You are somewhere in your 50s. You look at your retirement balance and the number is smaller than you hoped.

Key Takeaways

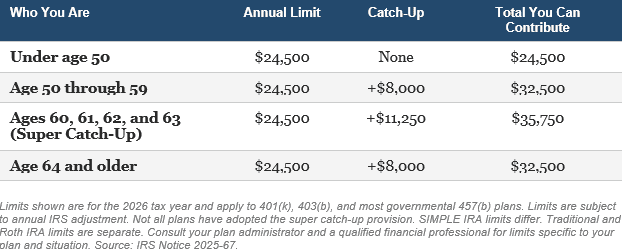

- Workers aged 60-63 can contribute ,750 annually to 401(k) plans through the super catch-up provision

- HSAs function as powerful retirement accounts with triple tax advantages when medical expenses are paid out-of-pocket

- The three catch-up tools (401k, HSA, IRA) can be used simultaneously, not competitively

- High earners over 0,000 FICA wages must make catch-up contributions on a Roth basis starting 2026

- The super catch-up window closes permanently at age 64 and never reopens

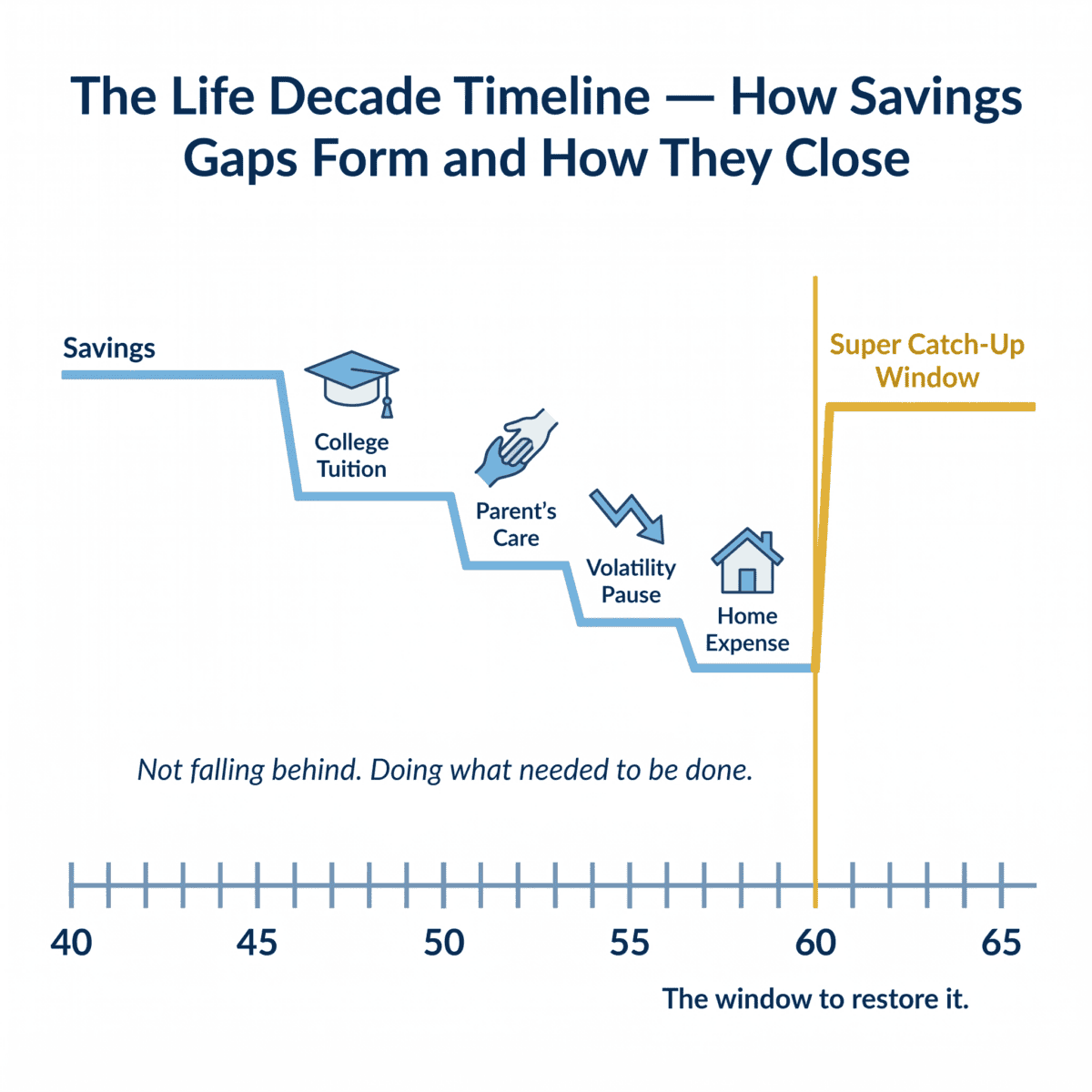

Life redirected the money you meant to save. College tuition. A parent who needed help.

A year when the market scared you and you pulled back. A divorce that reset everything. A business that took everything you had.

You did not fall behind because you were careless. You fell behind because you were doing the right thing for the people around you, and somewhere along the way your own future got pushed to the back of the line.

Most people in this situation assume the window to fix it has mostly closed. They contribute what they can. They tell themselves they will make it work.

What almost nobody told them is that the tax code has a set of tools built specifically for this decade. Some kick in at 50. One gets bigger at 55.

Another opens at 60 and closes permanently at 63. Used together, they may allow someone in their 50s to save meaningfully more than they thought possible, often in accounts most people are not fully using.

This article covers those tools, how they work, and what they may mean for someone who feels like they are running out of time.

The Savings Gap Most People Carry Silently

Feeling behind on retirement savings is one of the most common financial anxieties in America. People compare their balance to a number they read somewhere, or to what they assume their peers have saved, and they carry a quiet worry that they have fallen short.

