If you’ve been watching economic headlines, you likely saw: the Fed recently cut its benchmark interest rate. This move isn’t just a macro-story—it carries practical consequences for your investments, income planning, and broader financial strategy.

Let’s walk through what the rate cut means now, the remaining uncertainties, and some smart strategies you may want to consider.

Why a Rate Cut Changes the Game

Lowering interest rates ripples through the financial ecosystem in several ways:

- Bonds and fixed-income behave differently: When rates fall, existing bonds (especially longer-dated ones) often rise in value. But if you’re holding very short-term bonds or cash equivalents, you may not benefit from that rebound.

- Cash and short-term instruments become less attractive: With yields declining, the opportunity cost of holding cash rises (especially when inflation remains elevated).

- Equity markets may respond with optimism—but caution is warranted: A rate cut can stimulate growth, but it can also signal that the economy is weakening, which raises risk for markets.

Latest data & context:

- At its October 29 2025 meeting, the Fed cut its policy rate by 25 basis points, lowering the target range to 3.75%–4.00%.

- The yield on the 10-year Treasury note is around 4.08%–4.11% as of Oct 30–31.

- The spread between the 10-year and 2-year Treasuries is about 0.50 percentage points (i.e., still positive).

- Markets had priced in near-100% odds of the cut to 3.75%–4% and had also expected another cut in December (~71% after the meeting).

- The Fed statement notes “uncertainty about the economic outlook remains elevated” and “downside risks to employment rose in recent months.”

In short: yes — there are opportunities in a lower-rate world. But there are also risks: slower growth, higher volatility, lower income from “safe” assets.

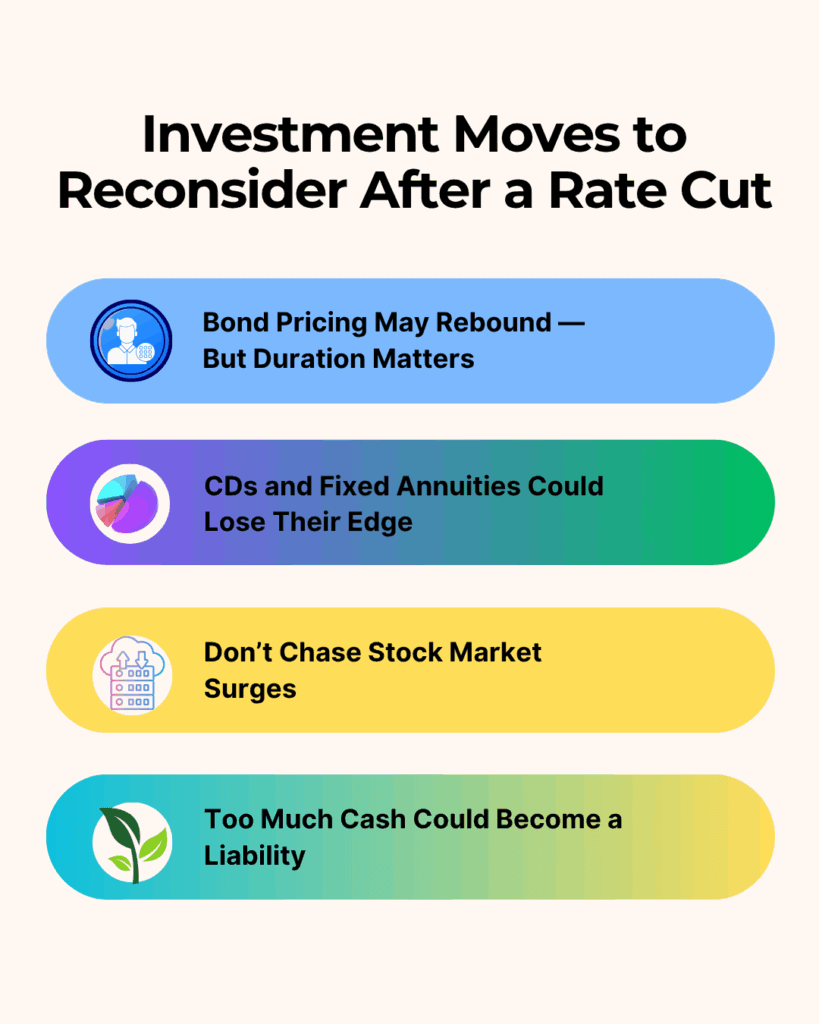

Investment Moves to Reconsider After a Rate Cut

Bond Pricing May Rebound — But Duration Matters

With lower rates, existing bonds (especially longer duration ones) may see price gains. However:

- If you’re holding very short-term maturities or ultra-low risk investments, you may miss much of the upside.

