The Portfolio You Have vs. The Portfolio You Think You Have

Sarah looked at her year-end statement and smiled. Her portfolio was up 18%. Nothing felt broken. Then her advisor asked a simple question: “Do you know what your current stock-to-bond ratio is?”

She didn’t.

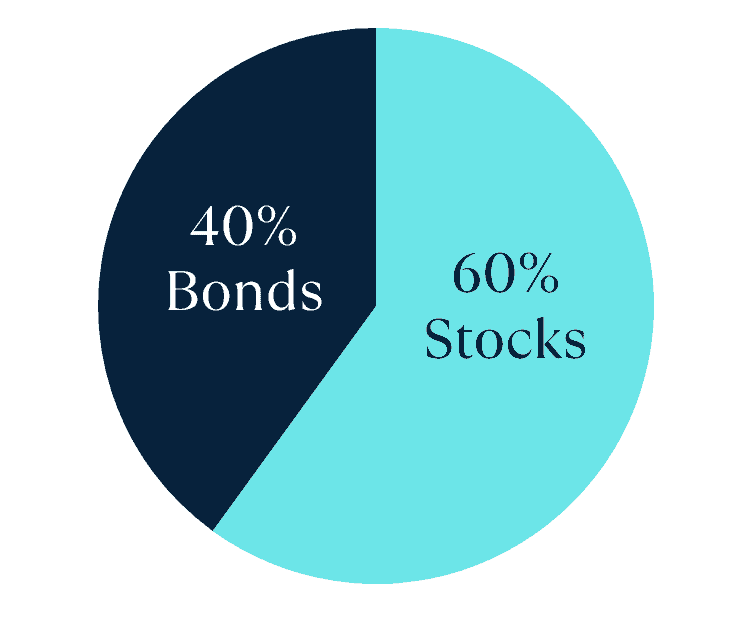

Turns out, the 60/40 portfolio she’d carefully chosen three years ago was now sitting at 73/27. Without making a single trade, her portfolio had quietly become 25% riskier than she’d intended.

“But everything’s going up,” she said. “Isn’t that good?”

“It is,” her advisor replied. “Until it isn’t.”

Six months later, when the market dropped 15%, Sarah’s portfolio fell harder than she’d expected. Not because she made a bad decision—but because she didn’t realize her portfolio had changed without her permission.

What Portfolio Drift Actually Means

Here’s what happens: When stocks grow faster than bonds, they automatically take up a bigger slice of your portfolio. You don’t buy more stocks. The math just shifts on its own.

Look at this:

| Year | Target Allocation | Actual Allocation | Drift |

| 2020 | 60% Stocks / 40% Bonds | 60% / 40% | 0% |

| 2022 | 60% / 40% | 68% / 32% | +8% stocks |

| 2024 | 60% / 40% | 75% / 25% | +15% stocks |

You didn’t change your strategy. The market changed it for you.

That 60/40 portfolio you chose because it felt balanced? It’s not balanced anymore. And if the market drops tomorrow, you’re going to feel it harder than you planned for.

Why Rebalancing Feels Backwards

Rebalancing means selling some of your winners and buying more of what hasn’t performed as well.

That feels wrong.

Every instinct tells you to let your winners run. Selling stocks that are up 30% to buy bonds that are flat seems like punishing success.

But here’s what you’re really doing:

You’re locking in gains before they disappear. You’re reducing exposure to assets that might be overpriced. You’re buying things when they’re cheaper. And most importantly, you’re protecting the plan you originally built.

Rebalancing isn’t about predicting what happens next. It’s about staying disciplined when everyone else is chasing returns or panic-selling.

That discipline is what separates people who stay on track from people who wonder what went wrong.

The Math That Matters

Let’s say you planned for a 60/40 portfolio. After a few strong years, you’re at 75/25—and you never rebalanced.

Then the market drops 20%.

At your original 60/40: You lose about 12% overall.

At your drifted 75/25: You lose about 15% overall.

That 3% difference doesn’t sound like much. But on a $1 million portfolio, that’s $30,000.

And if you’re retired and taking withdrawals? That loss compounds. You’re pulling money from a depressed portfolio, which means you’re selling assets at their lowest value—locking in losses you can never recover.

This is when people say, “I thought we were being conservative.”

You were. Until your portfolio quietly stopped being conservative.

The Hidden Stress Nobody Talks About

Portfolio drift doesn’t just create financial risk. It creates relationship stress.

One spouse looks at the balance and feels uneasy. Something doesn’t feel right, but they can’t explain what. The other spouse sees growth and wonders why anyone’s worried.

What’s actually wrong is the balance has changed. You’re not on the same page anymore because the portfolio isn’t where you both agreed it would be.

Rebalancing gives you a shared reference point. Instead of arguing about feelings, you can answer a simple question together:

“Are we still where we said we’d be?”

If not, fixing it is straightforward. And that clarity matters more than most couples realize.

Who Should Be Paying Attention Right Now?

If you’re in your 50s or early 60s and still working: Your portfolio might be carrying more risk than you realize. A downturn right before retirement could delay your plans by years.

If you’re within three to five years of retirement: This is when sequence-of-returns risk becomes real. You need to lock in gains and protect principal now—not after the market already dropped.

If you’re already retired and drawing income: Drift increases the chance you’ll be forced to sell volatile assets to cover living expenses. That’s when rebalancing supports income stability instead of just managing risk.

No matter where you are, staying on track matters more than chasing returns.

The Questions People Actually Ask

“Isn’t rebalancing just another form of market timing?”

No. Market timing is guessing what happens next. Rebalancing is following a rule you set in advance, regardless of what you think will happen.

“Will rebalancing improve my returns?”

Maybe slightly. But that’s not the point. The point is controlling risk so you can sleep at night and stick to your plan.

“How often should I do this?”

At least once a year. Or whenever your allocation drifts more than 5%. More than that and you’re probably overcomplicating it.

“Does it cost money?”

Sometimes, if you’re in taxable accounts and have to pay capital gains taxes. That’s why you need a strategy, not just a calendar reminder.

“Should retirees rebalance differently?”

Yes. When you’re taking withdrawals, timing and tax awareness matter more. This is where professional guidance pays for itself.

How to Check If Your Portfolio Has Drifted

- Pull up your most recent statement

- Calculate your current stock/bond/cash percentages

- Compare that to what you originally planned

- If the difference is more than 5%, you’ve drifted

- Decide which rebalancing rule fits your situation

- Set a calendar reminder to check again in three months

If you don’t know what your original target was—or if you’re not sure you ever had one—that’s a bigger problem than drift.

Want Someone to Look at This With You?

We built something simple called the Portfolio Drift & Rebalancing Check. It’s not a pitch. It’s not a sales meeting. It’s 10 minutes of looking at your actual numbers together.

You’ll see exactly where you are versus where you meant to be. How much risk you’re really carrying. And whether the structure you built still matches the life you’re living.

Most people leave that conversation relieved. Not because everything’s perfect—but because they finally know where they stand.

Link to tool

Or just call us. Talking through this stuff with someone who’s not emotionally invested in your portfolio helps more than you’d think.

This material is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.