Friday, the S&P 500 dropped to 6,506. You probably checked your balance. Maybe more than once.

Monday, markets bounced back 1.5%. You probably felt relief. Maybe even a little vindicated for not selling.

Here’s the problem: Neither day mattered to your plan. But they both felt like they did.

That’s the trap. Most of what feels urgent in investing is designed to make you react. Real signals that require action are quiet and measurable. They don’t scream at you from headlines.

DALBAR’s 2025 research shows this pattern costs investors an average of 8.5% per year. The average investor earned 16.5% in 2024 while the S&P 500 returned 25%. The gap wasn’t market returns. It was behavior driven by false urgency.

The Core Problem: We React to Everything

The financial media wants you anxious. Your brain wants you cautious. Both push you toward the same mistake: treating every move like it matters.

It doesn’t. In a 30-year retirement, there are maybe 15 to 20 moments when action is actually required. Everything else is noise pretending to be signal.

Research from Vanguard shows that investors who rebalance based on calendar dates (once per year, regardless of markets) outperform those who rebalance based on market moves by 0.4% annually. Why? Because calendar-based investors aren’t reacting. They’re responding to a plan.

The difference between reacting and responding: Reacting means you’re trading based on feelings. Responding means you’re making planned adjustments based on real thresholds.

The 5 Real Signals That Require Action

These are the only times your investments need to change. Not because markets moved. Because something in your actual situation changed.

Signal 1: Allocation Drift Exceeds 10%

Your plan says 60% stocks. Your actual allocation drifted to 72% stocks over the past three years as stocks outperformed bonds. That 12% difference is a real signal.

Why the 10% threshold? Research from Vanguard and Morningstar shows that drift under 5% has minimal impact on outcomes. Drift between 5% and 10% matters but isn’t urgent. Drift above 10% changes your risk profile enough to require action.

Example from this week: If you started 2024 at 60% stocks and drifted to 68% by Friday, that’s 8% drift. Friday’s drop hurt more than your plan expected, but the drift existed before Friday. The drop just revealed it.

What action looks like: Rebalancing back to your target. This usually means selling some stocks and buying bonds. Yes, even after a drop. Especially after a drop. That’s when rebalancing works best.

Key point: The signal is the drift, not Friday’s drop. If you’re at 61% stocks with a 60% target, Friday doesn’t trigger anything. If you’re at 72%, it does. Regardless of what markets did this week.

Signal 2: withdrawal rate Crosses Your Threshold

This applies to retirees and near-retirees (within 5 years of retirement).

Your withdrawal rate is how much you take out each year divided by your portfolio value. If you’re taking $50,000 from a $1 million portfolio, that’s 5%. Standard safe range based on Trinity Study research: 4% to 5.5%.

The signal triggers when your rate crosses 6.5% using recent lows, not current values. That means using Friday’s portfolio value, not Monday’s bounce.

Example: Your portfolio was $1 million. Friday it dropped to $920,000. Your withdrawal is $60,000 per year. That’s 6.52%. That’s a signal.

Why 6.5%? Trinity Study data shows withdrawal rates above 6.5% have less than 75% success rate over 30 years. Below 6.5%, success rates stay above 85%. That threshold matters.

What action looks like: Either reduce spending temporarily, increase stable asset reserves to avoid selling during drops, or adjust allocation to be more conservative. All three options reduce sequence-of-returns risk.

For pre-retirees: This signal applies if you’re modeling retirement income and your projected rate exceeds 6.5% at your planned retirement date.

Signal 3: Major Life Change

These are the big four:

● Retirement date arrives or changes

● Job loss or unexpected early retirement

● Major health event

● Large inheritance or windfall

These trigger reviews because your situation changed, not because markets moved. A job loss in your 50s changes how much risk you can take. An inheritance changes your income needs. Health events change time horizons.

Example from this week: If you were planning to retire in 2027 and your company announced layoffs this week, that’s a signal. Friday’s market drop is not. The layoff changed your timeline. The market drop is just volatility.

What action looks like: Full plan review. Income needs change, time horizon changes, risk capacity changes. This isn’t a tweak. It’s a recalculation.

Signal 4: Tax Law Changes Create New Opportunities

This is the most overlooked signal. Tax rules change, and most people don’t notice until their accountant mentions it months later.

Recent examples: RMD age changed from 72 to 73 in 2023, then to 75 in 2033. That creates new Roth conversion windows. SECURE Act 2.0 changed catch-up contribution rules. Those create planning opportunities.