- Consider shifting toward intermediate duration bonds or laddered maturities — balancing risk vs return rather than simply chasing the best yield.

Cash, CDs & Fixed Annuities Could Lose Their Edge

In a declining-rate environment, the high yields once offered by money market funds, CDs and newer fixed annuities may shrink.

Planning tip: If you’ve been waiting patiently for “just the right yield,” now might be the time to evaluate income tools while rates remain relatively elevated — but also prioritise liquidity and flexibility.

Don’t Chase Stock Market Surges Blindly

It’s tempting to believe “rate cut → stocks go up.” But when the cut is motivated by concerns about growth or employment rather than signal strength, the initial rally may reverse. Historically, the full impact of a cut can take 6-12 months to play out.

Actionable guidance: Maintain diversification across sectors and investment styles. Avoid over-concentration in sectors (e.g., speculative tech) just because they “pop” on the news.

Too Much Cash Could Become a Liability

High‐yield savings and money market funds have been strong cushions. But with yields falling and inflation still elevated (~3% or more in some readings), holding large amounts of cash may erode purchasing power.

Action step: Keep enough liquidity for short‐term needs, but consider reallocating excess toward more growth-oriented or tax-efficient vehicles.

Broader Planning Impacts You Might Not Have Considered

Retirement Income & Withdrawal Planning

If your income plan assumed 4–5% returns from fixed-income assets, a sustained lower-rate environment may squeeze that assumption.

Proactive step: Run updated projections with lower yield assumptions (e.g., using Treasury 10-yr yield ~4% as a benchmark) and consider adjusting withdrawal rates or maintaining more growth exposure.

Roth Conversions and Tax Planning

With tax law changes looming (2026 and beyond) and rate uncertainty rising, converting to a Roth IRA still makes sense—especially in years with lower taxable income or temporary dips.

Smart move: Use the rate-cut environment as one factor in timing conversions—but always align with income, tax, and withdrawal strategy.

Estate Planning and Interest-Sensitive Tools

Interest-rate drops affect more than investing—they also impact estate and gifting strategies. For instance, the IRS §7520 rate (used in many trust/gift valuations) declines when interest rates fall, making certain estate planning strategies more attractive.

If you’re high net-worth: Review your estate/gifting tools with your advisor while interest-rate assumptions remain favourable.

What This Means for the Market — and Your Future

It’s important to stay grounded. While a rate cut often triggers a positive headline, the broader context matters:

- The first cut can be a sign of economic cooling, not economic strength.

- Bond yields (e.g., 10-year Treasuries) are still around ~4.1% and have only moved modestly.

- Markets are pricing in further cuts, but Fed officials remain cautious due to inflation that still runs above the 2% target.

- The yield‐curve (10-yr minus 2-yr) remains positive (~0.5pp) but is compressed — a historically unreliable but noteworthy indicator of growth expectations.

For investors and pre-retirees, this is not a time to “set and forget.” It’s a time for clarity, flexibility, and scenario planning.

What Does the Fed Cut Mean For Me?

- Don’t assume falling rates mean “everything gets better.” Take the time to review your portfolio, income plan and underlying assumptions.

- Lower safe-asset yields mean you may need to adjust expectations or maintain more growth risk (within your risk tolerance).

- Roth conversions, charitable giving strategies (like QCDs), and estate/gifting plans may gain extra leverage in this window.

- Excess cash may feel safe—but it may silently erode value under inflation and declining yields.

So What Do I Do?

The Fed’s rate cut is more than a headline—it’s a signal that the financial world is shifting. For those near or in retirement (or managing high-net-worth portfolios), it means one thing: review, reflect and adjust. Your plan should match reality, not just your assumptions.

If you haven’t revisited your income strategy or portfolio in light of this change, now is an ideal time.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.