Friday, markets dropped 5%. You felt your stomach tighten. You thought about calling your advisor. Maybe you actually did.

Monday, markets bounced back. You felt better. But you still don’t know if Friday’s drop actually mattered to your plan.

Here’s the problem: Most people check their balance when they’re worried. The balance tells them what markets did. It doesn’t tell them if they’re okay.

There are four specific checks that answer the real question. Not ‘what did markets do?’ but ‘am I still on track?’

These take about three minutes total. And they give you a clear answer: either you’re fine and can stop worrying, or you need to make a call.

Why Checking Your Balance Doesn’t Help

Your balance went down Friday. It went up Monday. Both moves felt important. Neither one told you anything useful.

Think about what you actually need to know when you’re worried:

• Is my risk higher than it should be?

• Am I taking out too much?

• Do I have enough stable money to avoid selling when markets are down?

• Am I on track with my goals?

Your account balance answers none of these questions. It just shows you a number that changes daily.

Research from Barber and Odean shows that investors who check daily earn 2% less per year than investors who check monthly. The problem isn’t that daily checkers see bad news more often. The problem is that checking creates opportunities to react. And most reactions hurt.

The goal isn’t to stop checking. The goal is to check things that actually tell you if you’re okay.

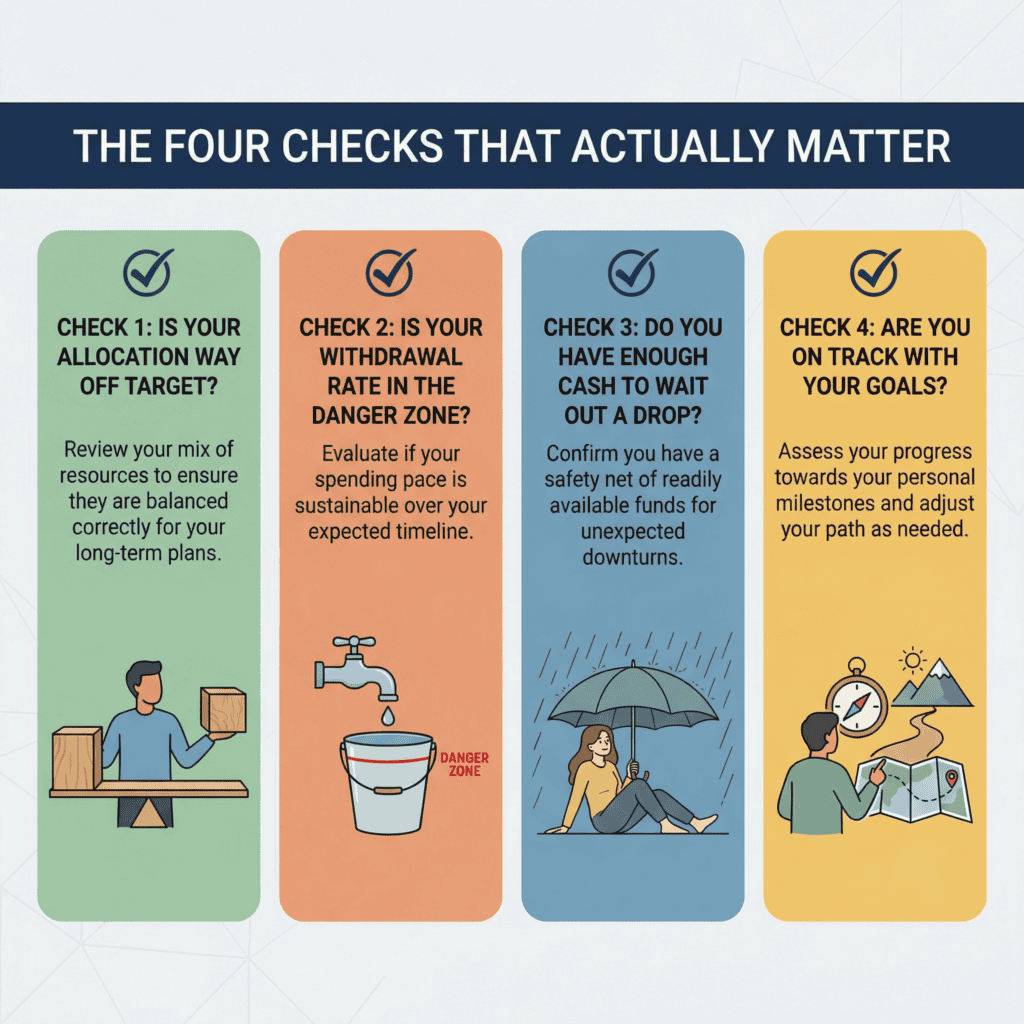

The Four Checks That Actually Matter

When you’re worried about your plan, check these four things. They tell you whether your worry is justified or just noise.

