For several years, a small group of large technology companies drove much of the market’s return. That leadership created strong gains. It also created concentration.

Now, signs suggest leadership may be broadening. That is not unusual — markets rotate. The important question is not whether technology continues to lead. The important question is whether your retirement plan depends on it.

What “Market Leadership” Really Means

Market leadership refers to which sectors or companies are responsible for most of the market’s gains. In recent years, leadership was narrow: large-cap technology, growth-oriented companies, AI-related infrastructure.

Because major indexes are market-cap weighted, the strongest performers gained more weight automatically. If they did well, the index did well. If they stalled, the index felt it. This created a cycle where index investors became increasingly exposed to a small group of companies — often without realizing it.

That’s how concentration builds quietly.

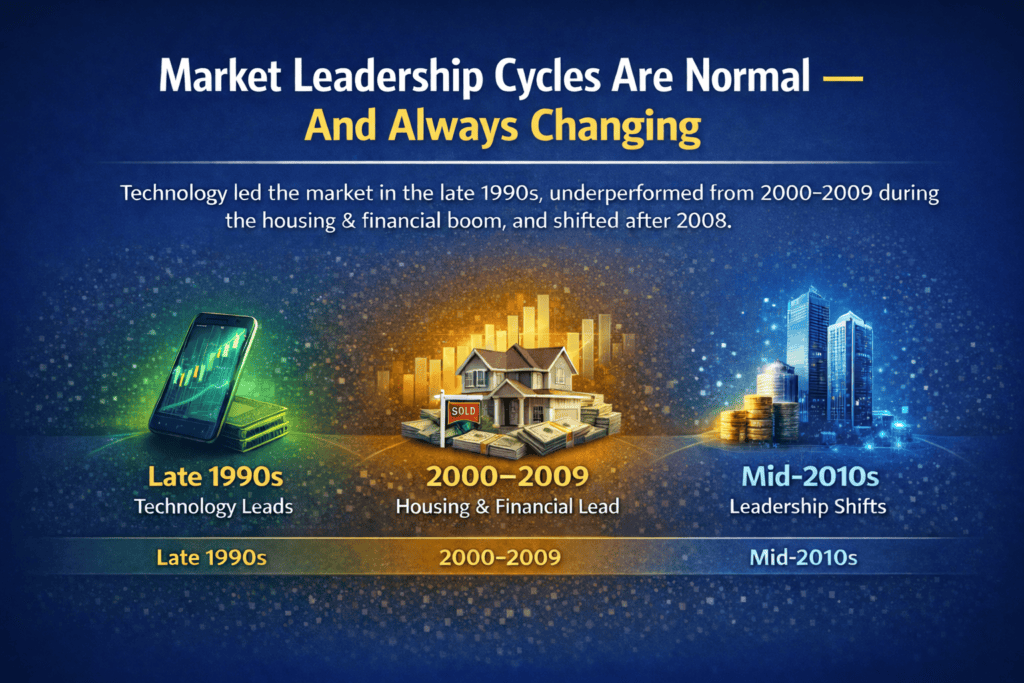

Leadership Cycles Are Normal

In the late 1990s, technology stocks led markets for years. From 2000 to 2009, technology significantly underperformed while other sectors carried returns. In the mid-2000s, housing and financial stocks dominated. After 2008, leadership shifted again.

Leadership cycles are normal. Designing a retirement plan around one cycle is not.

What Leadership Shifts Often Signal

When leadership rotates, several things tend to happen. Returns moderate in the previously dominant sector. Valuations compress — even if earnings remain solid. Capital flows into areas with steadier cash flow or lower expectations.

This doesn’t mean technology stops growing. It means markets rebalance expectations. For retirees and pre-retirees, that distinction matters, because return assumptions shape long-term planning.

Why This Matters More Near or In Retirement

If you are accumulating assets, leadership shifts are part of the journey. If you are withdrawing assets, leadership shifts change the math.

Consider a simplified example. Assume a $1,000,000 portfolio built during a strong tech cycle with a $50,000 annual withdrawal. If leadership shifts and returns moderate for several years — say from 9% to 4–5% — that difference compounds. After a 15% decline early in retirement, the portfolio drops to $850,000. The same $50,000 withdrawal now represents nearly 6%. Higher withdrawal rates make recovery more difficult, and each year spent drawing at that elevated rate deepens the gap.

