Major Tax Changes Are Coming — And They Could Hit Harder Than You Expect

As we close out 2025, it’s important to understand how federal tax laws are about to change — and why 2026 could significantly increase your tax exposure in retirement.

Unless Congress passes new legislation, many of the tax breaks enacted under the 2017 Tax Cuts and Jobs Act (TCJA) are scheduled to expire on January 1, 2026. This sunset will impact everything from income tax brackets to estate tax thresholds.

While lawmakers may intervene to extend or modify parts of the law, several changes are already in motion and deserve your immediate attention before year-end.

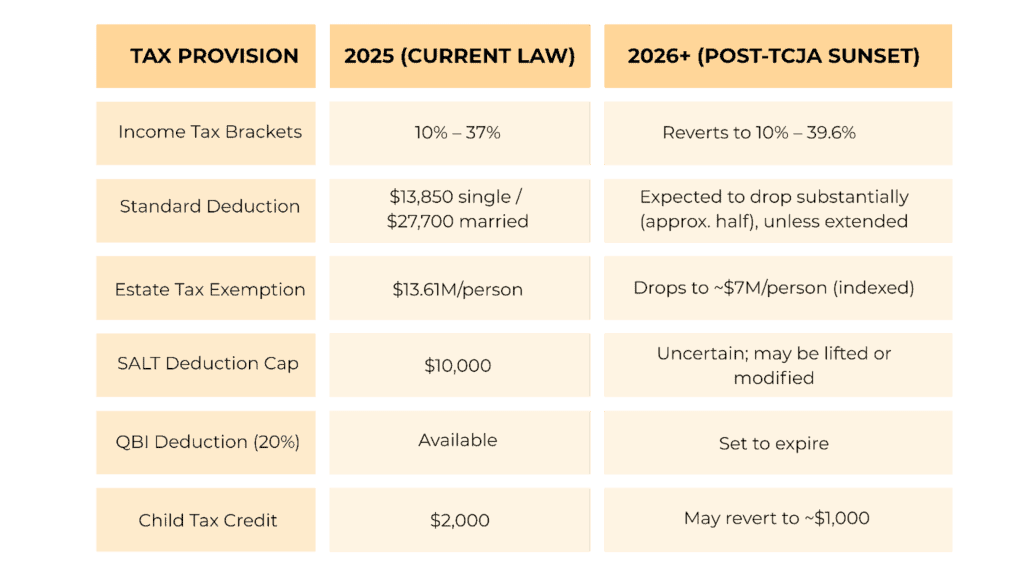

What’s Changing in 2026 — and Why It Matters

Even if your income remains steady, reverting tax rules could push you into a higher bracket with fewer deductions — especially if you’re drawing from retirement accounts.

What This Means for Pennsylvanians

Pennsylvania residents face a unique mix of federal and state tax implications:

Good news: PA does not tax Social Security benefits and excludes many types of retirement income from state taxes for individuals over age 59½.

Caution: These exclusions depend on income type and sourcing, and federal tax changes still apply.

Estate impact: While PA has no estate tax, it does have an inheritance tax: 4.5% for children, up to 15% for non-relatives.

Example: A Pennsylvania couple with $2M in investments and $280,000 in annual retirement income could see their marginal federal tax rate jump from 24% to 33% in 2026 if no legislative action occurs.

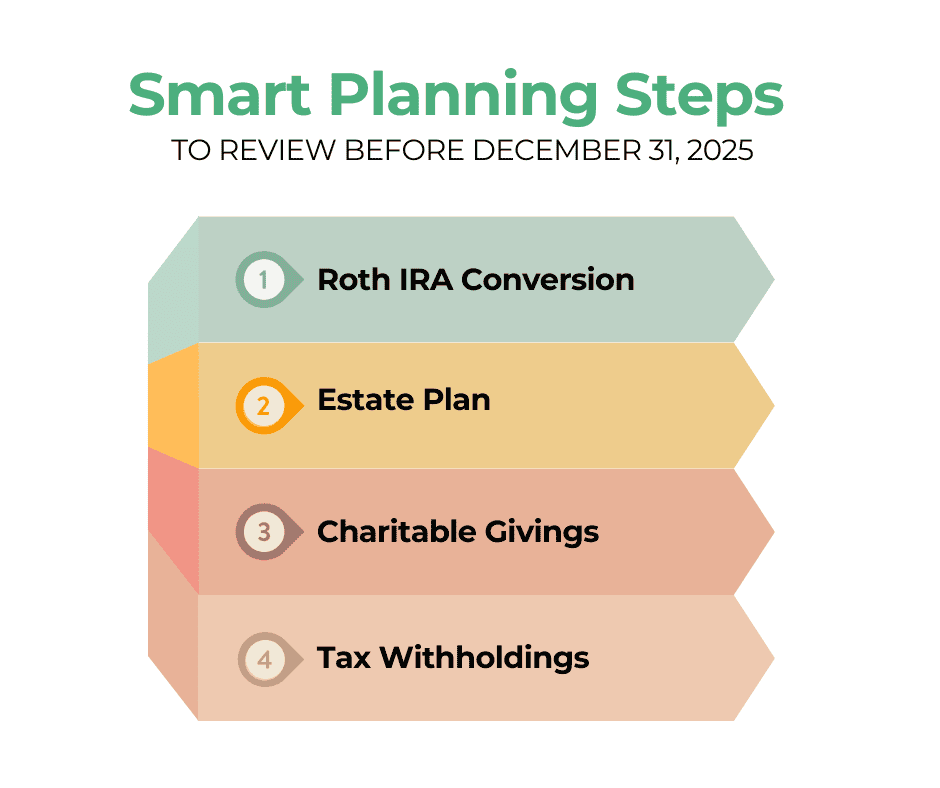

Year-End Moves to Consider in 2025

Here are smart planning steps to review before December 31, 2025:

Roth IRA Conversions

- Convert funds at today’s lower tax rates.

- Example: Converting $100,000 at 24% vs. 33% later could save $9,000 in taxes.

- PA does not tax conversions; Roth growth and withdrawals are federally tax-free.

Revisit Your Estate Plan

Lock in the higher estate tax exemption now using trusts or gifting.

Even if your estate is below $13M, dropping limits could create future exposure.

Charitable Giving Strategies

- Use Donor-Advised Funds or bunching strategies.

- Qualified Charitable Distributions (QCDs) from IRAs can lower your taxable income and count toward RMDs.

Check Withholding and Estimated Taxes

- Avoid underpayment penalties.

- Review bonuses, IRA withdrawals, investment sales, or unusual income this year.

Business Owners: Strategic Adjustments

- Reevaluate compensation methods (W-2 vs. distributions).

- Consider retirement contributions (Solo 401(k), SEP).

- Review how changes may affect your QBI deduction.

Key Stats & Takeaways

- 90% of U.S. taxpayers take the standard deduction (IRS).

- Without intervention, that figure may drop as itemizing becomes more common again.

- The Tax Policy Center estimates over 60 million Americans could face higher taxes in 2026.

- RMDs remain fully taxable and can unintentionally push retirees into higher brackets.

- PA inheritance tax still applies even in the absence of a state estate tax.

What Does 2026 Taxes Mean For Me?

2026 may not bring brand-new laws — but the return of older tax rules could dramatically reshape your retirement outlook.

If you:

- Withdraw from IRAs or other tax-deferred accounts

- Have income above $250,000

- Own a business

- Have a high-value estate

- Live in a state with inheritance tax like Pennsylvania…

Then now is the time to evaluate your exposure and coordinate with your financial planner or CPA. Small decisions before year-end could save you significantly in 2026 and beyond.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.