You did everything right. Filed the same way you always do. Same income, same deductions, same withholding.

But instead of your usual $2,000 refund, you owe $7,200.

What the hell happened?

If you’re one of the thousands getting hit with surprise tax bills this filing season, you’re not crazy—and you’re not alone. The shock is real. But here’s the part nobody warned you about: this isn’t because your taxes went up. It’s because of a timing mismatch created by legislation most people didn’t know existed.

The One Big Beautiful Bill Act—And Why It Blindsided Everyone

In July 2025, Congress passed the One Big Beautiful Bill Act (OBBBA). It made many 2017 Tax Cuts and Jobs Act (TCJA) provisions permanent (keeping lower tax brackets and higher standard deductions) and added new temporary breaks for 2025–2028, including:

- A new $6,000 senior deduction ($12,000 joint for both 65+).

- Increased Child Tax Credit to $2,200 per child under 17.

- Deductions for up to $25,000 in tips and $12,500 in overtime pay ($25,000 joint).

- Up to $10,000 deduction for interest on loans for American-made vehicles.

- Higher SALT deduction cap to $40,000 (for MAGI under $500,000).

- New “Trump Accounts” for kids (tax-deferred savings, with $1,000 government seed for births 2025–2028).

The problem? Most changes are retroactive to January 1, 2025. Your withholding all year was based on the old, higher tax rules. But when you filed your return, the IRS used the new, lower rates and added deductions.

That sounds helpful—but if your withholding was set too low under the old rules (or income pushed you past phaseouts), you underpaid and now owe.

A Hypothetical Example

A couple, both 67, with $140,000 income (401(k) withdrawals, Social Security, investments). Withholding was set for old rates; new senior deduction helped but didn’t cover enough. They owe $6,800 because:

- 401(k) withholding too low.

- No withholding on Social Security or investments.

- Phaseout reduced full senior benefit.

The IRS doesn’t care about the mismatch—you owe the difference.

Already Filed and Owe Money? Here’s What Happens Next

You’ll get an IRS notice in 4–6 weeks. Pay by April 15, 2026, to avoid penalties (0.5%/month up to 25%) plus interest (currently 7% compounded daily).

Options if you can’t pay full: short-term plan (180 days), long-term installment ($31–$130 setup), Currently Not Collectible, or Offer in Compromise (rare for hardship).

What You Need to Do Before April 15

- Pay what you owe — Even partial payment now reduces penalties. Use IRS.gov/payments (free bank transfer).

- File extension if needed — Form 4868 (free, online) gives until October 15 to file—but pay estimated owed by April 15.

- Fix 2026 withholding now — New W-4 (employer), increase to 20–25% on 401(k)/IRA, W-4V for Social Security (12–22%). Use IRS Withholding Estimator.

- Check state taxes — Pennsylvania exempts most retirement income; others may not follow federal changes.

- Verify senior deduction eligibility — 65+ by Dec 31, 2025; MAGI under $75k single/$150k joint for full benefit.

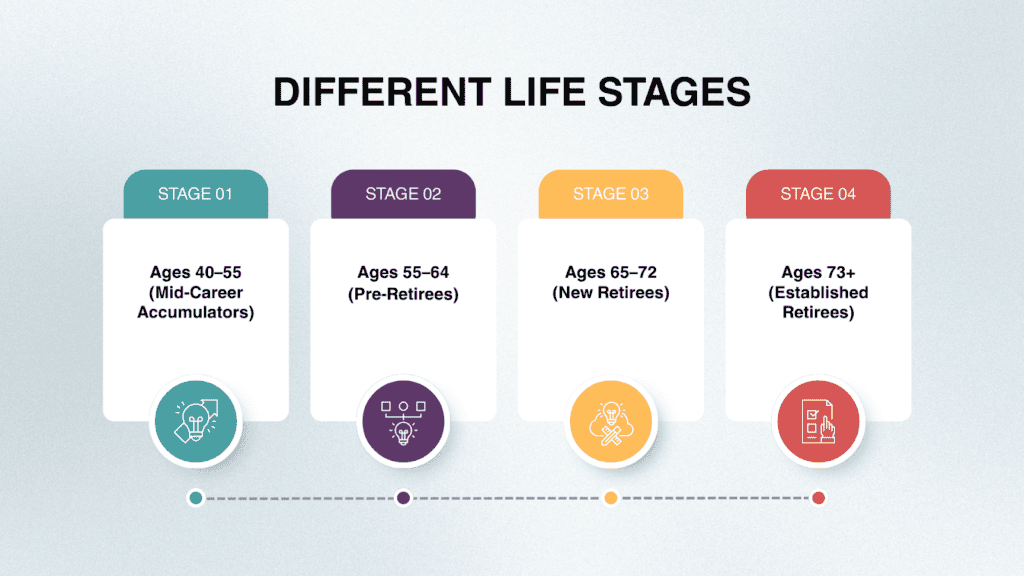

How This Hits Different Life Stages

Ages 40–55 (Mid-Career Accumulators)

Minimal direct OBBBA impact (no senior deduction), but surprises from tips/overtime deductions (up to $25k/$12.5k, phaseout over $150k single/$300k joint), car loan interest ($10k max, phaseout over $100k single/$200k joint), or higher CTC ($2,200/child). No withholding on tips/overtime often causes underpayment.

What you could do: Quarterly estimates (1040-ES) for non-W-2 income. Start Roth contributions to avoid future phaseouts.

Ages 55–64 (Pre-Retirees)

No senior deduction yet, but bridge income (early withdrawals, part-time) + new deductions (tips/overtime/car loans) can cause mismatches. Higher CTC helps if you have kids.

What you could do: Quarterly estimates. Roth conversions in gap years (low income before Social Security/RMDs).

Ages 65–72 (New Retirees)

Full senior deduction eligibility, but surprises from uncoordinated withholding on SS/401(k)/investments + phaseouts. New car loan/tips deductions may apply.

What you could do: Withhold aggressively (20–25% on distributions, 12–22% on SS). Roth conversions before RMDs.

Ages 73+ (Established Retirees)

RMDs push income up, potentially phasing out senior deduction and triggering Medicare IRMAA (surcharges over $109k single/$218k joint MAGI for 2026).

What you could do: Withhold 25–30% on RMDs. Use QCDs (up to $111,000 in 2026) to satisfy RMD tax-free, stay under phaseouts/IRMAA.

The Hidden Opportunity: Use Lower Rates for Long-Term Moves

OBBBA keeps TCJA brackets lower through 2028—ideal for Roth conversions (pay now at lower rates for tax-free growth/heirs). Who should: Income under $150k, long horizon. Skip if high income or need funds soon. Also consider capital gains harvesting in 0% bracket ($96,700 joint taxable income 2025).

Conversations We’re Having With Clients

Here are some of the ideas we’re sharing with clients that can help them with their situation. As always, always seek professional help before you take action. Pay owed now, fix withholding this week, use lower rates for Roth/QCDs. Don’t DIY complex income—get help.

Key Tax Deadlines to Watch

- April 15, 2026: File/extend 2025 return, pay owed; first 2026 estimated payment.

- June 16, September 15, 2026; January 15, 2027: Estimated payments.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal, financial, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.