When headlines get loud, the instinct to act is understandable.

Military escalation. Regional conflict. Market swings that feel different this time. If you’re nearing retirement or already there, questions start forming quickly.

Is this the beginning of something bigger? Should I move to cash? Will my retirement income hold?

These are reasonable questions. And history offers some useful perspective.

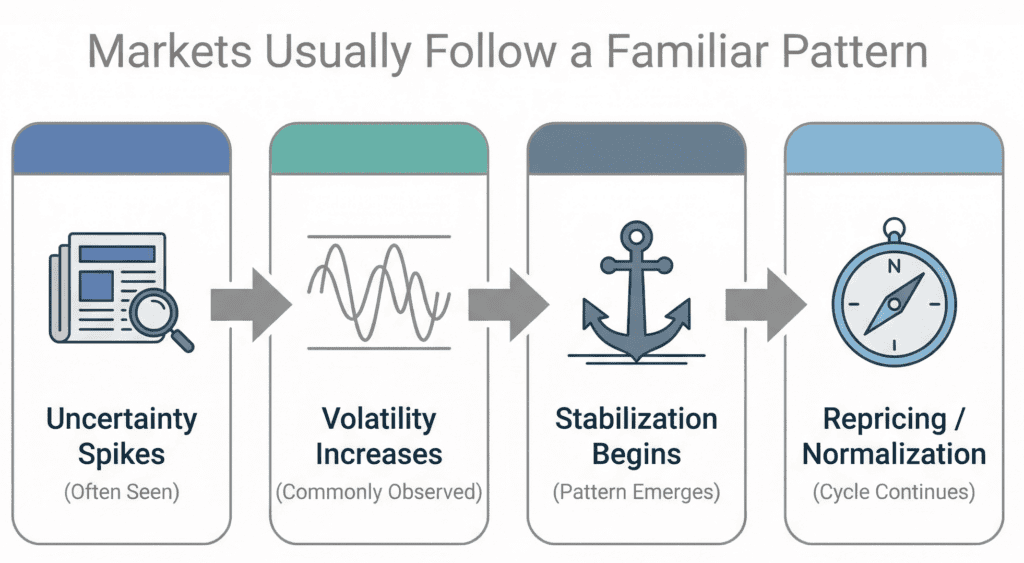

Markets Usually Follow a Familiar Pattern

When geopolitical tensions rise, markets tend to react in a predictable sequence.

First comes the immediate selling; investors price in uncertainty quickly. Then volatility spikes as the news cycle accelerates. Defensive assets like high quality bonds tend to stabilize first. And gradually, as clarity improves, markets begin separating long term economic reality from short term fear.

In many historical cases, the initial reaction was sharper than the long term outcome turned out to be.

