One of the most important decisions you’ll make about your retirement savings is whether to contribute to traditional (pre-tax) or Roth retirement accounts. This choice affects not only your current tax bill but also your financial flexibility and tax burden throughout retirement.

Understanding the differences between these two approaches can help you optimize your retirement planning strategy and potentially save thousands of dollars in taxes over your lifetime.

The decision isn’t always straightforward, and the best choice often depends on your current income, expected future tax rates, and retirement timeline. Many people can benefit from using both types of accounts strategically, creating tax diversification that provides flexibility in retirement.

Understanding Pre-Tax vs. Roth Contributions

Pre-tax contributions go into traditional retirement accounts like 401(k)s and traditional IRAs. These contributions reduce your current taxable income, lowering your tax bill today. However, when you withdraw the money in retirement, both your contributions and any growth are taxed as ordinary income.

Roth contributions are made with after-tax dollars to Roth 401(k)s and Roth IRAs. You don’t get a tax deduction today, but qualified withdrawals in retirement are completely tax-free, including all the growth your money has earned over the years.

The fundamental trade-off is simple: pay taxes now (Roth) or pay taxes later (traditional). But determining which is better for your situation requires looking at several factors that are part of comprehensive tax planning services.

The Tax Bracket Consideration

Your current tax bracket compared to your expected retirement tax bracket is the most important factor in deciding between Roth and traditional contributions.

If you’re in a high tax bracket today and expect to be in a lower bracket in retirement, traditional contributions usually make more sense. You get a valuable tax deduction now and pay taxes later at lower rates.

If you’re in a lower tax bracket today than you expect to be in retirement, Roth contributions are typically better. You pay taxes at current low rates and avoid higher taxes later.

If you expect to be in a similar tax bracket in retirement, other factors like required minimum distributions and estate planning goals become more important in the decision.

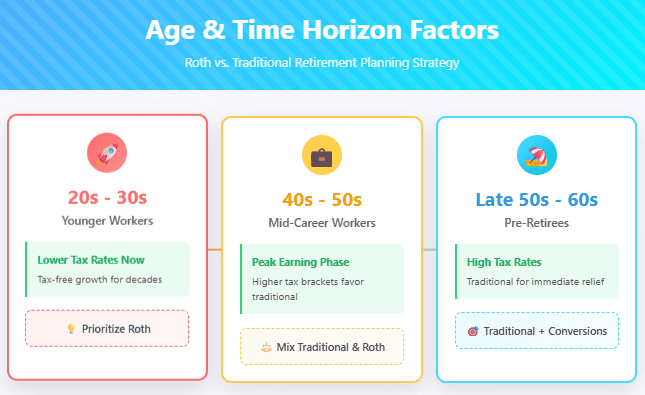

Age and Time Horizon Factors

Your age and how long until retirement significantly impact the Roth vs. traditional decision:

Younger Workers (20s and 30s): Generally benefit more from Roth contributions because they typically have lower incomes (and tax rates) now, plus decades for tax-free growth to compound. Even if they’re in higher tax brackets later in their careers, the long-term tax-free growth often outweighs the immediate tax savings of traditional contributions.

Mid-Career Workers (40s and 50s): Often in their peak earning years with higher tax brackets, making traditional contributions more attractive for the immediate tax savings. However, Roth contributions can still make sense if they expect higher retirement income or want to minimize required distributions.

Pre-Retirees (Late 50s and 60s): Traditional contributions often provide more immediate benefit due to high current tax rates, but Roth IRA conversions might be attractive in early retirement years when income is lower.

Income Levels and Contribution Limits

Your income level affects both the tax benefits and your eligibility for different types of accounts:

High-Income Earners: Get more value from traditional contributions due to higher tax brackets. However, they may be limited in their Roth IRA contribution eligibility due to income limits and should consider high-income retirement strategies.

Moderate-Income Earners: Have the most flexibility and can often benefit from either approach. This group should focus on projected future tax brackets and retirement goals.

Lower-Income Earners: Often benefit more from Roth contributions due to lower current tax rates, though they might also benefit from the Saver’s Credit available for traditional contributions.

Required Minimum Distributions

Traditional retirement accounts require you to start taking minimum distributions at age 73, whether you need the money or not. These required minimum distributions (RMDs) can push you into higher tax brackets and force you to pay taxes on money you might prefer to leave invested.

Roth IRAs don’t have required minimum distributions during your lifetime, giving you complete control over when and how much you withdraw. This flexibility can be valuable for:

- Managing tax brackets in retirement

- Preserving assets for estate planning

- Maintaining eligibility for income-based benefits

- Avoiding the taxation of Social Security benefits

Estate Planning Considerations

Roth accounts offer superior estate planning benefits:

Tax-Free Inheritance: Your heirs receive Roth accounts tax-free, while inherited traditional accounts are taxable to beneficiaries.

No RMDs: Since Roth IRAs don’t require distributions during your lifetime, you can leave larger amounts to heirs.

