When markets drop and headlines turn dark, most people feel the same pull.

Do something. Anything. Just don’t sit still.

It’s a completely human response. But it’s also the response that causes the most financial damage during volatile periods, not the volatility itself.

The investors who come through these moments with the least regret aren’t the ones who move fastest. They’re the ones who pause longest, follow a process, and resist the instinct to treat urgency as a strategy.

That discipline isn’t passive. It’s a skill and it looks very different from doing nothing.

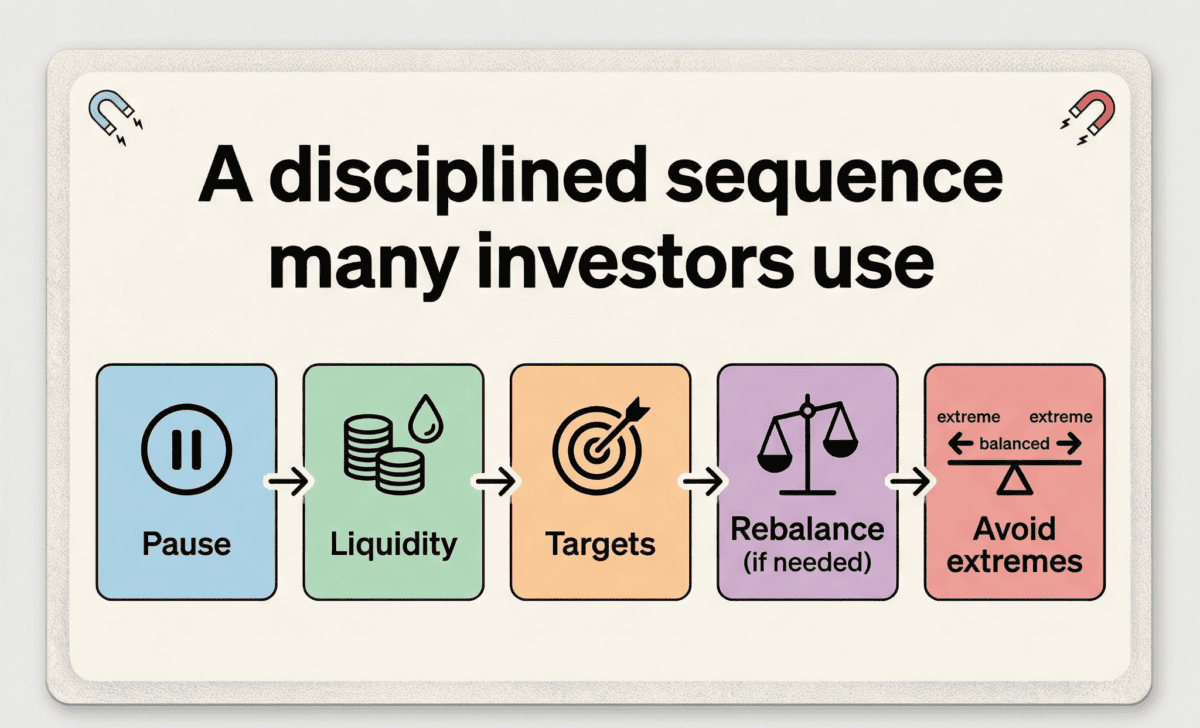

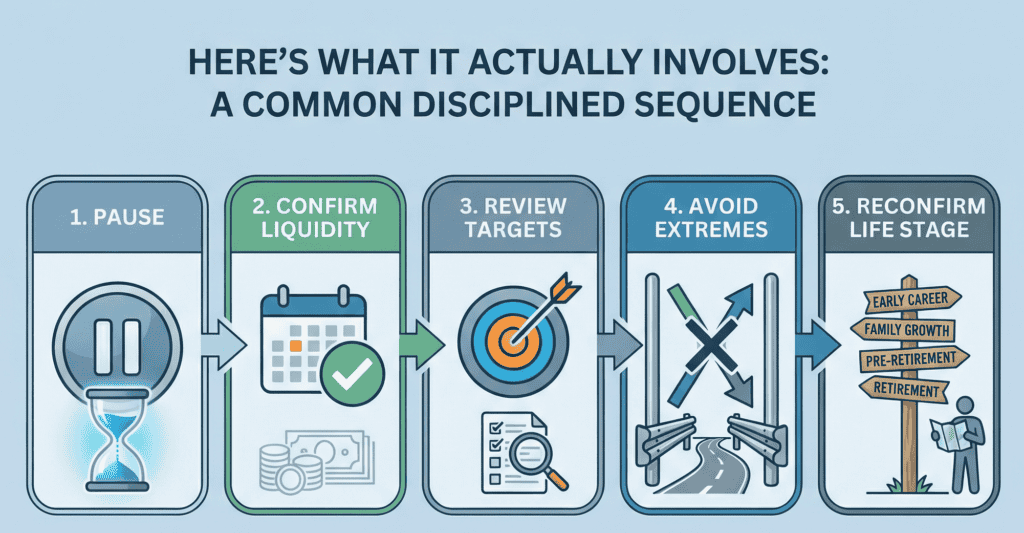

Here’s what it actually involves.