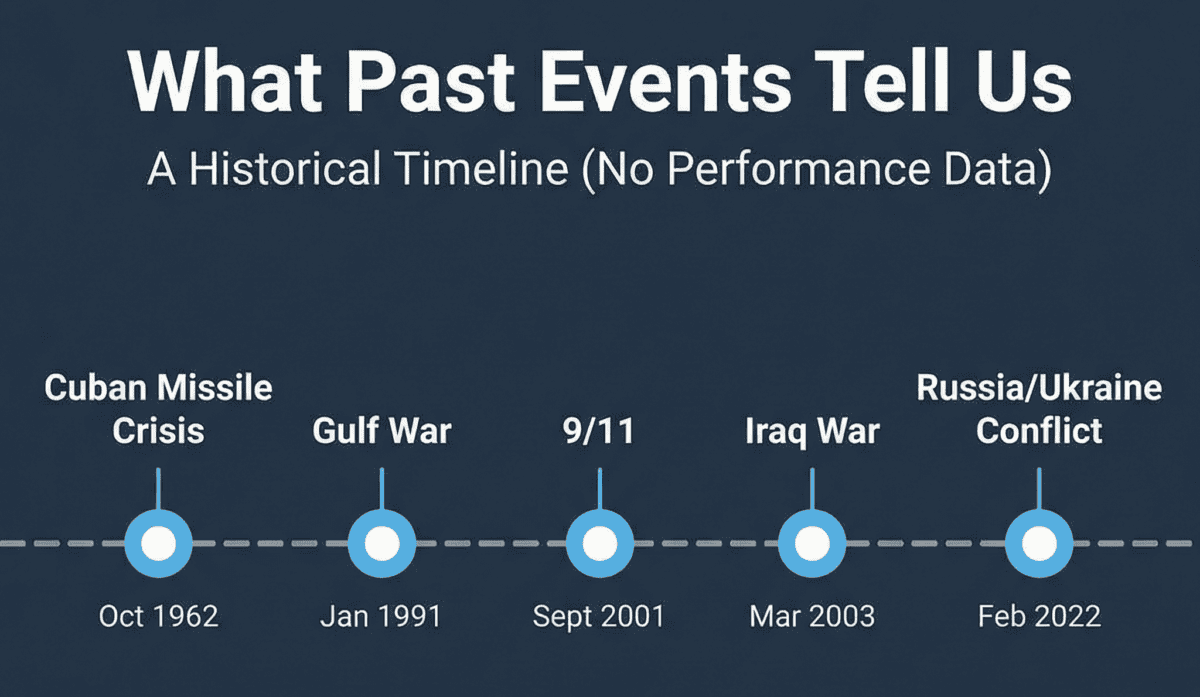

What Past Events Tell Us

Since World War II, markets have weathered a long list of serious events; the Cuban Missile Crisis, the Gulf War, 9/11, the Iraq War, Russia’s invasion of Ukraine, and dozens of regional conflicts in between.

In most cases, markets declined in the short term and recovered within months once economic fundamentals reasserted themselves.

Longer, deeper bear markets were more often tied to recessions, monetary tightening, or credit crises, not isolated geopolitical events.

That distinction matters. Geopolitical shocks create uncertainty. Economic contractions create sustained declines. They are not the same thing, and treating them the same leads to costly decisions.

Volatility Is More Normal Than It Feels

In a typical year, the stock market often experiences a temporary decline of 10–15% at some point, yet many of those same years still finish positive.

Volatility feels unusual in the moment. Historically, it isn’t.

A retirement plan that assumes smooth markets isn’t a realistic one. A plan that assumes periodic downturns and is built to absorb them is.