According to the Employee Benefit Research Institute, half of Americans retire earlier than they planned. The median retirement age in the United States is 62. For most people, that means less time to save than they expected when they started.

Research from Fidelity Investments and Vanguard shows that average 401(k) balances rose more than 10% in 2025. Balances are growing. But for many people in their 50s, the balance still feels short of where it needs to be.

What most of those people do not know is that the tax code may give them more runway than they realize. Not because the rules changed recently, but because the rules that already exist are almost never fully explained.

Tool One: The Catch-Up That Starts at 50

The first tool becomes available the year you turn 50. Most people who have worked with a financial advisor know it exists. Many do not use it to its full potential.

Once you turn 50, the IRS allows you to contribute more to your 401(k) each year than younger workers are allowed. In 2026, the standard 401(k) contribution limit for workers under 50 is $24,500. The moment you turn 50, you can add an additional $8,000 per year as a catch-up contribution, bringing your total to $32,500.

This applies to 401(k), 403(b), and most governmental 457(b) plans. If you are currently contributing at the standard limit and have not updated your contribution to reflect the catch-up, you may be leaving $8,000 in tax-advantaged savings on the table each year.

That is a meaningful starting point. But it is just the beginning of what is available.

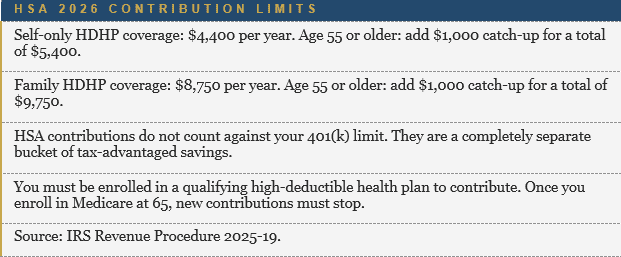

Tool Two: The HSA as a Second Retirement Account

Most people think of a Health Savings Account as a way to pay for medical bills. A debit card for copays and prescriptions. That framing is the most common reason people leave one of the most powerful savings tools in the tax code completely underused.

The HSA is available to people enrolled in a qualifying high-deductible health plan, a plan with a higher annual deductible in exchange for lower monthly premiums. If you have that type of plan, you can contribute to an HSA regardless of age. At 55 and older, the contribution limit increases further.