Example: You’re 72. Under old rules, RMDs started this year. Under new rules, you have one more year before RMDs begin. That’s an extra year for Roth conversions at lower rates. That’s a signal.

Why this matters more than Friday’s drop: Tax rules are permanent until they change again. Market drops are temporary. Tax planning windows close. Markets recover.

What action looks like: Roth conversions, contribution strategy changes, withdrawal order adjustments. All based on new rules, not market moves.

Signal 5: Plan Failure Detected

This is the emergency signal. Something in your plan is broken. Not uncomfortable. Broken.

Three tests for plan failure:

● Liquidity crisis: Less than 6 months of spending in stable assets and you need income from portfolios

● Income gap: Essential expenses exceed guaranteed income (Social Security + pensions) by more than your portfolio can safely generate

● Sequence risk triggered: Three consecutive years of negative real returns (after inflation) early in retirement

Example from this week: If Friday’s drop meant you couldn’t cover next month’s mortgage without selling stocks at a loss, that’s a liquidity crisis. That’s not market volatility. That’s a structural problem.

What action looks like: Immediate adjustments. Reduce spending, increase stable reserves, change withdrawal strategy. This isn’t a market call. It’s triage.

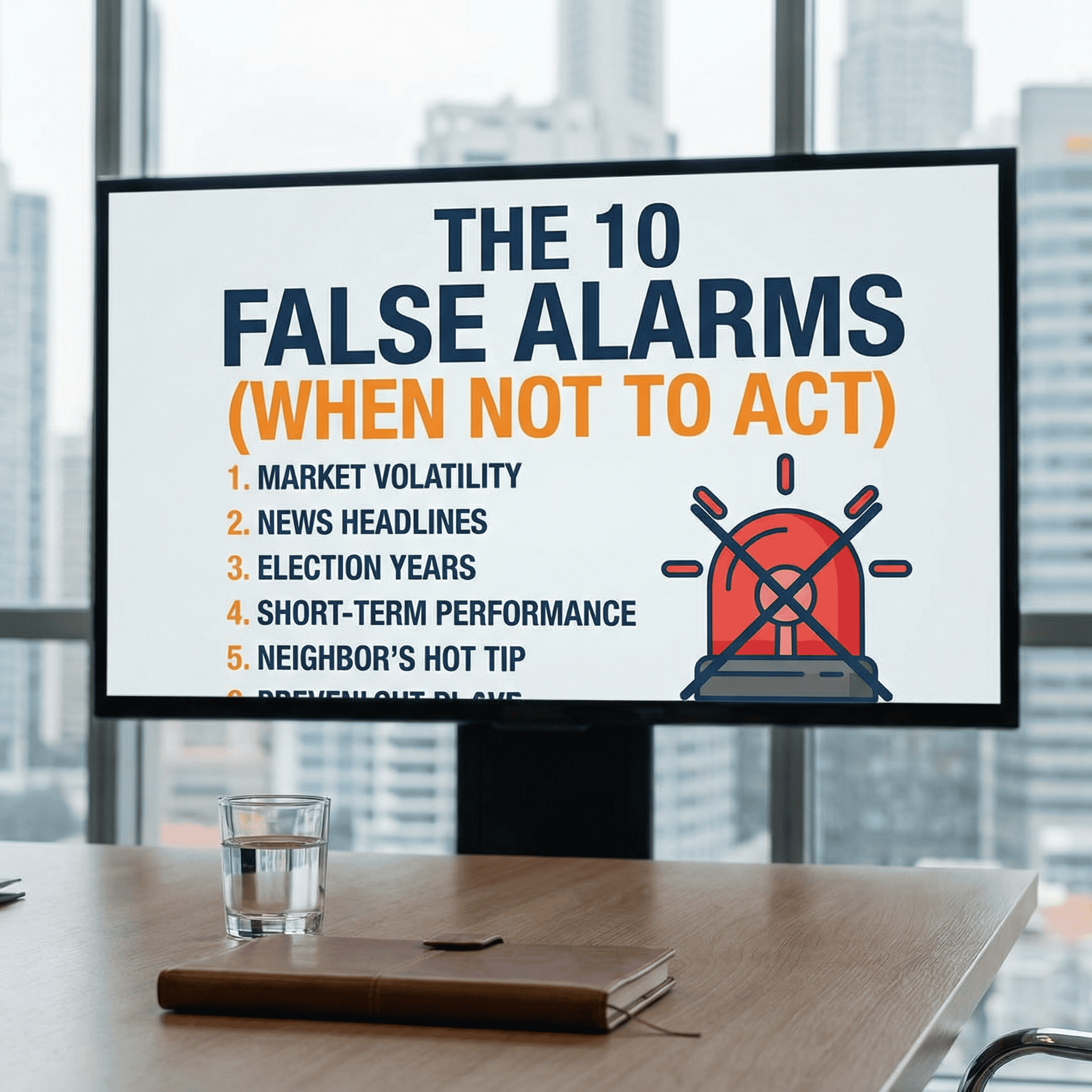

The 10 False Alarms (When NOT to Act)