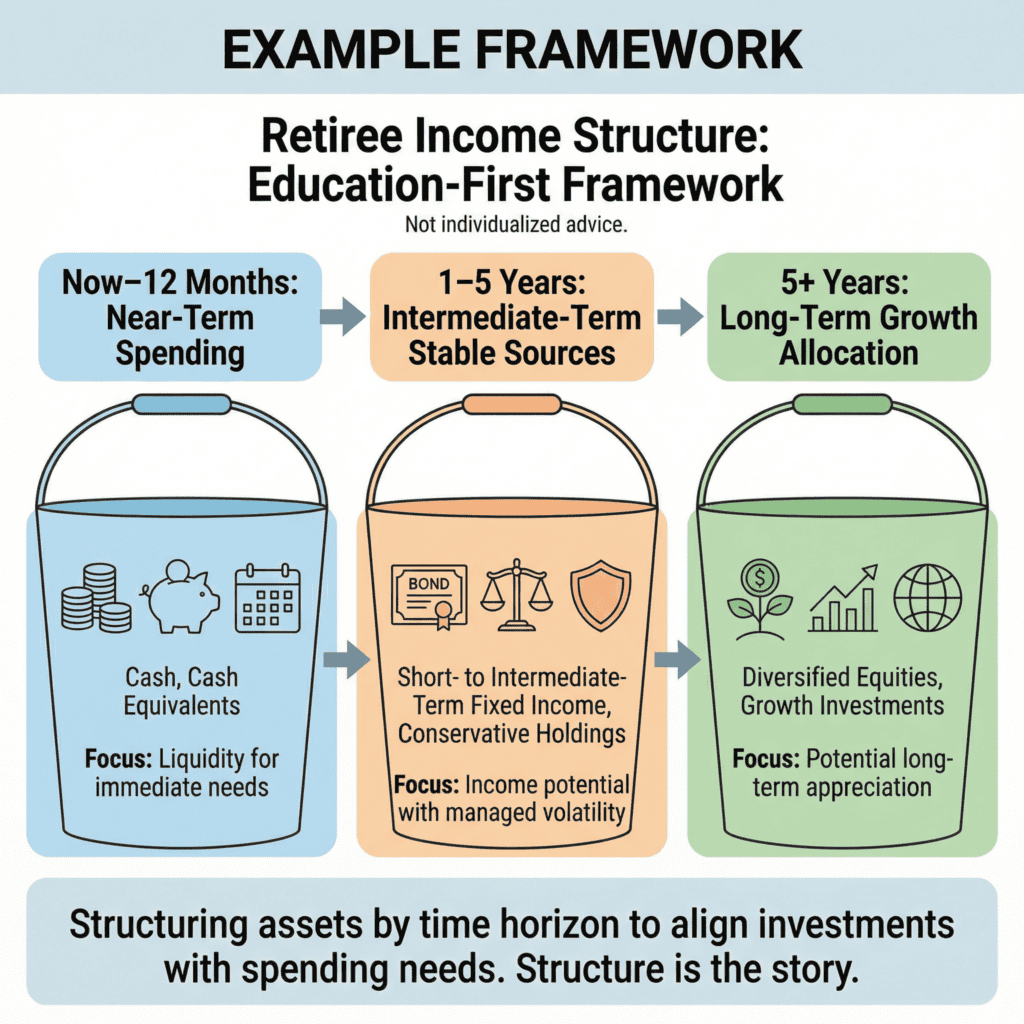

If You’re Already Retired: The Question That Actually Matters

The real issue isn’t the headline. It’s your income structure.

Ask yourself three questions:

- Do I need to sell stocks this year to fund my spending?

- Do I have six to twelve months of expenses in stable assets?

- If markets dropped 20%, would my income change or just my account balance?

That last question is the critical one.

If your income is layered with cash and stable assets covering near term needs, market swings affect your statements more than your lifestyle. If income depends on selling growth assets during downturns, volatility becomes genuinely disruptive.

The event isn’t the determining factor. Your structure is.

If You’re Five to Ten Years From Retirement: This Is a Useful Signal

This stage calls for a shift in thinking. You still need growth, but you also need resilience.

It’s worth asking whether your allocation still reflects where you’re headed, not just where you’ve been. Would a 15% market decline change your retirement timeline? Have you gradually built in some stability as the date gets closer?

Market shocks often reveal whether transition planning is ahead of schedule or behind it. Gradual adjustments made early reduce pressure later.

Why Moving to Cash Usually Doesn’t Help

Moving to the sidelines feels like control. But history shows that strong recovery periods often begin well before the headlines improve.

Missing just a handful of strong rebound days can meaningfully reduce long-term returns. And research consistently shows that investors who try to time exits and re-entries during volatility tend to underperform the market over time.

The long-term risk isn’t just market decline. It’s mistimed decisions made in response to it.

That doesn’t mean ignore risk. It means: confirm your liquidity, review your allocation, rebalance methodically if needed, and avoid making permanent changes in reaction to temporary conditions.

Discipline tends to outperform reaction.

Putting It in Perspective

Geopolitical events are serious. Markets respond quickly. Volatility can be unsettling, especially when you’re close to or already in retirement.

But most market shocks throughout history have been temporary disruptions, not permanent damage to well structured portfolios.

For retirees, the more important question isn’t whether markets will recover. It’s whether your income plan is insulated from short term declines.

For those approaching retirement, it’s whether your portfolio reflects your current stage of life, not a stage you’ve already moved past.

Retirement plans are built to last 25–30 years. They have to assume multiple downturns along the way. A plan that only works in calm markets isn’t a durable one.

The goal isn’t to eliminate volatility. It’s to eliminate the need to make reactive decisions when volatility arrives.

If recent events raised questions about whether your plan is ready for that; a calm, deliberate review now is far more valuable than a reactive decision later.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.