Step 1: Pause Before Acting

The first move isn’t a trade. It’s time.

Sharp market reactions often happen before the full picture is available. Decisions made at peak uncertainty, when emotions are highest and information is least complete, carry the highest risk of regret.

Disciplined investors give themselves at least 24 to 48 hours before making any structural changes. Not because they’re ignoring the situation, but because they understand that urgency and accuracy rarely coexist during volatile markets.

The data supports this instinct. According to JPMorgan Asset Management’s long-term market research, an investor who missed just the 10 best trading days in the S&P 500 over a 20-year period ended up with roughly half the returns of someone who stayed fully invested. Many of those best days occurred during, or immediately after, periods of peak uncertainty.

Urgency rarely improves outcomes. Patience often does.

Step 2: Confirm Short-Term Income Is Secure

Before adjusting investments, calm investors review their liquidity, not their performance.

They ask three questions: How is my next 12 months of spending funded? Do I have cash or short-term assets already set aside? And if markets declined further from here, would anything about my daily life actually change?

That last question cuts through the noise quickly.

An investor with near-term spending already covered in stable assets isn’t forced to make decisions under pressure. That single layer of structure, cash or short-term reserves for near-term needs, removes the element that turns normal volatility into a real problem.

Liquidity doesn’t just protect portfolios. It protects decision-making.

Step 3: Follow Your Rebalancing Rules — Not Your Instincts

Experienced investors don’t react to headlines. They follow guidelines they established when they were calm, precisely because they knew moments like this would come.

During volatility, the right questions aren’t about what the market is doing. They’re about what your portfolio is doing relative to its targets. Has your allocation drifted meaningfully? Does this decline create a rebalancing opportunity? Is your current risk level still appropriate for where you are in life, not where you were five years ago?

Rebalancing and reacting are not the same thing. Rebalancing is planned, systematic, and rooted in strategy. Reacting is unplanned, emotional, and costly.

DALBAR’s annual Quantitative Analysis of Investor Behavior has tracked this gap for decades. In their long-term studies, the average equity investor significantly underperformed the S&P 500, not because of poor fund selection, but because of mistimed decisions made during exactly these kinds of volatile moments.

The gap between what the market returns and what investors actually capture is largely a behavior problem, not an investment problem.

Step 4: Avoid Extreme Allocation Shifts

Moving entirely to cash during market turbulence feels protective. It rarely works the way it feels.

Strong recovery periods frequently begin while headlines are still negative. Investors who exit and wait for clarity often miss the rebound and then face a harder problem: deciding when to get back in, with no clear signal and the same emotional noise still present.

Research from Vanguard suggests that behavioral coaching alone, helping investors avoid reactive exits, adds approximately 1.5% in net annual returns over time. That’s not investment selection. That’s simply not making avoidable mistakes at the wrong moment.

There’s a meaningful difference between a calibrated adjustment and abandoning a plan. One is strategic. The other is surrender dressed up as prudence.

