Investment firms don’t typically advertise this, but the mutual fund you own likely comes in several different “flavors”—and the one you’re sold might not be the cheapest option available.

These different versions, called share classes, contain identical underlying investments but charge dramatically different fees.

It’s like buying the same car with different financing terms, except most investors never realize they had options. Let’s decode this system so you can ensure you’re not overpaying for the same investment performance.

The Share Class System: Same Fund, Different Price Tags

Think of mutual fund share classes as membership tiers at the same club. You get access to the same amenities (the fund’s investment portfolio), but your membership fees vary based on which entrance you use and how the club gets paid.

Here’s how the major classes typically work:

| Share Class | Upfront Cost | Annual Fees | Best For | Key Feature |

|---|---|---|---|---|

| Class A | 3-5% Load | 0.7-1.2% | 7+ Year Holdings | Front-loaded Savings |

| Class C | None | 1.3-2.0% | Short-term (rare) | No Initial Commitment |

| Class I | None | 0.4-0.8% | High Net Worth | Lowest Ongoing Cost |

| Class R | Varies | Plan Dependent | 401(k) Participants | Employer Negotiated |

Class A Shares: Pay Now, Save Later

- The deal: Pay a 3-5% commission upfront, get lower ongoing fees

- Annual expenses: Usually 0.7-1.2%

- Best for: Long-term investors who plan to hold for 7+ years

- The math: That upfront fee gets diluted over time by lower annual costs

Class C Shares: No Upfront Cost, Higher Long-Term Price

- The deal: No initial commission, but higher annual fees

- Annual expenses: Often 1.3-2.0% or more

- Hidden catch: May include a 1% fee if you sell within the first year

- Best for: Shorter holding periods (though this is rarely optimal for retirement planning)

Class I Shares: The VIP Option

- The deal: Lowest ongoing costs, but higher account minimums

- Annual expenses: Typically 0.4-0.8%

- Access requirements: Often $500,000+ unless purchased through an advisor

- Best for: High-net-worth investors or those working with fee-only advisors

Class R Shares: The 401(k) Special

- The deal: Designed for retirement plans, fees vary widely

- Annual expenses: Range from reasonable to expensive depending on plan size

- Note: Your HR department’s negotiating power affects what you pay

The Compound Effect of Fee Differences

Small percentage differences create massive long-term impacts. Consider this scenario based on a $500,000 portfolio over 20 years with 7% gross returns:

- High-fee scenario (1.5% annual expenses): $1,620,000 final value

- Low-fee scenario (0.5% annual expenses): $1,970,000 final value

- The difference: $350,000

That’s more than two-thirds of your original investment—lost not to market risk, but to avoidable fees.

For retirement planning, this matters enormously. An extra $350,000 represents years of additional financial security or significant legacy enhancement. It’s the difference between a comfortable retirement and a truly secure one.