CHECK 1: IS YOUR ALLOCATION WAY OFF TARGET?

Pull up your most recent statement. Add up your stocks, bonds, and cash across all accounts. Calculate the percentages.

Compare that to your target. If you don’t have a written target, use the allocation you had when you started working with an advisor or when you set up your accounts.

Example: Your target is 60% stocks, 35% bonds, 5% cash. Your actual allocation right now is 64% stocks, 32% bonds, 4% cash.

The difference: 4% more stocks than target. That’s normal drift. Not a problem.

Same example, but your actual allocation is 72% stocks, 24% bonds, 4% cash. That’s 12% more stocks than target. That’s a real problem.

Why this matters: When you’re 12% over on stocks, market drops hurt more than your plan expected. Friday’s 5% drop hit a portfolio that was already taking more risk than it should. The drop revealed the problem. It didn’t create it.

The threshold: If you’re within 5% of your target, you’re fine. Between 5% and 10%, worth watching. Over 10%, that’s a real signal.

What it means:

• Under 5% drift: You’re fine. The worry is just volatility, not structure.

• 5-10% drift: Schedule a rebalancing conversation in the next month. Not urgent.

• Over 10% drift: Call this week. Your risk level doesn’t match your plan.

For pre-retirees: Same check. If you’re 15 years from retirement and you’ve drifted to 85% stocks when your target is 70%, that matters. Not because of Friday’s drop. Because the next bear market will hit harder than you planned for.

CHECK 2: IS YOUR WITHDRAWAL RATE IN THE DANGER ZONE?

This applies to retirees and anyone within 5 years of retirement.

Take your annual withdrawal and divide it by your current portfolio value. Not your high from last year. Not your low from Friday. Just wherever it is right now.

Example: You withdraw $50,000 per year. Your portfolio right now is $950,000. That’s 5.26%.

Compare that to the safe range. Research from the Trinity Study shows:

• Under 4%: Very safe. Room for growth even with withdrawals.

• 4% to 5.5%: Safe range. The standard target.

• 5.5% to 6.5%: Watch zone. Works in good markets, struggles in bad ones.

• Above 6.5%: Danger zone. High failure rate over 30 years.

If you’re at 5.26%, you’re in the safe range. Friday’s drop didn’t change that. You can stop worrying.

If you’re at 6.8%, you have a problem. Not because markets dropped Friday. Because your withdrawal rate was already too high. Friday just made it visible.

The threshold: Under 5.5% means you’re okay. 5.5% to 6.5% means have a conversation soon. Above 6.5% means call this week.

Why this check beats checking your balance: Your balance tells you what happened to markets. Your withdrawal rate tells you whether your plan can survive what markets do next.

For pre-retirees: Calculate your projected rate. If you plan to withdraw $60,000 annually starting in three years and your portfolio is $850,000 today, that’s 7%. That tells you to either save more now or plan to spend less. That matters more than any single day’s market move.

CHECK 3: DO YOU HAVE ENOUGH CASH TO WAIT OUT A DROP?

Add up everything in stable accounts. Checking, savings, money markets, CDs, bonds that mature in the next 12 months.

Divide that total by your monthly spending. That tells you how many months you can cover without selling stocks.

Example: $60,000 in stable money. $4,000 monthly spending. That’s 15 months of coverage.

Why this matters: If you have 15 months of coverage, Friday’s drop doesn’t force you to do anything. You can wait 15 months for markets to recover before you need to sell stocks. That’s what makes volatile weeks survivable.

If you have 4 months of coverage, Friday’s drop is a different situation. You don’t have time to wait. That creates pressure to sell at the wrong time.

The threshold: 12 to 24 months is ideal for retirees. 6 to 12 months works for pre-retirees with steady income. Under 6 months creates real pressure during drops.

What it means:

• 12+ months: You’re fine. Market drops don’t create income pressure.

• 6-12 months: Not urgent, but worth refilling soon.

• Under 6 months: This needs attention now. You’re one bad quarter away from forced selling.