That is sequence-of-returns risk. Concentration increases exposure to it. Leadership rotation is not dangerous by itself — dependence on one leadership cycle is.

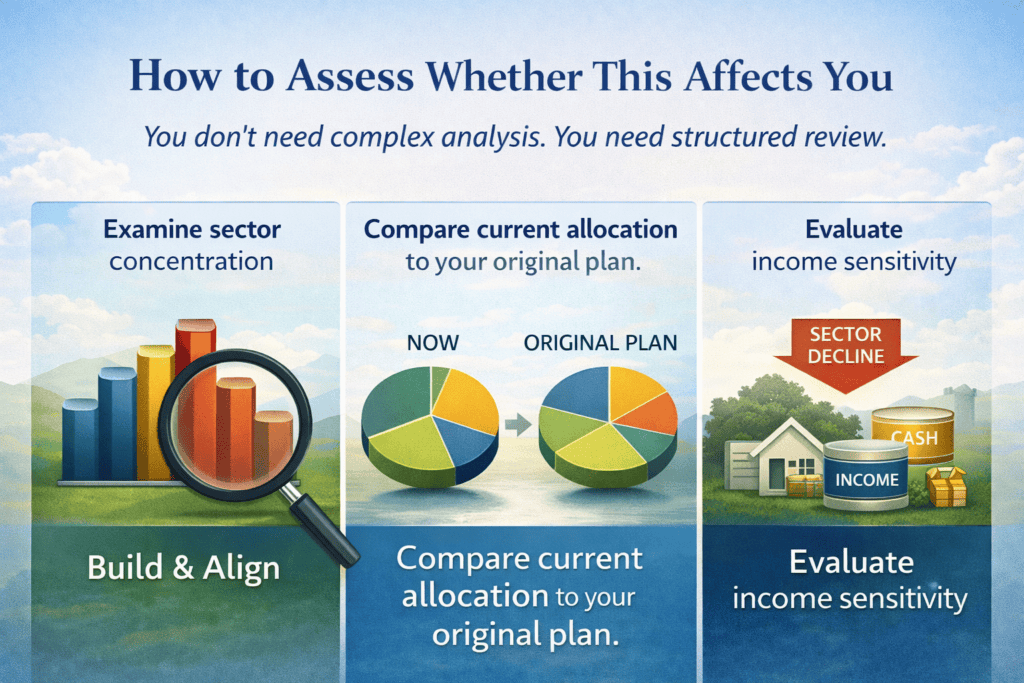

How to Assess Whether This Affects You

You don’t need complex analysis. You need structured review.

Examine sector concentration. Estimate what percentage of your equity portfolio is tied to large-cap technology, growth-oriented sectors, dividend and value sectors, and international markets. If one area exceeds 30–35%, your outcomes may be heavily influenced by that sector’s performance. That may be intentional — or it may be drift.

Compare current allocation to your original plan. Was your allocation designed this way, or did strong performance increase exposure over time? Index structures automatically overweight winners. Rebalancing is what restores discipline.

Evaluate income sensitivity. If leadership shifts for five years, does your income plan remain stable? Does your withdrawal rate stay sustainable? Can you avoid selling concentrated holdings during underperformance? Do you have income flexibility built in? The goal is not to avoid downturns. It is to avoid structural fragility.

What Pre-Retirees Should Be Thinking About

If retirement is within five to ten years, this is your adjustment window. Consider rebalancing to target allocations, revisiting forward return assumptions, and ensuring diversification across economic drivers.

If the next decade produces more moderate returns than the last, your plan should still work. Planning for moderation builds durability.

What Retirees Should Be Thinking About

If you are already drawing income, focus on flexibility.

Do you have one to three years of spending insulated from equity volatility? Can withdrawals come from multiple sources? Is your allocation aligned with current spending needs? Small allocation adjustments and coordinated withdrawal strategies often reduce long-term strain more than dramatic portfolio shifts.

A Measured Perspective

Market leadership is shifting beyond big technology. That is not a forecast — it is an observable pattern of capital rotation and valuation adjustment. Innovation will continue. Technology will evolve. But leadership rarely remains concentrated indefinitely, and retirement plans should not rely on it doing so.

If leadership broadens for the next five years, does your plan remain stable?

If the answer is yes, you are positioned thoughtfully. If the answer is unclear, that is worth reviewing before volatility forces decisions.

Retirement confidence comes from structure — not momentum.

bout the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.