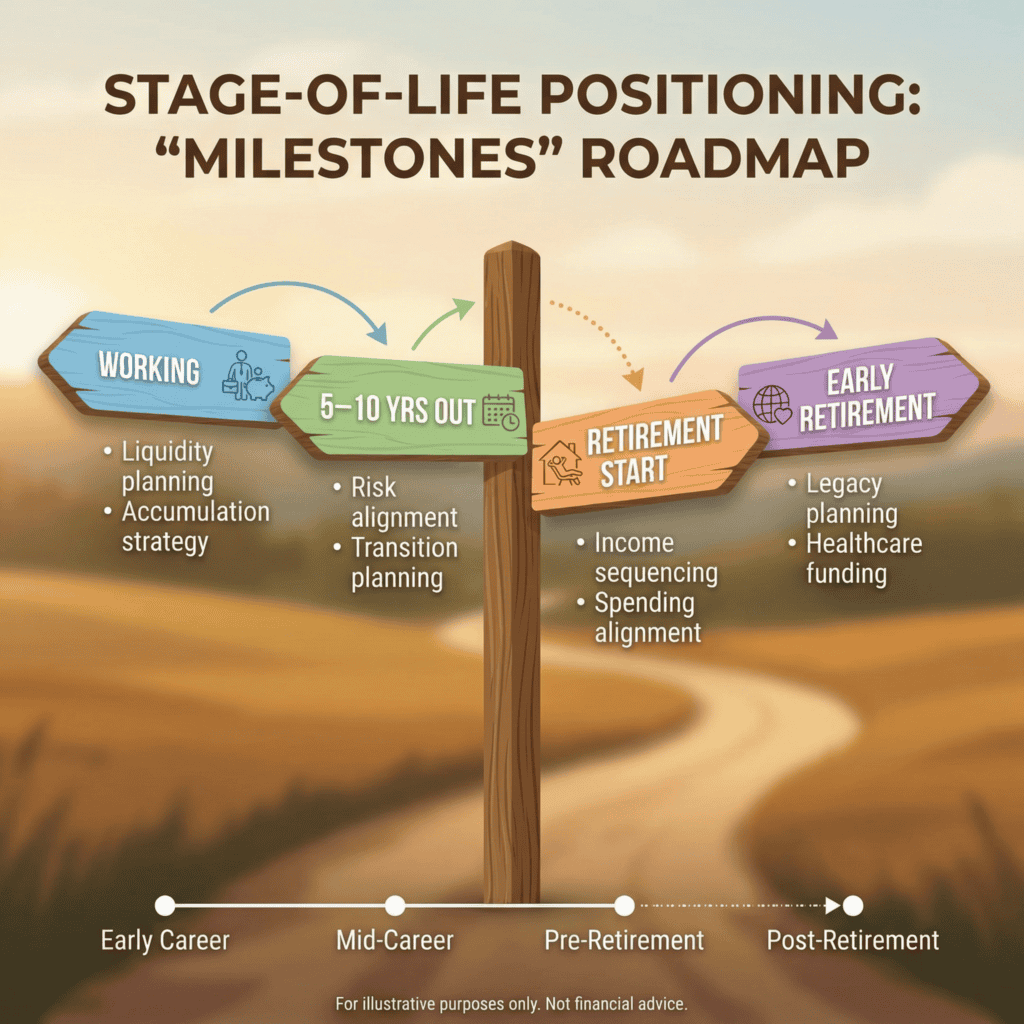

Step 5: Reconfirm Your Stage-of-Life Positioning

Volatility is useful for one thing: it forces clarity about whether your portfolio actually matches the life you’re living now, not the one you were planning for several years ago.

For those already in retirement, the key issue isn’t whether the portfolio can recover. It’s whether the recovery timeline creates any cash flow problems along the way. A portfolio designed to provide income for 25 to 30 years can absorb downturns, but only if it’s structured to avoid selling growth assets at temporarily depressed prices to fund near-term spending.

For those five to ten years out, the question is one of transition. Has your allocation kept pace with the shift from accumulation to preservation? Investors who enter retirement with the same aggressive allocation they held a decade earlier are exposed to sequence-of-returns risk that a few years of thoughtful repositioning could have significantly reduced.

Market volatility doesn’t change your plan. It shows you whether your plan was built for the life stage you’re actually in.

