What the Markets, Inflation, and Interest Rates Actually Mean for Your Money in 2026

Here’s something worth paying attention to:

The story most people are hearing about 2025 is missing some important context—and understanding what actually happened (versus what the headlines suggest) matters more than you might think.

I’m not here to predict what happens next or tell you what to do with your investments.

I’m here to help you understand what changed in 2025—so you can make better decisions about your own situation in 2026.

Most summaries of 2025 sound like this:

“Markets were up.”

“Inflation cooled.”

“Jobs stayed steady.”

And everyone breathes a sigh of relief: “Things are getting back to normal.”

That conclusion feels comforting. It’s also incomplete.

Here’s what I mean.

The Real Story of 2025: Reset, Not Recovery

Walk into any conversation about the economy right now and you’ll hear some version of:

“2025 turned out better than expected. We’re fine.”

And on the surface, that makes sense.

But here’s the distinction that matters: 2025 wasn’t a recovery year. It was a reset year.

Recovery means things go back to how they were.

Reset means conditions changed—and we’re adjusting to a new baseline.

That difference matters more than most people realize, especially when you’re making decisions about your financial future.

Let me show you what actually happened.

What the Numbers Actually Show (With Real Data)

Markets: Strong Returns, But the Journey Was Rough

What happened:

The S&P 500 finished 2025 with a 16.4% gain—a strong year by any measure, and the third straight year of double-digit returns.

What people missed:

In early April, markets dropped approximately 10% in just two days following President Trump’s sweeping tariff announcements. It was one of the sharpest two-day declines since 2020, not a smooth or orderly pullback.

Many investors panicked during that drop and moved to cash “until things settled down.”

They missed the entire recovery that followed.

Why this matters:

When markets deliver positive returns through volatility rather than smooth growth, it reveals who has an actual plan versus who’s reacting emotionally to headlines.

Inflation: Cooled Significantly, But Your Costs Didn’t

What happened:

Inflation fell from 9.1% at its peak in mid-2022 to 2.7% by November 2025—a dramatic improvement and close to the Federal Reserve’s 2% target.

What people missed:

Prices didn’t go back down. They just stopped rising as fast. Everyday costs such as food, insurance, housing, and healthcare remain materially higher than pre-pandemic levels, even though inflation has cooled.

Why this matters:

When inflation “cools,” it doesn’t mean things get cheaper. It means they stop getting more expensive at the same pace. If your financial plan assumes pre-pandemic prices, you’re underestimating your actual cost of living.

Interest Rates: Lower Than Last Year, But Not “Low”

What happened:

The Federal Reserve cut interest rates three times in 2025, bringing the federal funds target range down from 4.25%–4.50% early in the year to 3.50%–3.75% by December.

What people missed:

Even after these cuts, rates remain roughly 3+ percentage points above the near-zero environment that dominated from 2008 through 2021.

Why this matters: An entire generation of financial decisions—from home buying to portfolio construction to business borrowing—were made assuming near-zero rates would last forever.

That era is over.

Higher rates aren’t necessarily bad. They’re just different.

And different requires adjusted thinking.

Jobs: Steady, But Weakening Around the Edges

What happened:

The unemployment rate reached 4.6% by November 2025, the highest level since 2021.

Employers added just 64,000 jobs in November, well below the pace earlier in the year.

What people missed:

While overall numbers remain historically decent, hiring slowed considerably.

Federal government employment dropped by 271,000 jobs since January.

Why this matters:

A stable but weakening job market prevents immediate economic crisis, but it doesn’t create the momentum that drives sustained growth.

We’re in maintenance mode, not expansion mode.

