It’s a Good Reaction at the Wrong Time

Thirty years of data tell a consistent story: the average investor significantly underperforms the investments they own. Not because of poor fund selection. Because of what they do when those funds fall.

This Is Not a Normal Week

Oil prices are up more than 40% in two weeks. The jobs market stumbled badly in February, losing 92,000 positions where economists expected gains. The Federal Reserve is frozen; unable to cut rates to support growth without risking a new inflation surge from elevated energy costs. Markets are unsettled. Geopolitical risk is elevated in ways that feel genuinely different from recent memory.

Weeks like this one produce a specific, familiar feeling. Something has changed. The news is alarming. The instinct to act, to protect, to do something feels not just reasonable but responsible.

That feeling is worth examining carefully, because it is precisely the feeling that has produced the most consistently destructive investor behavior across every volatile period in the last three decades.

The Number That Changes How You Think About Risk

8.48%

The gap between the average equity investor’s return and the market’s return in 2024. Source: DALBAR Quantitative Analysis of Investor Behavior, 2025. Not caused by bad funds. Caused entirely by behavior.

Every year since 1994, independent research firm DALBAR has measured the difference between what the stock market returns and what the average investor actually earns. The results have been remarkably consistent and remarkably sobering.

In 2024, a year when the market delivered strong performance, the average equity fund investor underperformed the market by 8.48 percentage points. The year before, the gap was similar. The year before that, the same. This is not a fluke of one bad year. It is a persistent, measurable, 30-year pattern.

The critical insight from DALBAR’s research is what causes the gap. It is not bad fund selection. It is not high fees, though those matter. It is behavior; buying after markets have risen, selling after they have fallen, moving to cash during frightening periods, and missing the recoveries that follow.

“Investment results are more dependent on investor behavior than on fund performance.”

That finding, from the 2025 DALBAR report, is the single most important sentence in this article. Your returns over a 20 or 25-year retirement will be shaped more by what you do during the difficult weeks than by which funds you own during the easy ones.

Why the Brain Gets This Wrong

The behavioral economics research of Daniel Kahneman and Amos Tversky established something confirmed by decades of subsequent study: human beings feel the pain of a loss approximately twice as intensely as the pleasure of an equivalent gain.

This is called loss aversion, and it is not a character flaw. It is a feature of how human cognition evolved to handle genuine danger. When the threat was a predator or a food shortage, the brain that responded urgently to potential losses survived. The brain that deliberated calmly often did not.

In investing, that same hardwired urgency works in reverse. Falling portfolio values trigger the same neural response as physical danger. The brain generates a feeling that action is required immediately. Waiting feels irresponsible. Moving to safety feels prudent. And the more alarming the context — a geopolitical crisis, an oil shock, a jobs miss — the stronger that signal becomes.

The problem is that the “safety” the brain reaches for; moving to cash, reducing equity exposure, waiting for clarity; consistently produces worse outcomes than staying invested. Not in theory. In the hard data of 30 years of actual investor behavior.

The Recovery Is the Most Dangerous Part

Most investors who move to cash during a downturn understand, at least in the abstract, that they will need to get back into the market at some point. What they underestimate is how costly the timing of that return is.

Research consistently shows that seven of the ten best single-day market returns over any recent 20-year period occurred within two weeks of the ten worst days. The market does not announce its recovery days in advance. They arrive suddenly, often when the news is still alarming, when headlines still sound dangerous, and when getting back in feels as frightening as it did to get out.

The investor who moved to cash now faces a different and worse decision: when is it safe enough to go back in? The answer that feels rational, “when things stabilize”, is almost always the wrong one. By the time things feel stable, the recovery has already happened.

The Cost of Missing the Recovery — Illustrative Example

Consider $500,000 invested in a broadly diversified portfolio across a 20-year period that included the 2008 financial crisis, the 2020 pandemic crash, and multiple corrections. Left invested through every downturn, the portfolio grows to approximately $1.93 million at a 7% average annual return. Now assume the investor moved to cash during three major scares, missing 15 of the best trading days in the process. The same $500,000 grows to approximately $890,000. Same market. Same starting amount. The difference — more than $1 million — was behavior during three frightening periods. Each decision felt right at the time.