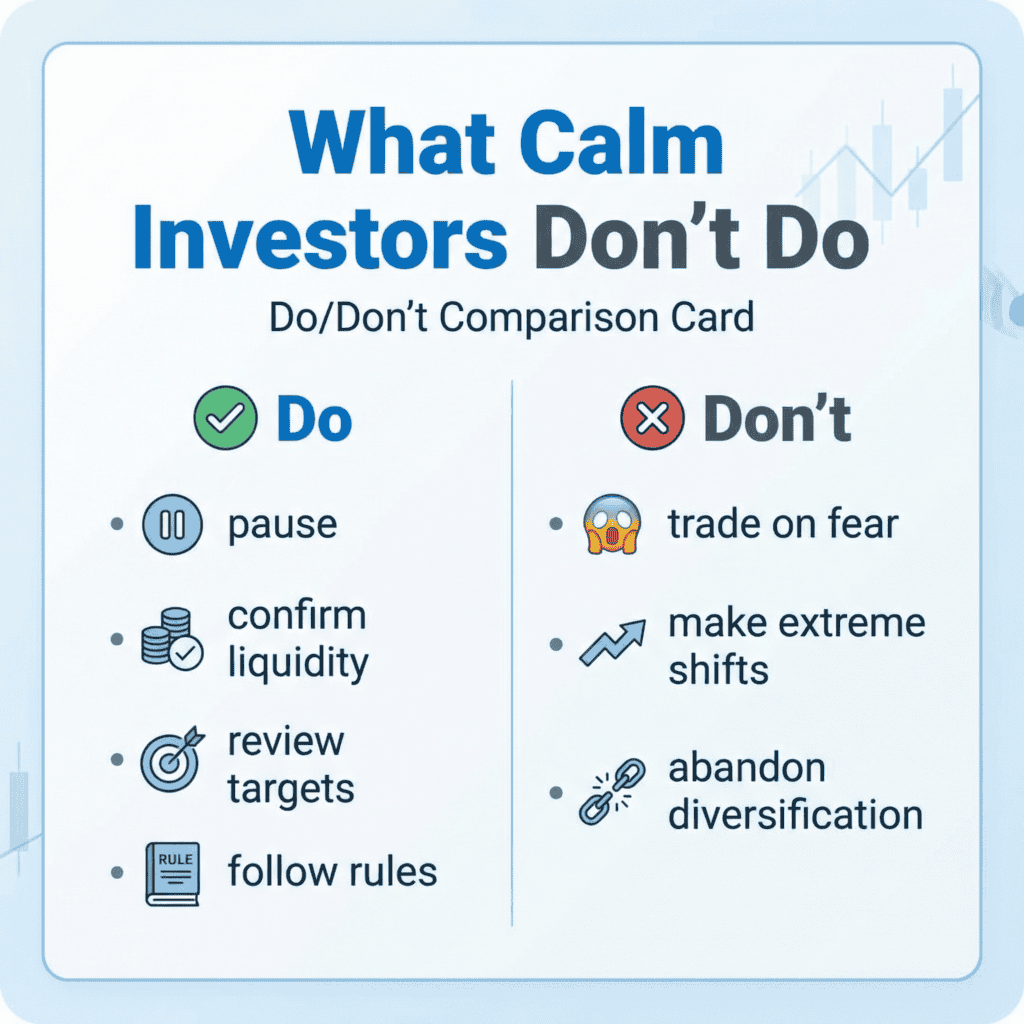

What Calm Investors Don’t Do

They don’t trade on fear. They don’t assume every period of geopolitical tension becomes a prolonged economic contraction, because history shows most don’t. They don’t abandon diversification when it feels like it isn’t working. And they don’t let short-term conditions drive long-term structural decisions.

One of the more counterintuitive findings in investor behavior research comes from Fidelity, which analyzed which accounts performed best over long periods. The answer: accounts belonging to investors who had forgotten they had them. Inactivity, in many cases, outperformed activity.

That’s not an argument for ignoring your plan. It’s an argument for trusting a well-built one.

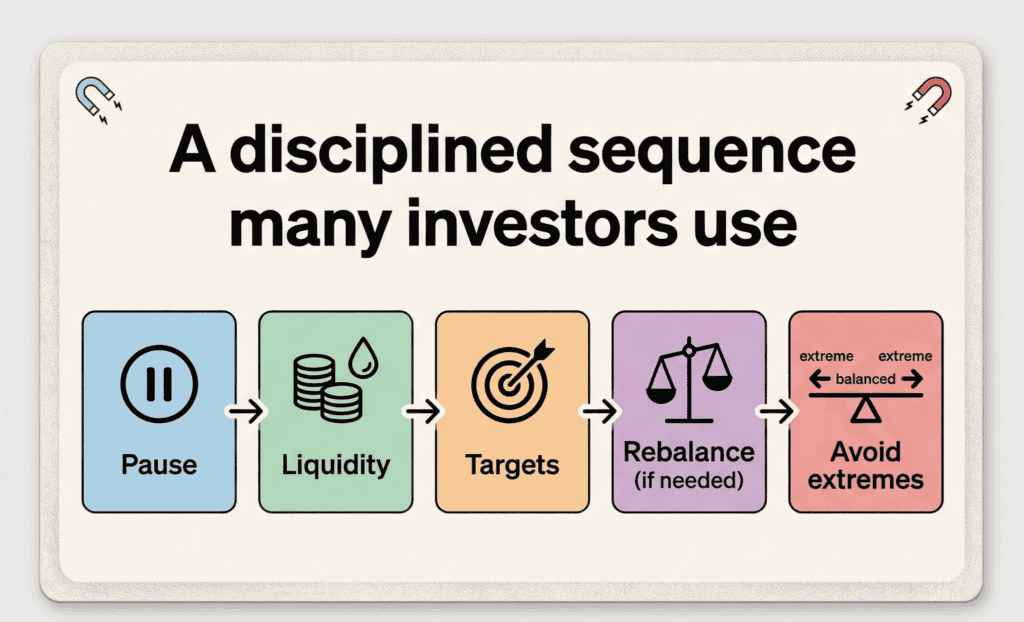

The Sequence That Works

When headlines escalate, disciplined investors follow a simple sequence:

Pause. Confirm liquidity. Review allocation against predetermined guidelines. Rebalance if drift is meaningful. Avoid extreme moves.

That’s not complicated. But it runs counter to every instinct that volatility triggers, which is exactly why most investors don’t follow it consistently.

Retirement success is rarely determined by one week of market turbulence. It’s far more often shaped by whether the decisions made during that week were deliberate or emotional.

If recent events have left you uncertain about whether your plan holds up under pressure, that’s a reason for a calm conversation, not a reason to act before you’ve thought it through.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.