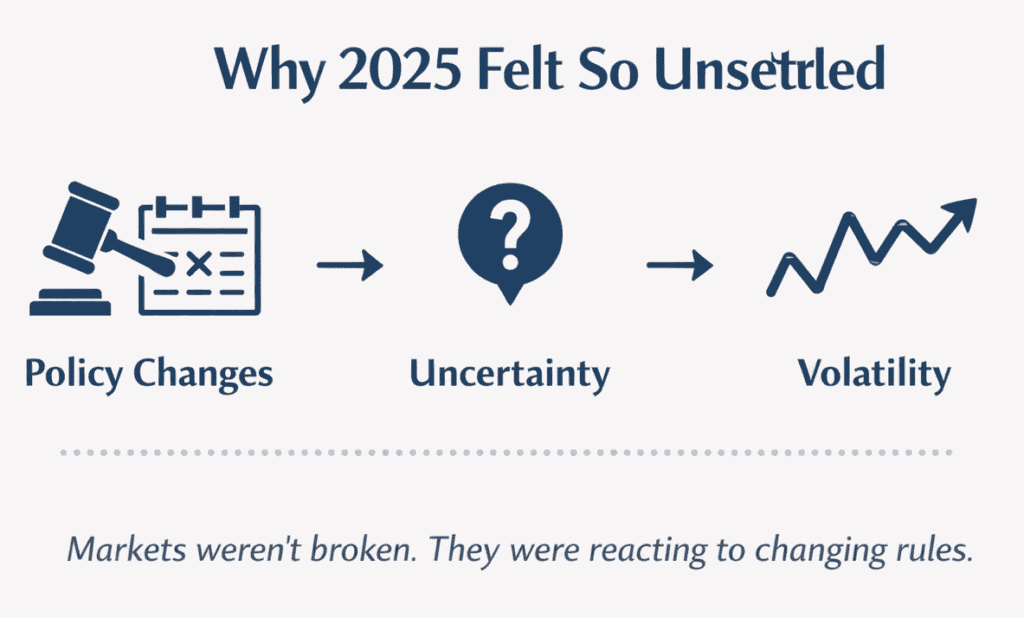

What Drove the Volatility: Policy, Not Just Markets

Understanding why 2025 was volatile helps explain why this was a reset year rather than a recovery year.

Three major policy shifts created uncertainty:

- Tariff Policy: President Trump’s April announcement of sweeping tariffs triggered one of the sharpest market sell-offs since the pandemic. When tariffs were partially rolled back roughly 90 days later, markets surged—creating prolonged uncertainty for businesses making hiring and investment decisions.

- Government Shutdown: A 43-day federal shutdown disrupted economic data collection. The Bureau of Labor Statistics was unable to conduct key October surveys, creating gaps in employment and inflation data.

- Federal Workforce Reductions: The elimination of 271,000 federal jobs affected not just employment numbers, but the delivery of government services businesses and individuals rely on.

These weren’t market-driven events. They were policy-driven events that markets had to process in real time.

The result: hesitation, delayed decisions, and whipsawing sentiment.

This is why 2025 felt stressful even though the year-end numbers looked solid.

Why “Reset” Matters More Than “Recovery”

If 2025 had been a recovery year:

- Interest rates would be back near zero

- Inflation would have pushed prices back down

- Markets would have climbed smoothly

- Everything would feel “normal” again

That’s not what happened.

Instead:

- Interest rates settled into a higher range

- Inflation cooled, but prices stayed elevated

- Markets gained ground through volatility

- Core assumptions fundamentally changed

This isn’t temporary turbulence.

This is the new normal.

What This Means for Your Money (Based on Where You Are)

The 2025 reset affects everyone differently. Here’s what matters based on your situation:

If You’re Still Building Wealth (Working Years)

The good news: Time remains your biggest advantage. If you kept investing through 2025’s volatility, you captured the full recovery.

What 2025 proved: The investors who panicked during April’s market drop and moved to cash missed a 16% annual return. The ones who kept contributing bought shares at lower prices and benefited from the rebound.

What you need to understand:

Markets being up 16% for the year doesn’t mean they rose smoothly. They dropped sharply, recovered, wobbled, and ended higher. That’s normal market behavior.

The danger isn’t volatility. The danger is abandoning your strategy because of volatility.

The higher-rate environment actually helps you:

- Your cash savings earn 4-5% again (money market funds paying real returns)

- Bonds provide actual income instead of negligible yields

- You can lock in higher rates for future needs

Your immediate opportunity: Review whether you maintained consistent contributions during 2025’s volatility. If you stopped or reduced contributions during the April drop, restart them now. You’re not investing for 2026—you’re investing for 2040-2060, and staying disciplined through volatility is what builds wealth.