Why This Is a Retirement Account, Not Just a Healthcare Account

The strategy that turns an HSA into a retirement savings accelerator is this: pay your medical expenses out of pocket now and invest your HSA balance for long-term growth. There is no time limit on HSA reimbursements. That means you can reimburse yourself years later, with dollars that have been growing tax-free in the meantime.

A 55-year-old on a family high-deductible plan who contributes $9,750 to their HSA each year instead of spending it on medical costs is building a second retirement account alongside their 401(k). The two accounts together may allow them to shelter meaningfully more income from taxes each year than most people assume is possible.

After age 65, HSA withdrawals for qualified medical expenses remain tax-free for life. For non-medical expenses, withdrawals are taxed as ordinary income, similar to a traditional IRA. But for healthcare costs in retirement, including Medicare premiums, dental, vision, and hearing expenses, the HSA provides tax-free income from an account that has been growing for years.

Tool Three: The IRA Catch-Up Most People Overlook

On top of your 401(k) and HSA contributions, the IRS also allows an additional contribution to an Individual Retirement Account each year. For 2026, the IRA contribution limit is $7,500 for savers under age 50. For those age 50 and older, an additional $1,100 catch-up brings the total to $8,600.

Whether this strategy makes sense depends on your income and your tax situation. Contributions to a traditional IRA may be tax-deductible depending on your income and whether you or your spouse are covered by a workplace retirement plan. Roth IRA contributions are made with after-tax dollars but grow and can be withdrawn tax-free in retirement, subject to income eligibility limits.

IRA contributions are subject to income phase-out ranges that vary by filing status and plan coverage. A qualified tax professional can help you determine which type makes sense for your situation and whether you are eligible for the full contribution. The important thing to know is that this bucket exists, it is separate from your 401(k) limit, and for many people in their 50s it is an additional savings opportunity they have not fully explored.

Tool Four: The Roth Conversion Window in Your 50s

Your 50s are often the best decade to think about Roth conversions. Not because the math always works in their favor, but because this is typically the window when several factors come together in a useful way.

A Roth conversion means taking money out of a pretax account like a traditional IRA or 401(k), paying ordinary income taxes on the amount converted today, and moving it into a Roth account where it grows tax-free. Future withdrawals from the Roth are not taxed. And unlike traditional accounts, Roth IRAs do not have required minimum distributions starting at age 73.

Why does this matter in your 50s specifically? A few reasons. Income may be near or at its peak, which means the tax rate you pay today may not be dramatically higher than what you would pay in retirement.

Mandatory distributions do not begin until 73, so converted Roth balances can grow tax-free for a decade or more before you need them. And reducing your pretax account balance now means smaller required distributions later, which can reduce Medicare surcharges and keep more of your Social Security benefit from being taxable.

Roth conversions are not right for everyone and can be counterproductive if done in the wrong year or at the wrong amount. Converting too much in a single year can push you into a higher tax bracket or trigger Medicare surcharges two years later. This is a strategy worth modeling with a qualified financial professional before acting on it, not a DIY calculation.