This check is what turns Friday’s drop from scary to manageable. Same portfolio value. Same market move. But with 18 months of coverage, it’s just volatility. With 4 months of coverage, it’s a crisis.

CHECK 4: ARE YOU ON TRACK WITH YOUR GOALS?

This check looks different depending on where you are.

For pre-retirees: Are you on pace to hit your savings targets for the year? If your goal is $30,000 in total contributions and it’s the end of March, you should be around $7,500. If you’re at $4,000, you’re behind.

Why this matters: Being behind on contributions has nothing to do with Friday’s market drop. But if you’re focused on the drop, you miss the more important problem. Small gaps in contributions compound dramatically over decades.

For retirees: Are your expected income sources hitting your accounts as expected? Social Security, pension, required distributions. Errors happen. Missing a pension payment matters more than Friday’s market move.

The point: Market drops feel urgent. Being behind on contributions or missing income payments are actually urgent. This check makes sure you’re focused on the right problem.

What to Do After Your Four Checks

You just checked four things. Now you have clear information instead of vague worry.

IF ALL FOUR CHECKS PASSED:

• withdrawal rate under 5.5% (or on track for pre-retirees)

• liquidity coverage above 12 months

• Goals on track

Then Friday’s drop didn’t matter to your plan. Close your account. Stop checking. You just proved to yourself that you’re okay. The worry was volatility, not structure.

IF ONE OR TWO CHECKS ARE IN THE YELLOW ZONE:

• Drift between 5% and 10%

• Withdrawal rate between 5.5% and 6.5%

• Liquidity between 6 and 12 months

• Slightly behind on goals

Schedule a conversation in the next few weeks. Not urgent, but worth addressing before the next volatile week. These are adjustments, not emergencies.

IF ANY CHECK IS IN THE RED ZONE:

• Drift over 10%

• Withdrawal rate over 6.5%

• Liquidity under 6 months

• Significantly off track with goals

Call this week. These aren’t market calls. They’re plan maintenance that’s overdue. Your advisor should welcome these calls because they’re based on real thresholds, not panic.

Why This Works When Balance-Checking Doesn’t

Checking your balance when you’re worried gives you a number. That number might be lower than last week. That creates more worry. You check again tomorrow. The cycle continues.

These four checks give you an outcome. Either you passed and can relax, or you found a specific problem you can fix. Either way, the worry stops because you have information instead of just a number.

This week proved the difference. Investors who checked their balance Friday and Monday experienced volatility as emotion. They felt worse Friday. They felt better Monday. But they still don’t know if they’re okay.

Investors who ran these four checks know exactly where they stand. If all four passed, they’re done worrying. If one flagged, they know exactly what to address. Same market moves. Completely different experience.

The Real Benefit: Permission to Stop Checking

Most people check their accounts because they don’t know if they’re okay. These four checks answer that question directly.

Once you know you’re okay, you can stop checking. Not because you’re ignoring risk. Because you’ve already checked the things that matter.

Research shows this pattern clearly. Investors who check less often don’t do better because they’re lucky. They do better because they trade less. Every time you check, you create an opportunity to react. Most reactions hurt more than they help.

The goal isn’t to never check. The goal is to check the right things, get a clear answer, then stop until something actually changes.

when to run these checks again

Two situations trigger these checks:

SITUATION 1: YOU’RE WORRIED

Markets dropped. Headlines are scary. You’re thinking about calling your advisor. Before you call, run these four checks. They take three minutes. They’ll tell you if your worry is justified or just volatility.

SITUATION 2: SOMETHING IN YOUR LIFE CHANGED

You retired. You changed jobs. You inherited money. You had a health event. Life changes trigger plan changes. Run these four checks to see what needs adjusting.

Everything else? You don’t need to check. If markets drop and nothing in your life changed and you’re not worried, you can skip it entirely. Your plan was built to survive drops. These checks just confirm it’s still working as designed.

If you ran these checks this week and everything passed, congratulations. Friday’s drop was just noise. If something flagged, now you know exactly what needs attention. Either way, you have clarity instead of just worry.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

Sources

Barber, Brad M. and Terrance Odean, “Trading Is Hazardous to Your Wealth,” Journal of Finance, 2000

Trinity Study (Cooley, Hubbard, Walz), updated through 2025

Vanguard, “Best Practices for Portfolio Rebalancing,” 2024

DALBAR, Inc., Quantitative Analysis of Investor Behavior, 2025 edition