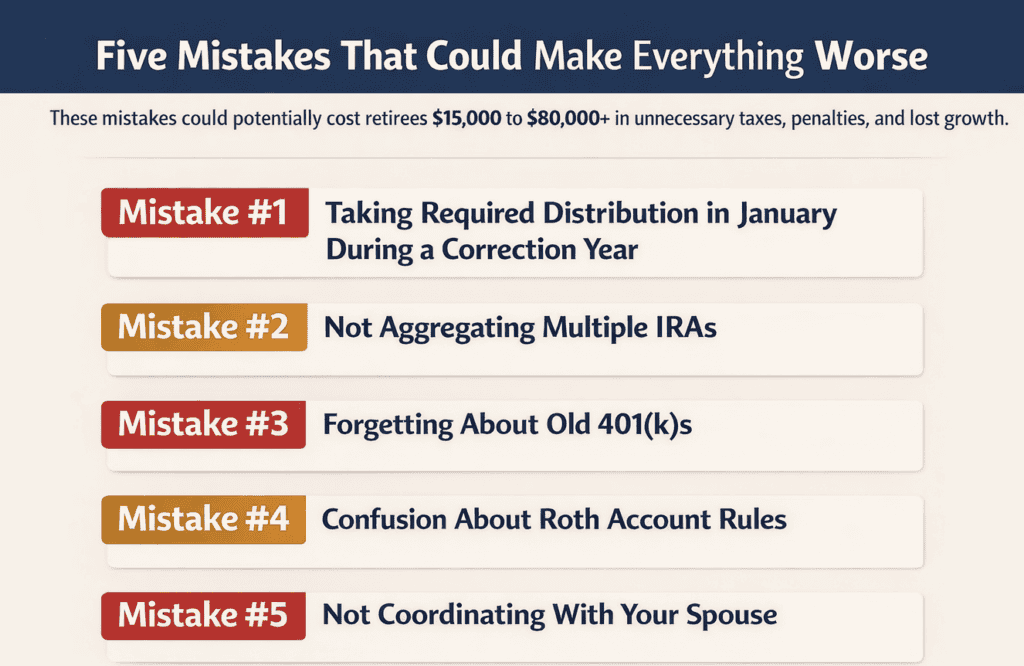

Five Mistakes That Could Make Everything Worse

These mistakes could potentially cost retirees $15,000 to $80,000+ in unnecessary taxes, penalties, and lost growth, though actual costs vary by individual circumstances:

Mistake #1: Taking Your Required Distribution in January During a Correction Year

Potential cost: If you take your distribution in January and markets fall 12% in March, you sold before the drop. Waiting until November might mean selling at better prices after some recovery. For a hypothetical $500,000 portfolio, taking the distribution 10 months later after partial recovery could potentially save you from selling 30 to 40 extra shares. Over 20 years of hypothetical growth at 7% annually, those shares could potentially be worth $12,000 to $18,000, though actual returns will vary.

Mistake #2: Not Aggregating Multiple IRAs

Strategic opportunity: If you have three IRAs worth $200,000, $150,000, and $100,000, your total required distribution is based on $450,000. But you don’t have to take proportional amounts from each account. You can take the entire amount from just one IRA. Many people don’t realize this and take from all three, missing the chance to be strategic about which shares they sell during corrections.

Mistake #3: Forgetting About Old 401(k)s

Potential cost: Required distributions apply to 401(k)s too. If you have an old 401(k) from a previous employer, you must take distributions from it separately. You can’t aggregate 401(k)s with IRAs.

Many people forget about old 401(k)s and miss required distributions. The penalty: 25% of the missed amount. Missing a hypothetical $15,000 distribution from a forgotten 401(k) could result in a $3,750 penalty.

Mistake #4: Confusion About Roth Account Rules

Clarification: Roth IRAs don’t have required distributions. Ever. As of 2024, the SECURE 2.0 Act also eliminated required minimum distributions from Roth 401(k)s. Previously, Roth 401(k)s had RMDs unless rolled to a Roth IRA, but this is no longer the case.

Mistake #5: Not Coordinating With Your Spouse

Potential impact: If both spouses have IRAs and both are over 73, both owe required distributions. Combined, those distributions might push you into a higher tax bracket or trigger Medicare premium surcharges. Strategic coordination, like taking one spouse’s distribution from cash reserves during correction years, could potentially save thousands annually.