Why This Matters More in Retirement Than During Accumulation

During the accumulation years, behavioral mistakes are expensive but often recoverable. Time is on your side. Contributions continue. The portfolio has years to recover what emotion cost it.

In retirement and in the years just before it, the stakes change significantly in three specific ways.

Withdrawals replace contributions.

When a portfolio falls and an investor sells investments to cover living expenses, those shares are permanently gone. They cannot recover because the investor no longer owns them. This is the mechanism behind sequence-of-returns risk, and it is why the first five to seven years of retirement carry disproportionate financial weight. A 15% decline in year one of retirement has a meaningfully larger impact on long-term sustainability than the same decline in year fifteen.

Emotional intensity is at its peak.

When the money falling represents your income for the next 20 years, losses do not feel abstract. They feel like years of work disappearing. That emotional intensity is precisely when the behavioral research says investors are most likely to make the most costly decisions. The feeling of urgency is most powerful exactly when acting on it is most dangerous.

The false safety trap compounds silently.

A retiree with a 25-year horizon who moves entirely to cash or short-term bonds is not being conservative. They are accepting guaranteed purchasing power erosion while giving up the growth their portfolio needs to last as long as they do. At 4% inflation, $500,000 in cash has roughly $274,000 of real purchasing power in 10 years. The balance on the statement looks the same. The retirement it can fund does not.

“Being overly cautious of market volatility could leave investors with a portfolio unable to grow enough to meet their spending needs through retirement.”

Has Anyone Reviewed Whether Your Plan Is Built for This Environment?

The behavioral risks in retirement are different from those during accumulation — and most plans are not specifically designed around them. We will review your buffer, your allocation, and whether your written plan eliminates or amplifies the pressure to act under stress.

Free, no obligation, about 20 minutes.