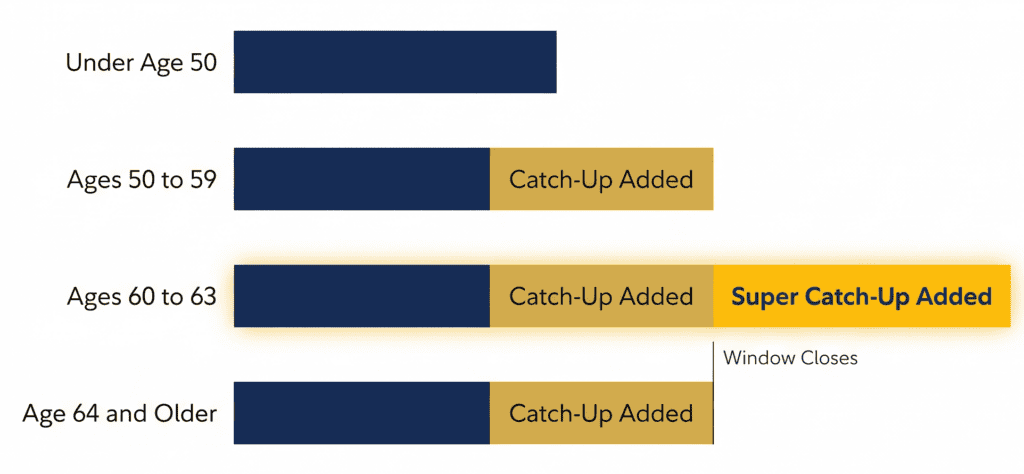

Tool Five: The Super Catch-Up That Almost Nobody Knows About

The SECURE 2.0 Act, signed into law in December 2022, created a new and larger catch-up contribution window for a specific group: people between the ages of 60 and 63.

During these four years, and only these four years, the catch-up contribution limit is higher than the standard age-50 catch-up. In 2026, the super catch-up allows a total contribution of $35,750 to a 401(k) or similar workplace retirement plan. The moment you turn 64, the limit drops back to the standard age-50 amount. The window does not reopen.

Who You Are Annual Limit Catch-Up Total You Can Contribute

The Tax Reduction Angle Most People Overlook

Every dollar you contribute to a traditional pretax 401(k) reduces your taxable income for the year. If you are in the 22% federal tax bracket and you contribute $35,750 this year instead of $24,500, you have reduced your taxable income by an additional $11,250. At 22%, that is approximately $2,475 in federal tax savings in a single year from the super catch-up alone.

For someone in a higher bracket, the savings are larger. For someone who expects to be in a lower bracket in retirement than they are today, contributing pretax now and paying taxes later at a lower rate may add a second layer of value.

What the Full Toolkit Could Mean Together

Here is the insight most people never see. These tools do not compete with each other. They stack. Each one draws from a different bucket with different rules and different tax treatment.

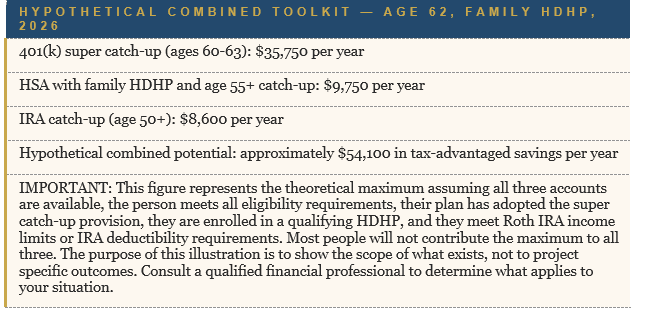

Consider someone who is 62 years old and enrolled in a family high-deductible health plan. In 2026, assuming they meet all eligibility requirements and their plan allows it, the combined available contribution across all three accounts could look like this.

✓ Curious how much tax-advantaged savings capacity you’re actually leaving on the table? Take our 5-minute Catch-Up Calculator to discover your personalized contribution limits across all available accounts. Get your results instantly and see what’s possible before age 64.

What This Looks Like in Real Numbers: Meet Karen and David

Hypothetical scenario for illustration purposes only. Karen and David are fictional characters representing a composite of common planning situations. This scenario does not represent actual client results.

Assumed annual growth rate of 6% is not guaranteed, does not represent any specific investment, and is used for illustrative purposes only. Actual results will vary based on contribution amounts, investment performance, tax rates, plan rules, and individual circumstances. Past performance does not guarantee future results.

Karen is 61. She spent 14 years working part-time while raising three children and returned to full-time work at 52. David is also 61.

He spent 27 years in manufacturing management. Together they earn approximately $140,000 per year.

They have saved consistently. But four years of college tuition for their youngest, two years of reduced contributions while helping David’s mother through a health situation, and a stretch in 2022 when market volatility pushed them to pause contributions left their combined retirement balance at approximately $380,000. It is not where they hoped to be at 61.

When they sat down for a planning conversation, they expected to hear that they needed to work longer or spend less. That was not the conversation they had.

Instead, they discovered three things they had not known. First, David’s employer plan had adopted the super catch-up provision. Starting that year, they could contribute $35,750 to his 401(k) instead of $24,500.