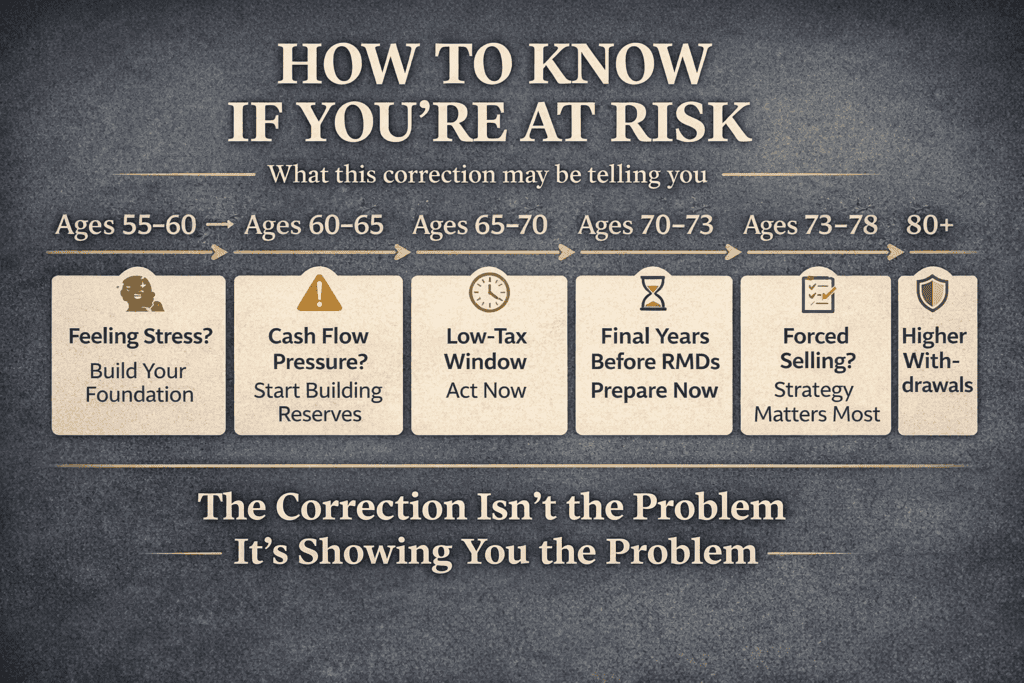

How to Know If You’re At Risk

This correction can be diagnostic. It may reveal whether your structure works under stress. Here’s what to look for based on your age:

Ages 55 to 60: If this correction stressed you out, use that information. You have 13 to 18 years before required distributions begin. That’s enough time to build strong structure: multiple years of cash reserves, significant Roth balances, diversified income sources.

The anxiety you feel now is feedback. It’s suggesting you may want to build better buffers.

Ages 60 to 65: If this correction created cash flow pressure, that’s a warning sign. You have 8 to 13 years before forced distributions. If corrections stress your cash flow now, required distributions could amplify that pressure later. This is your window to build reserves outside retirement accounts and consider increasing Roth conversion activity.

Ages 65 to 70: You’re in the golden window. These are often your lowest-tax years. If this correction stressed your cash flow, that’s urgent information.

You have 3 to 8 years to build better structure before required distributions start. Every year you delay could be a year you won’t get back. This may be your last chance to build cash reserves, do Roth conversions, and position yourself for forced distributions.

Ages 70 to 73: Final countdown. If this correction forced difficult choices, you’re in the last years before the IRS requires withdrawals. You have 0 to 3 years to build cash reserves outside retirement accounts, complete strategic Roth conversions, and position yourself. The correction may be showing you whether your current path leads to flexibility or forced selling.

Ages 73 to 78: If this correction forced you to sell stocks you wanted to hold to satisfy your required distribution, that could reveal insufficient preparation. You entered the distribution years without adequate buffers. The correction isn’t the problem.

It’s the messenger. The problem may be the structure. The good news: you can still build cash reserves going forward using the tactics above.

It’s harder after 73 than before, but not impossible.

Ages 80+: Required distributions are taking 6% to 7% of your portfolio each year. Corrections can hit harder because your distribution percentage is higher, which means more potential forced selling during downturns. This is when qualified charitable distributions, strategic account selection, and building non-IRA cash reserves may matter most.

The structure decisions you made at 68 can determine how manageable life is at 82. But even at 80+, tactical improvements can still help.

What This Means For You

You can’t avoid age 73. But you can potentially control what happens when you get there.

If you’re 58, you have 15 years to build structure before the IRS requires withdrawals. That’s 15 tax years to potentially convert to Roth, 15 years to build cash reserves, 15 years to position yourself for success instead of stress. Many people defer these decisions thinking 73 is too far away to worry about. Then they turn 73 and realize they’re facing forced selling during corrections with limited options.

If you’re 68, you have 5 years. Not 15. Five.

Every year you delay building cash reserves or doing Roth conversions is one year closer to the deadline with less room to maneuver. This isn’t distant planning anymore. This could be urgent.

If you’re 75, that window closed. But the tactical decisions you make today, which account to pull from, when to take your distribution, how to build reserves going forward, can still influence whether the next 15 years feel manageable or overwhelming. The structure challenges may be harder to address, but you’re not powerless.

Market corrections don’t create these problems. They reveal them. The people who handle corrections without forced selling are often the people who built the right structure before age 73.

They have cash reserves. They did Roth conversions when their tax brackets were low. They took intentional distributions to fill lower brackets before the IRS required larger withdrawals.

The people who struggle during corrections are sometimes the people who thought they had time, didn’t build structure, and crossed into required distributions without adequate protection.

The question isn’t whether required distributions are coming. It’s whether you’ll be ready when they arrive.

How To Find Help

Not sure if your current structure protects you from forced selling at age 73? We can review your numbers: current IRA balance, projected required distributions, tax bracket impact, and cash reserve gaps. You’ll see what age 73 might look like with your current structure, and what changes could potentially make a difference.

If you’re between 65 and 72, this type of planning has a natural time limit. After 73, you’re managing requirements instead of preventing challenges.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.