How Social Security, Taxes, Medicare, and Income Change When One Spouse Dies

Subscribe to The Confident Retirement Brief for weekly planning insights.

Key Takeaways

- When a spouse dies, Social Security income drops 30-40% because survivors keep only the larger check.

- Surviving spouses often face higher tax rates filing single despite earning significantly less income.

- Couples should stress-test their retirement plan now by modeling finances on one income only.

- Medicare premiums can increase for surviving spouses whose income crosses IRMAA thresholds after death.

- Shared expenses don’t drop by half at death, creating a dangerous income-to-expense gap for survivors.

Most retirement plans are built for two people. Two Social Security checks. Joint tax filing.

Shared expenses. Two people making decisions together.

That plan may work well for years. It may be carefully designed and regularly reviewed. But many couples never ask the question that matters most: what happens to this plan if only one of us is here to use it?

When one spouse dies, the financial picture does not simply shrink. It changes shape. Income drops, but not evenly.

Expenses drop, but not by half. Tax rates often go up. Medicare costs may increase.

And the surviving spouse has to manage all of it alone, often while grieving.

This article walks through what actually changes, and what couples can do now to close the gap before it matters.

What Happens to Social Security When a Spouse Dies

When one spouse dies, the surviving spouse keeps the larger of the two Social Security checks and loses the smaller one. The surviving spouse does not keep both.

For many couples, this means a sudden loss of $1,500 to $2,500 per month in household income. The amount depends on the claiming ages and earnings histories of both spouses.

Hypothetical scenario:

A couple receives Social Security of approximately $2,800 per month (higher earner) and approximately $1,600 per month (lower earner). Combined: approximately $4,400 per month. When the higher earner dies, the surviving spouse keeps the $2,800 check and loses the $1,600 check.

Monthly income drops by approximately $1,600, or roughly 36%. But the mortgage, property taxes, utilities, and insurance do not drop by 36%. Individual results will vary.

This is why the higher earner’s Social Security claiming age is often described as a form of life insurance. A higher earner who delays claiming from 62 to 70 may increase the survivor benefit by roughly $1,000 or more per month. That difference lasts for the rest of the surviving spouse’s life.

Women who are 62 today have an average life expectancy of roughly 86, compared to roughly 83 for men, according to Social Security Administration actuarial tables. In many couples, the person who makes the claiming decision is not the person who lives with the consequences the longest.

What Happens to Taxes When a Spouse Dies

This is the change that surprises most families. After a spouse dies, the surviving spouse files as single beginning the following tax year (or in the year of death, they may file jointly for that final year).

Single filer tax brackets are roughly half as wide as married filing jointly brackets. That means the surviving spouse could pay a higher tax rate on less total income.

Hypothetical scenario:

A couple with approximately $110,000 in combined income files jointly and stays in the 22% bracket (which applies up to roughly $201,050 for joint filers in 2026). After one spouse dies, the survivor has approximately $75,000 in income. As a single filer, the 22% bracket applies only up to roughly $100,525.

The survivor may still be in the 22% bracket, but with less room before moving to 24%. And income that was comfortably in the 12% bracket as a couple may now land in the 22% bracket as a single filer. Individual results will vary.

This is sometimes called the “widow’s tax penalty.” It is not a separate tax. It is the structural result of bracket compression when filing status changes. The surviving spouse may pay thousands more in taxes on income that is actually lower than what the household earned as a couple.

The new $6,000 senior deduction (from the One Big Beautiful Bill Act, available to filers 65 and older for tax years 2025 through 2028) may help offset some of this. For a joint filing couple where both spouses are 65 or older, the combined deduction could be $12,000. After one spouse dies, it drops to $6,000. The deduction phases out for single filers with income above roughly $75,000.