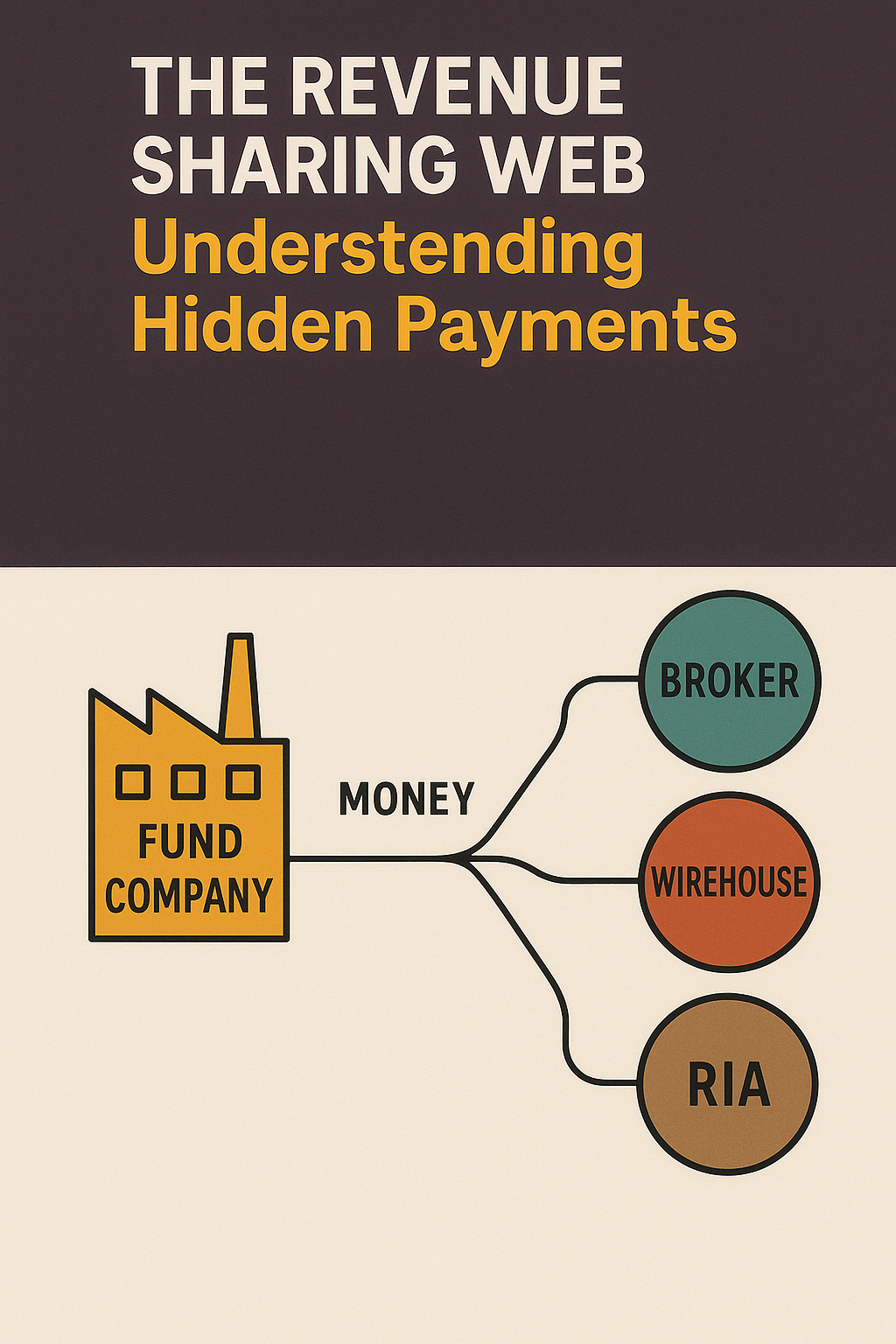

The Revenue Sharing Web: Understanding Hidden Payments

Here’s where the system gets murky. Many fund companies pay brokers, wirehouses, and even some RIAs a portion of the fees you’re charged. These “revenue sharing” arrangements are legal but create obvious conflicts of interest.

How it works: You pay 1.2% annually for a Class C share. The fund company might pay your broker 0.25% of that for bringing them your business. Suddenly, your broker has a financial incentive to recommend the more expensive option.

The disclosure challenge: These payments are often buried in lengthy prospectuses or disclosed separately from investment recommendations.

The fiduciary difference: Fee-only, fiduciary advisors typically avoid these arrangements entirely, focusing instead on securing the lowest-cost share classes available to you.

Cost Transparency: What to Look For

| Fee Type | What It Is | Typical Range | Where to Find |

|---|---|---|---|

| Expense Ratio | Annual fee percentage | 0.4-2.0% | Fund prospectus |

| 12b-1 Fees | Marketing charges | 0.25-1.0% | Fee disclosure |

| Sales Loads | Commission charges | 0-5.75% | Investment statement |

| Advisory Fees | Advisor compensation | 0.5-1.5% | Separate disclosure |

Your investment statements and fund prospectuses contain this information, but you need to know where to look:

Expense Ratio: The annual fee percentage (this is your primary concern)

12b-1 Fees: Ongoing marketing charges (often 0.25-1.0% annually)

Sales Loads: Front-end or back-end commission charges

Advisory Fees: What you pay your advisor (separate from fund expenses)

Pro tip: Services like Morningstar’s fund screener or FeeX can help you analyze your current costs and identify lower-fee alternatives.

Strategic Implications for Retirement Investors

Fee optimization becomes even more critical as you approach and enter retirement for several reasons:

Sequence of returns risk: High fees compound the damage during market downturns when you’re taking withdrawals.

Tax efficiency: Lower-cost funds often have lower turnover, generating fewer capital gains distributions in taxable accounts.

Income replacement: Every dollar saved on fees is another dollar available for retirement income.

Legacy preservation: Lower fees mean more wealth available for heirs or charitable giving.

Many retirees discover they could increase their sustainable withdrawal rate by 0.2-0.5% annually simply by optimizing their fund expenses—equivalent to having significantly more assets.

The Right Questions for Your Financial Professional

Don’t be afraid to ask direct questions about costs and compensation:

- “What share class am I currently in, and are lower-cost versions available?”

- “How are you compensated on these specific investments?”

- “Do you receive any revenue sharing or 12b-1 payments from fund companies?”

- “If I qualify for institutional share classes, why aren’t we using them?”

- “Can you show me the total cost breakdown including all fees?”

These conversations reveal whether your advisor prioritizes your financial outcomes or their compensation structure.

Implementation Strategy: Making the Switch

If you discover you’re in higher-cost share classes, the solution isn’t always immediate. Consider:

Tax implications: Switching funds in taxable accounts may trigger capital gains

Timing: Markets don’t pause for fee optimization—coordinate changes thoughtfully

Account type: IRAs and 401(k)s allow changes without immediate tax consequences

Minimum requirements: Ensure you meet requirements for lower-cost share classes

Often the best approach: Work with a fiduciary advisor who has access to institutional pricing and can navigate these transitions tax-efficiently.

The Bottom Line

Fund share classes represent one of the few areas in investing where you have direct control over costs without sacrificing investment quality. The same portfolio management, the same underlying securities, but potentially dramatically different long-term outcomes based on which “version” you own.

Given that most retirement portfolios hold funds for decades, optimizing share classes isn’t just about saving money—it’s about securing your financial future. The difference between expensive and efficient fund classes could determine whether you leave a legacy or leave your heirs wondering what happened to your wealth.

Next time you review your investment statements, look beyond the account balances. Check those expense ratios. Question those share classes. Your future self will thank you.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.