Second, Karen’s employer offered a high-deductible health plan. By switching to it and opening an HSA, she could contribute $9,750 per year to a second tax-advantaged account. Third, they had never contributed to IRAs.

At their income level, a Roth IRA was available to Karen and a deductible traditional IRA contribution may have been available to David depending on coverage and income.

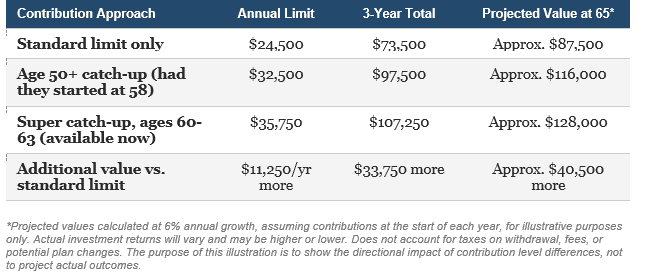

They focused on what was immediately actionable: the super catch-up and the HSA. Here is what the numbers looked like for the 401(k) piece alone.

At a combined income of $140,000, Karen and David fall below the $150,000 individual FICA wage threshold that would require Roth catch-up contributions in 2026. In this hypothetical illustration, David’s pretax super catch-up contributions reduce their taxable income by an additional $11,250 per year. At a 22% federal rate, that may be approximately $2,475 in federal tax savings per year from the super catch-up alone, or approximately $7,400 over three years.

State tax treatment varies. Individual results depend on filing status, deductions, and applicable rates.

When Karen added the HSA, they were sheltering an additional $9,750 per year from taxes in a dedicated healthcare reserve that would also double as a retirement savings account. In this hypothetical, the combination of the super catch-up and the HSA added approximately $21,000 per year in new tax-advantaged savings capacity they had not been using.

David said the planning conversation changed how he thought about the next three years. Not as the final stretch before retirement but as the most meaningful savings window of his financial life.

If Life Got in the Way, That Is the Point

Many people in their 50s and early 60s are what researchers call the sandwich generation. They are supporting aging parents and adult children at the same time, often while carrying their own financial obligations. Caregiving.

Tuition. Medical costs for a parent. A child who needed help getting started.

These are not irresponsible choices. They are the choices people make when they are the ones others depend on. The financial cost accumulates quietly over years without a line item on any statement.

The expanded contribution rules in the 50s and early 60s reflect a recognition that this decade is when life is often the most financially demanding and, often, when income is finally at or near its peak. The higher limits are available exactly during the years when contributing more becomes possible for the first time in a long time.

Why This Decade Is Also the Most Vulnerable for Your Portfolio

There is a second reason these years matter beyond contribution limits. It is a concept researchers call the retirement red zone.

Your retirement portfolio is at or near its largest point during the final years before you stop working. A significant market decline in this window hits at the worst possible time. The portfolio is at its maximum size, contributions are slowing or ending, and there is the least time to recover before distributions begin.

Research from Morningstar’s Mind the Gap 2025 study found that the average investor consistently earns less than the funds they invest in. The reason is behavioral. People tend to reduce equity exposure after a decline and miss the recovery. The financial cost of that pattern is real.

Building a larger balance through the tools available in your 50s does not eliminate this risk. But contributing consistently during these years, rather than pulling back, is one of the more meaningful ways to build the cushion that makes sequence-of-returns risk more manageable. Staying invested through the years when it feels most uncomfortable is one of the hardest and most valuable things a pre-retiree can do.

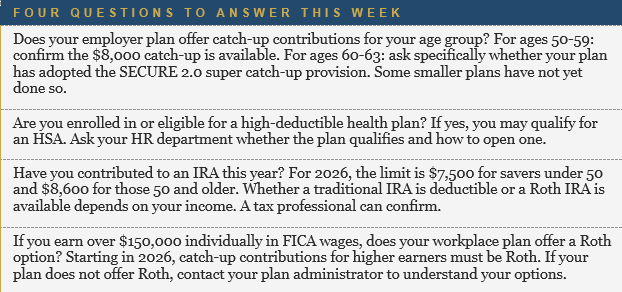

How to Know Which Tools Are Available to You

Not every tool in this article is available to every person. Eligibility depends on your age, your income, your employer’s plan, your health plan type, and your existing account balances. Here is how to start.