If You’re Approaching Transition (Late Career/Pre-Retirement)

The reality: You’re in a critical phase—close enough that volatility matters, but far enough away that you still have time to adjust.

What 2025 proved: Market returns tell only part of the story. The bigger question is whether you understand how your money will work once you’re no longer earning a paycheck.

What you need to understand:

This economic environment changed several fundamental assumptions:

On interest rates: For over a decade, bonds paid almost nothing. Now they pay 4-5%. That’s good for generating income—but it also means bond prices fluctuate more than you might expect based on the past 15 years.

On inflation: Even though inflation is “cooling,” your cost of living reset permanently higher. If you’re planning future income needs based on pre-2022 prices, you’re underestimating by 20-25%.

On market patterns: Smooth, predictable returns were always an illusion. This environment simply makes that more obvious. Planning beats predicting.

Recent data shows that a majority of Americans approaching retirement feel uncertain whether their savings will last—not because they didn’t save enough, but because the environment changed and they haven’t updated their assumptions yet.

Your immediate opportunity: Spend 20 minutes this month answering one question: “Where will my income come from in Year 1, Year 2, and Year 3 of retirement?” Write down specific accounts and amounts. If you can’t answer this clearly, that’s your priority—not watching market movements.

If You’re Living on Your Savings (Already Retired)

The reality: You’re experiencing the economic environment directly—through monthly expenses, portfolio statements, and tax bills.

What 2025 proved: Positive years can create false confidence. Volatile years reveal whether your plan has flexibility or whether you’re just hoping things work out.

What you need to understand:

The sequence in which you experience returns matters as much as the returns themselves.

If you pulled $50,000 evenly throughout 2025, you sold some investments during April’s drop. Those shares are gone forever—they didn’t participate in the recovery.

If you had 2-3 years of expenses in cash and didn’t touch your portfolio during the drop, you preserved more principal for future growth.

On healthcare costs: Fidelity estimates a 65-year-old couple will spend approximately $330,000 on healthcare in retirement (after-tax). That assumes Medicare coverage starting at 65 and doesn’t include long-term care. These costs are based on today’s prices—which are 20-25% higher than five years ago.

On taxes: The economic environment affects your taxes in ways that aren’t always obvious:

- Social Security benefits become more taxable as other income rises

- Medicare premiums increase (IRMAA surcharges) when income crosses certain thresholds

- Required Minimum Distributions force withdrawals—and taxes—whether you need the money or not

Your immediate opportunity: Calculate your actual withdrawal rate from 2025. Take your total withdrawals, divide by your portfolio balance, and see what percentage you’re pulling. If it’s over 5%, you need more spending flexibility or risk running short. If it’s under 4%, you might have more cushion than you thought.