Schedule Your Free Portfolio Review →

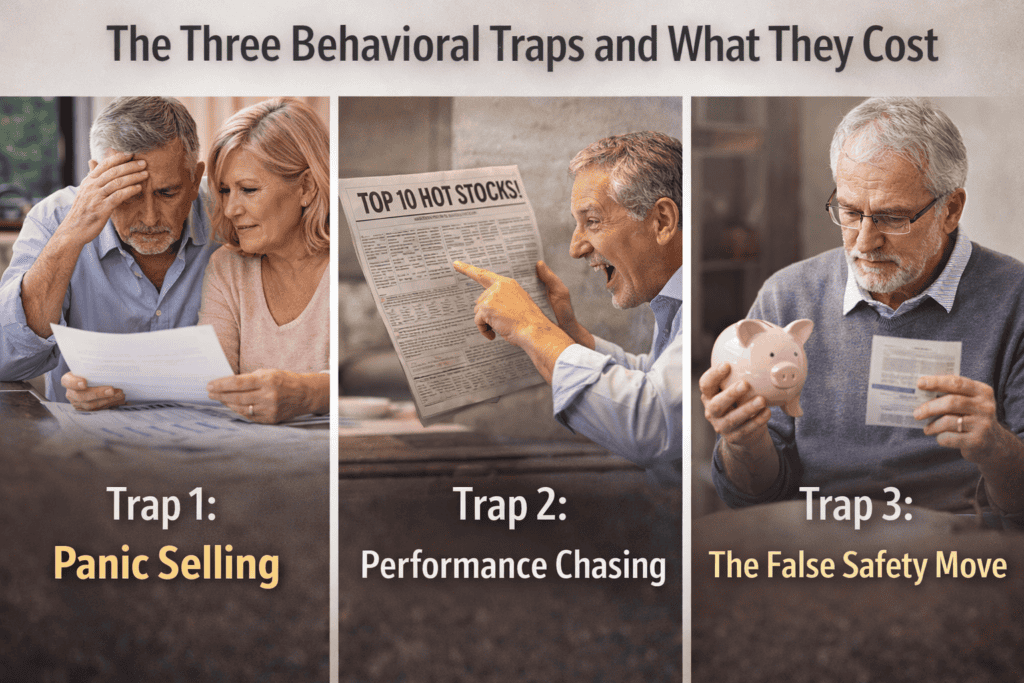

The Three Behavioral Traps and What They Cost

Trap 1: Panic Selling

Selling during a downturn to stop the immediate pain. This locks in the loss permanently and removes the investor from the recovery. Because recoveries tend to arrive before the news feels safe again, investors who sold are usually still waiting on the sidelines when the rebound happens. They then face buying back at higher prices than they sold, which most cannot bring themselves to do, or staying out even longer, missing more of the recovery.

Trap 2: Performance Chasing

Moving money toward whatever has performed best recently. After a period of strong returns in a specific sector, investors allocate more to it; buying high, attracted by recent performance. When that leadership cycle ends, as cycles always do, they are overexposed to exactly the area now correcting. DALBAR’s data shows that investors consistently underperform the very funds they hold, because they buy them after they have already risen.

Trap 3: The False Safety Move

Moving entirely to cash or very short-term instruments during a period of fear, believing this is the responsible choice. For a retiree with a 20 to 25-year horizon, a portfolio that never grows does not protect purchasing power — it erodes it. If inflation runs at 4% and cash earns 4%, the real return is zero. Expenses continue rising. The portfolio does not keep pace. The conservative feeling of being in cash can quietly undermine financial security over a decade in a way that feels invisible until it is too late to address.

What the Research Says Works Instead

The investors who consistently outperform their behavioral counterparts are not the ones who made better market predictions. They are the ones who built structures that made predictions unnecessary.

1 — Build the Buffer

Keep 12 to 24 months of essential living expenses in stable, liquid assets outside your investment portfolio. This single change eliminates the most common source of forced selling in retirement — the need to cover expenses when markets are down. With a buffer in place, a market decline becomes something to monitor, not something that immediately affects your ability to pay bills.

2 — Write the Plan

Investors with a written financial plan that specifies their target allocation and rebalancing conditions make far better decisions in volatile periods. The plan becomes the decision-maker. When markets fall, the question is not “should I change something?” It is “does my allocation still match my plan?” If yes, no action is required.

3 — Pre-Commit the Answer

The most underutilized tool in behavioral finance is the conversation that happens before a crisis, not during one: “If markets fall 20%, what will we do?” Having that conversation in advance, documenting the answer, and committing to it while emotions are calm changes the decision entirely when the decline actually arrives.

None of these require predicting what markets will do. They require building a structure that makes the prediction irrelevant — and holding to that structure when everything around you says to abandon it.