Everything else is noise. Here’s what pretends to be urgent but isn’t:

False Alarm 1: Daily or Weekly Volatility

Friday’s drop and Monday’s bounce. Neither mattered unless they triggered one of the five real signals above. If your allocation is still on target and your withdrawal rate is still safe, both days were just numbers moving.

False Alarm 2: Headlines About Fed, Oil, or Geopolitics

These feel important because they’re on the news. But unless they trigger one of your five real signals, they’re just information, not action items. The Fed held rates this month. That doesn’t change your allocation target or your withdrawal rate threshold.

False Alarm 3: Friends or Family Saying ‘I’m Moving to Cash’

Your brother-in-law sold everything and feels smart because Monday bounced. His plan is not your plan. His risk tolerance is not your risk tolerance. His retirement date is not your retirement date. Ignore this completely.

False Alarm 4: One Quarter of Negative Returns

Q1 2026 is down. So what? Your plan was built to survive multiple bad years in a row, not just one bad quarter. Research shows trying to avoid negative quarters costs more than just living through them.

False Alarm 5: Your Balance Is Lower Than Last Month

This is just a number. It doesn’t tell you if your plan is working. Your withdrawal rate matters. Your allocation drift matters. The absolute number only matters in relation to those signals.

False Alarms 6-10: The Rest of the Noise

● Media creating urgency (CNBC breaking news alerts)

● Your own anxiety (‘I feel worried’ is not a signal)

● Technical market levels (correction territory, bear market, etc.)

● Election years (markets don’t care as much as media suggests)

● Expert predictions (no one can time markets reliably)

Why This Week Matters as a Teaching Moment

Friday and Monday created the perfect test case. Both felt urgent. Neither triggered any of the five real signals for most people.

If your allocation was still on target Friday morning, it’s probably still on target Monday night. If your withdrawal rate was safe before Friday, it’s probably still safe after Monday. Nothing structural changed.

What did change was how you felt. Friday created fear. Monday created relief. Both feelings pushed you toward action. That’s the trap.

The families who navigate weeks like this successfully aren’t the ones who predicted the bottom or timed the bounce. They’re the ones who knew their five signals ahead of time and checked nothing else.

How to Use This Framework

Write down your five thresholds before the next volatile week:

● My allocation drift threshold: 10% from target

● My withdrawal rate threshold: 6.5% using recent lows

● Life changes that require review: (list yours)

● Tax rule changes I’m watching: (list current ones)

● Plan failure tests: liquidity <6 months, income gap, 3-year negative sequence

When markets move, check only those five. If none triggered, close your account and go about your day. You just saved yourself from becoming another DALBAR statistic.

The Real Benefit of Knowing Your Signals

It’s not about making more money. Research shows investors who check less often don’t actually earn higher returns because they’re smarter. They earn higher returns because they trade less.

Barber and Odean’s research shows daily checkers underperform monthly checkers by 2% annually. The difference? Daily checkers find reasons to act. Monthly checkers only see what truly changed.

When you know your five real signals, you get permission to ignore everything else. That permission is worth more than any market prediction.

This week, most investors checked their balance a dozen times. They felt Friday’s panic. They felt Monday’s relief. They didn’t make any money from either feeling. They just felt things.

Investors with clear signals checked their five thresholds once. None triggered. They went back to their lives. That’s the difference.

If you’re not sure what your five thresholds should be, or you think one might have triggered this week but you’re not certain, that’s exactly what planning conversations are for. The best time to set thresholds is before the next volatile week, not during it.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

Sources

- DALBAR, Inc., Quantitative Analysis of Investor Behavior, 2025 edition

- Vanguard, “Best Practices for portfolio rebalancing,” 2024

- Trinity Study (Cooley, Hubbard, Walz), updated through 2025

- Barber, Brad M. and Terrance Odean, “Trading Is Hazardous to Your Wealth,” Journal of Finance, 2000

- Morningstar, “The Right Rebalancing Strategy for You,” 2023