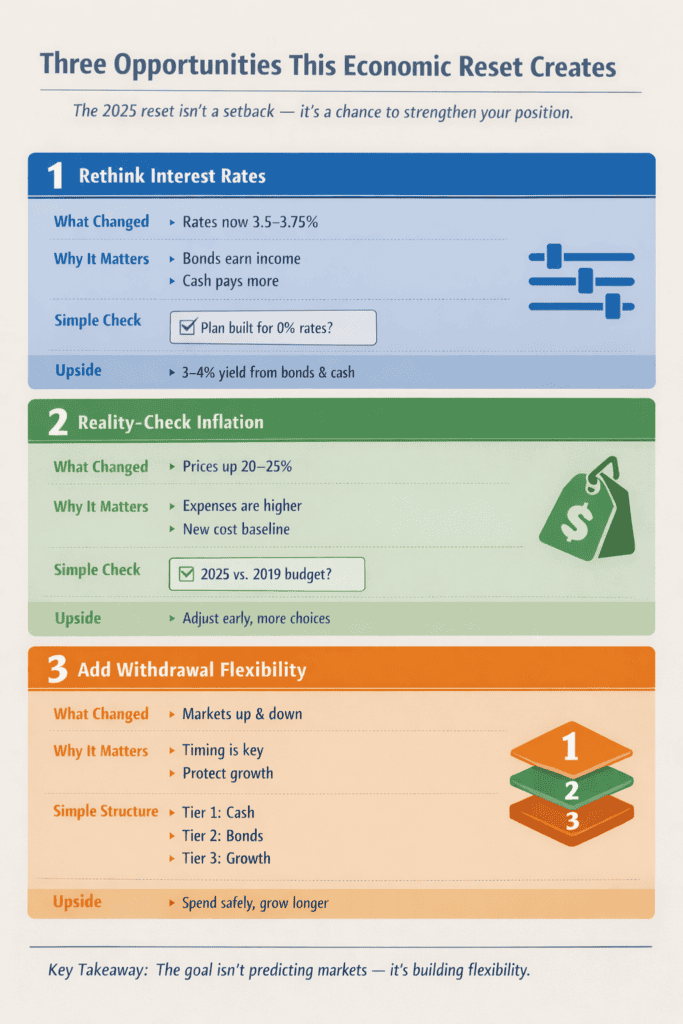

Three Opportunities This Environment Creates

Most people see the 2025 reset as a problem to worry about. I see it as creating three specific opportunities to strengthen your position:

Opportunity 1: Review Your Interest Rate Assumptions

The shift: Rates went from near-zero to 3.5-3.75%—and they’re likely staying in this range.

What this means for you:

- Bonds actually provide income again (4-5% yields)

- Cash savings earn meaningful returns (money market funds at 4-5%)

- Your portfolio allocation might need adjustment based on your timeline

Your action: Ask yourself: “Was my portfolio built assuming 0% rates forever?” If yes, review whether your current allocation still makes sense.

The upside: Higher rates mean you can generate income without taking as much risk. A balanced portfolio can now produce 3-4% yield from bonds and cash alone—something that was impossible from 2008-2021.

Opportunity 2: Stress-Test Your Inflation Assumptions

The shift: Prices reset 20-25% higher than pre-pandemic levels—and they’re staying there.

What this means for you:

- Your actual cost of living is higher than you might have budgeted

- Future increases start from this new, higher baseline

- Income needs should reflect reality, not outdated assumptions

Your action: Compare your actual monthly expenses from 2025 to what you budgeted based on 2019 costs. Calculate the difference.

The upside: If you identify a gap now, you have time to adjust. You can work longer, save more, or modify spending expectations. Finding this out at 58 is manageable. Finding it out at 68 is much harder.

Opportunity 3: Build Flexibility Into Your Withdrawal Strategy

The shift: Market volatility is back to normal (which means not smooth).

What this means for you:

- When you take money out matters as much as how much you take out

- Selling during market drops locks in losses permanently

- Having multiple sources of funds gives you options

Your action: Create a simple “tier” system:

- Tier 1: 1-2 years of expenses in cash/money market (use first)

- Tier 2: 3-5 years in bonds/stable investments (use if Tier 1 depletes)

- Tier 3: Long-term growth investments (leave alone during downturns)

The upside: When markets drop (like April 2025), you pull from Tier 1 and let your growth investments recover. When markets are up, you refill Tier 1 by taking gains. This simple system prevents the worst mistake retirees make: selling stocks at the bottom to fund living expenses.

One Simple Tool to Get Started

I know the hardest part isn’t understanding these concepts—it’s actually sitting down and reviewing your own situation.

That’s why I created The Economic Reset Checklist—a simple self-assessment that helps you see how today’s environment affects your specific situation.

The checklist covers two areas:

Market & Money – Quick checks on volatility preparedness, inflation assumptions, and interest rate impacts

Income & Planning – Simple questions about income stability, retirement structure, and whether you feel informed or just reactive

This isn’t a test. There’s no score. You don’t need to complete everything—start with whichever section feels most relevant.

👉 Download The Economic Reset Checklist

Use it this month. Take 15 minutes. Start with whichever section feels most relevant to you. You’ll either confirm you’re well-positioned for the current environment—or you’ll identify exactly what needs adjustment.

Either way, you’ll have clarity instead of uncertainty.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.