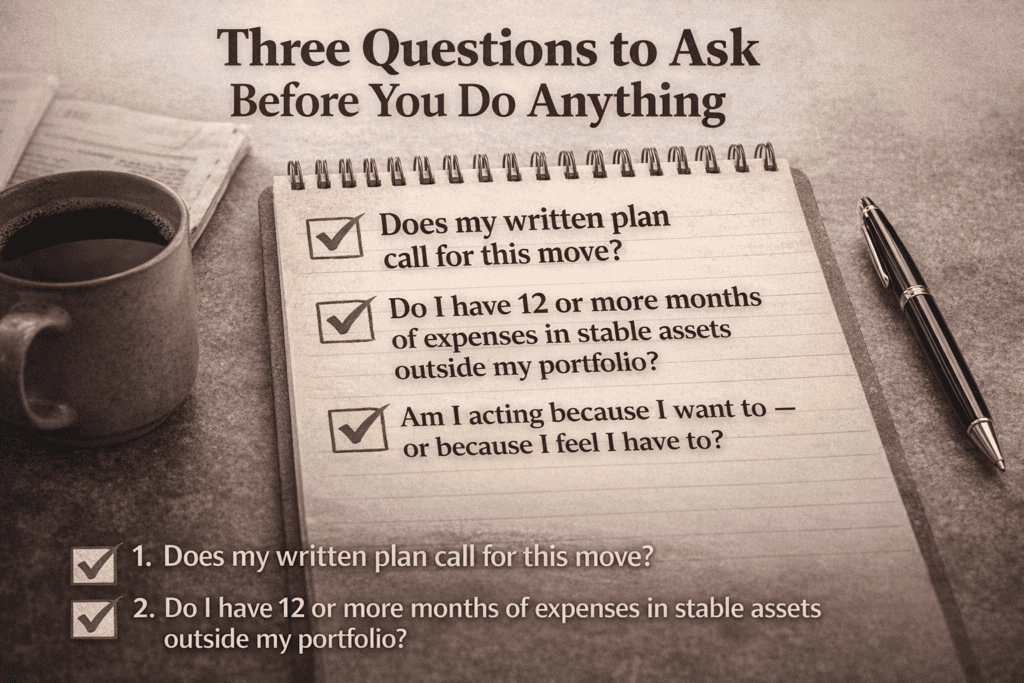

Three Questions to Ask Before You Do Anything

The current environment is producing pressure to act. Before making any portfolio change, work through these three questions in order. They are designed to make sure that if you act, it is your plan driving the decision — not the headline.

Question 1

Does my written plan call for this move?

Your plan was built when you were calm. If the plan does not specify this action, that absence is meaningful.

| ✓ Yes — the plan specifies this action. Proceed. Document why and inform your advisor. | → No — this is a reaction to current conditions Stop. Continue to Question 2 before taking any action. |

Question 2

Do I have 12 or more months of expenses in stable assets outside my portfolio?

If yes, you are not financially compelled to sell anything right now. The pressure to act is emotional, not structural.

| ✓ Yes — my buffer is intact Continue to Question 3. The financial urgency is not real. | → No — my buffer is below 12 months Call your advisor to discuss building the buffer first. |

Question 3

Am I acting because I want to — or because I feel I have to?

The feeling of having to act is the most reliable signal in behavioral finance that a decision will be regretted.

| ✓ I want to — this is a deliberate, considered decision Call your advisor, walk through the reasoning, and proceed if it still makes sense. | → I feel I have to — the discomfort is driving this Wait 48 hours. Then call your advisor. |

What This Week’s Headlines Mean for Your Portfolio

The current environment — oil prices up sharply, a jobs miss, a frozen Fed, geopolitical uncertainty with no obvious near-term resolution — is exactly the kind of environment where the behavioral research says investors are most likely to make costly decisions.

It is also exactly the kind of environment where the same research says that doing nothing, assuming your structure is sound, produces the best long-term outcomes.

The S&P 500 is down roughly 5% from its all-time high as of this writing. That is not a crash. It is not even a correction by the standard definition. But it feels more alarming than the number suggests, because of the context surrounding it. That feeling is information about your emotional state. It is not information about what the market will do next.

The question worth asking right now is not “is this the time to make a move?” It is: does my current structure — my buffer, my allocation, my written plan — make a move necessary or even rational? For most investors with a well-designed retirement plan, the answer is no.

The Bottom Line

The most expensive mistake in retirement investing is not buying the wrong fund, making the wrong sector bet, or timing the market incorrectly. Those mistakes are recoverable.

The most expensive mistake is making a sequence of decisions that felt right in the moment; panic selling during a downturn, chasing recent performance, moving to false safety, and missing the recoveries that followed. Each one felt reasonable. Together, they produced the 8.48% annual gap that DALBAR has documented year after year for three decades.

The protection is not better market prediction. It is better structure: a buffer that eliminates forced selling, a written plan that becomes the decision-maker, and a pre-commitment conversation that decides in advance what you will do when the headlines get loud.

That structure is worth more than any market call. And it is far easier to build before a difficult week than during one.

Is Your Portfolio Structured to Survive the Decisions You Might Make?

Most retirement plans are designed around investment assumptions. The best ones are also designed around behavioral ones. We will review whether your current structure eliminates or amplifies the pressure to make costly decisions under stress and tell you clearly what, if anything, needs attention.

Free, no obligation, about 20 minutes.

Schedule Your Free Behavioral Portfolio Review →

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.