What If I Cannot Afford to Max Everything Out?

The limits in this article are ceilings, not requirements. Contributing any amount above what you currently contribute is a step forward. Many people find it easier to increase contributions gradually, by 1% or 2% of salary per year, than to try to jump to the maximum immediately.

The goal is not to hit every limit. The goal is to use the tools that are available to you intentionally, because some of them close permanently with time. The super catch-up window for ages 60 to 63 is the most time-sensitive. The moment you turn 64 it closes and does not reopen.

The Most Valuable Conversation You Can Have Right Now

If you are in your 50s and you feel behind on retirement savings, you are not out of options. You may have more tools available than you have ever been told about. Some of them are available right now. Some of them will not be available in a few years.

The standard catch-up started at 50. The HSA catch-up increased at 55. The super catch-up opens at 60 and closes permanently at 64.

Roth conversions are most valuable in the years before mandatory distributions begin at 73. Each tool has a window. The windows do not stay open.

The families that build the most retirement security in this decade are not always the ones who started with the most. They are often the ones who found the rules that applied to their situation and used them fully while they still could. That starts with knowing they exist.

ABOUT THE FINANCIAL PLANNING AUTHOR

Alexander Langan, J.D., CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual and Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

ABOUT LANGAN FINANCIAL GROUP: FINANCIAL ADVISORS

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, PA.

With over 150 five-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice. Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC. Investment Advisor Representative, Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor.

Cambridge and Langan Financial Group, LLC are not affiliated. Cambridge does not offer tax or legal advice. All hypothetical examples are for illustration purposes only and do not represent actual client results.

Past performance does not guarantee future results. Individual results will vary. The 6% growth rate used in illustrations is hypothetical and not guaranteed and does not represent the performance of any specific investment.

401(k) contribution limits are for the 2026 tax year per IRS Notice 2025-67 and are subject to annual adjustment. The super catch-up provision of $11,250 applies to 401(k), 403(b), and governmental 457(b) plans that have adopted the SECURE 2.0 provision; not all plans have done so. HSA contribution limits are for the 2026 tax year per IRS Revenue Procedure 2025-19; eligibility requires enrollment in a qualifying high-deductible health plan as defined by IRS guidelines; contributions must stop upon Medicare enrollment.

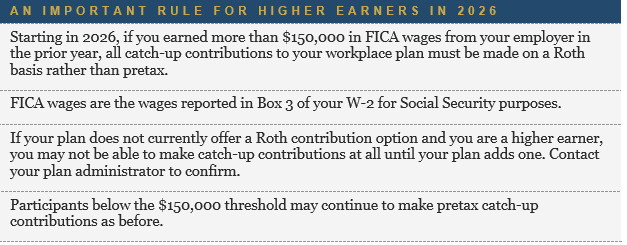

IRA contribution limits are for the 2026 tax year; deductibility and Roth eligibility are subject to income phase-out ranges. Roth IRA contributions are subject to income limits. Starting in 2026, catch-up contributions for employees who earned more than $150,000 in FICA wages from their employer in the prior year must be made on a Roth basis per SECURE 2.0 Act provisions; if a plan does not offer Roth contributions, catch-up contributions may not be available to those employees.

Roth conversions increase taxable income in the year of conversion and should be evaluated with a qualified tax professional. Tax savings illustrations assume a 22% federal tax rate for hypothetical purposes only; actual results depend on individual filing status, income, deductions, state taxes, and other factors. The combined $54,100 hypothetical toolkit figure assumes maximum contributions across all three accounts by an eligible 62-year-old with family HDHP coverage meeting all eligibility requirements; most individuals will not contribute the maximum to all three accounts.

Data sourced from Northwestern Mutual 2026 Planning and Progress Study, Employee Benefit Research Institute, Fidelity Investments, Vanguard, Morningstar Mind the Gap 2025, and IRS guidance on SECURE 2.0 Act provisions. This article must be reviewed and approved by a qualified registered principal prior to use as a retail communication under FINRA Rule 2210.