Flexibility for Beneficiaries: Inherited Roth accounts provide tax-free growth and distributions, giving your beneficiaries more financial flexibility.

If leaving money to heirs is important to you, Roth contributions and conversions can be powerful estate planning tools.

The Power of Tax Diversification

Rather than choosing exclusively between Roth and traditional contributions, many people benefit from tax diversification – having money in both types of accounts.

Tax diversification provides several advantages:

Flexibility in Retirement: You can choose which accounts to withdraw from based on your tax situation each year, potentially keeping yourself in lower tax brackets.

Hedge Against Tax Rate Changes: If future tax rates are higher than expected, you have tax-free Roth money. If they’re lower, you have traditional accounts to withdraw from at favorable rates.

Managing Other Income: You can coordinate withdrawals with Social Security, pension income, and required minimum distributions to optimize your overall tax picture.

Employer Match Considerations

If your employer offers matching contributions to your 401(k), always contribute enough to get the full match first, regardless of whether you choose Roth or traditional contributions. The employer match is free money that provides an immediate 100% return on your contribution.

Employer matching contributions always go into the traditional (pre-tax) side of your account, even if your own contributions are Roth. This automatically provides some tax diversification in your 401(k).

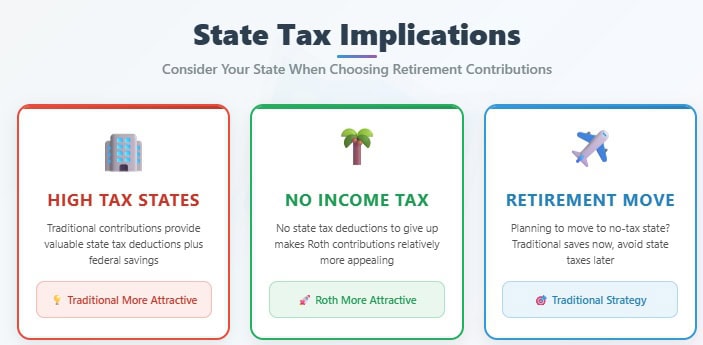

State Tax Implications

Don’t forget about state taxes in your decision:

High State Tax States: Traditional contributions can provide valuable state tax deductions in addition to federal tax savings.

States with No Income Tax: The lack of state income tax makes Roth contributions relatively more attractive since you’re not giving up state tax deductions.

Retirement State Planning: If you plan to move to a state with no income tax in retirement, traditional contributions might be more valuable since you’ll avoid state taxes on retirement withdrawals.

Social Security Tax Implications

The type of retirement accounts you withdraw from can affect whether your Social Security benefits are taxable:

Traditional Account Withdrawals count as income for Social Security taxation purposes and can cause up to 85% of your Social Security benefits to become taxable.

Roth Account Withdrawals don’t count as income for Social Security taxation, potentially keeping more of your Social Security benefits tax-free.

This factor can be significant for retirees who want to minimize taxes on their Social Security benefits and implement effective Social Security planning strategies.

Practical Strategies for Different Situations

Starting Your Career: Focus on Roth contributions while your income and tax bracket are relatively low. You have decades for tax-free growth to compound.

Peak Earning Years: Consider traditional contributions for the immediate tax savings, but don’t ignore Roth options entirely. Some tax diversification is usually beneficial.

Approaching Retirement: Traditional contributions often provide more immediate benefit, but consider Roth conversions in early retirement when your income might be lower.

Variable Income: If your income fluctuates significantly, adjust your contribution strategy accordingly. Use traditional contributions in high-income years and Roth in lower-income years.

Common Decision-Making Mistakes

All-or-Nothing Thinking: Many people think they must choose exclusively between Roth and traditional. Tax diversification through both types of accounts is often the best approach.

Ignoring Future Tax Rates: Focusing only on current tax brackets without considering future tax policy changes or personal income changes.

Forgetting About State Taxes: State tax considerations can significantly impact the optimal choice, especially if you plan to move in retirement.

Not Maximizing Employer Match: Failing to contribute enough to get the full employer match is leaving free money on the table.

Paralysis by Analysis: Spending so much time trying to optimize the choice that you delay starting to save. Starting with either option is better than not saving at all.

If I Need Help Determining Roth vs. Traditional Contribution Strategies

The Roth vs. traditional decision involves complex interactions between current taxes, future tax projections, estate planning, and retirement income planning. A fee-only financial advisor can help you:

- Model different scenarios based on your specific situation

- Consider the interaction with other parts of your financial plan

- Develop a strategy that adapts as your circumstances change

- Optimize your overall retirement tax strategy

The Roth vs. traditional decision is important, but it’s not permanent. You can adjust your strategy over time as your income, tax situation, and retirement goals evolve. The most important thing is to start saving consistently, regardless of which type of account you choose.

Ready to determine the best retirement contribution strategy for your unique situation? Contact our team to schedule a consultation and develop a personalized retirement savings plan that optimizes your tax strategy and helps you achieve your financial goals.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 9 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.