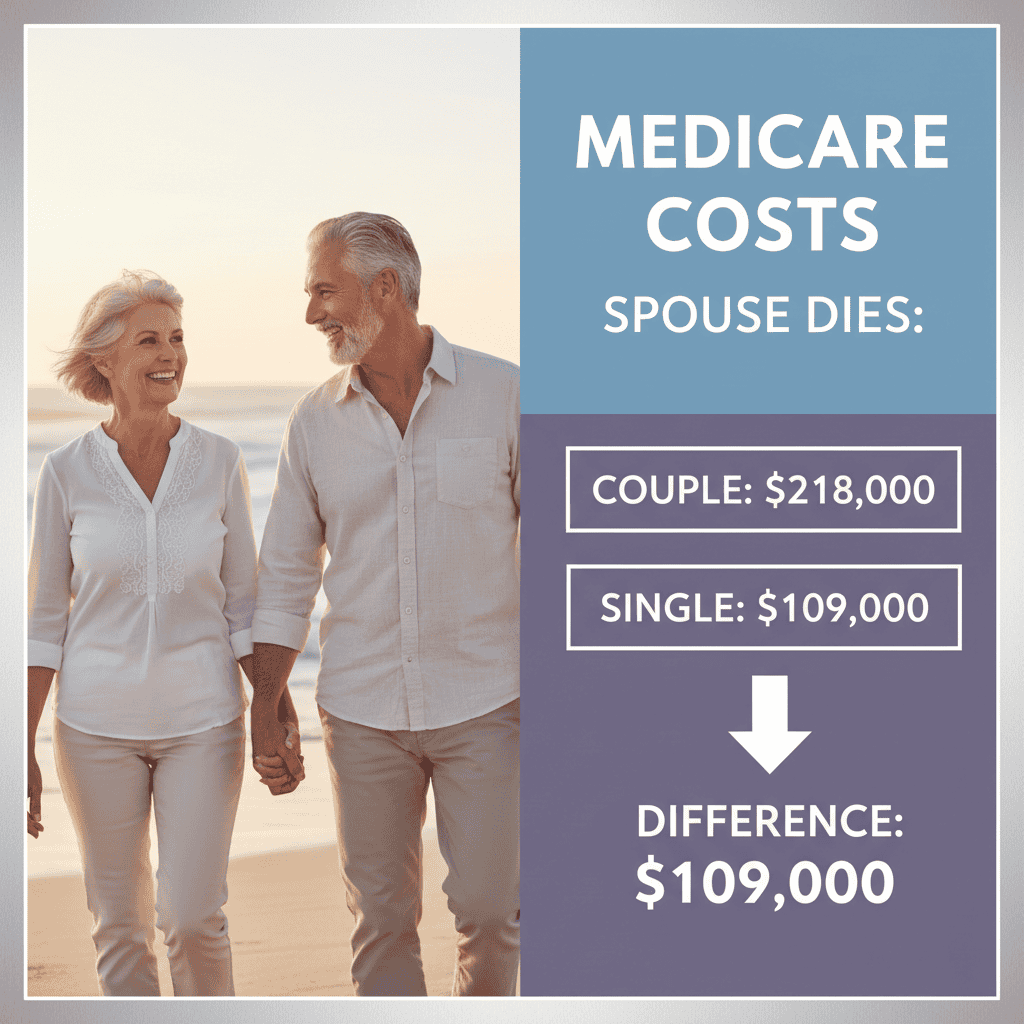

What Happens to Medicare Costs When a Spouse Dies

Medicare Part B and Part D premiums include income-related surcharges called IRMAA (Income-Related Monthly Adjustment Amount). These surcharges are based on income from two years prior.

The first IRMAA threshold for 2026 is $218,000 for married couples filing jointly. For a single filer, it drops to $109,000. That is a difference of $109,000.

A couple with $180,000 in combined income is well below the joint threshold and pays no surcharge. After one spouse dies, the survivor may have $100,000 to $120,000 in income. As a single filer, that could push them above the $109,000 threshold, triggering surcharges that did not exist while both spouses were alive.

The surcharge applies to the entire tier, not just the income above the line. And because IRMAA uses a two-year lookback, the higher premiums may arrive during a year when the surviving spouse’s actual income has already dropped.

What Happens to Pension and Annuity Income When a Spouse Dies

Many pensions offer a choice at the time of retirement: take a higher monthly payment with no survivor benefit, or take a reduced payment that continues for the surviving spouse.

This election is often made once, at retirement, and cannot be changed. Some pensions offer 100% survivor benefits (the full payment continues). Others offer 50% or even 0% survivor options. The choice between these options affects the pensioner’s monthly income for the rest of their life, and the surviving spouse’s income after that.

If the pensioner chose the “life only” option (0% survivor benefit) to maximize monthly income, the full pension disappears when they die. If they chose 50%, the surviving spouse receives half. Many surviving spouses discover this only after the death, when the first reduced check arrives.

If you have a pension, check which survivor option was elected. If you do not know, call the plan administrator. This is one of the most important numbers in any survivor income analysis.

Wondering how your retirement plan holds up on one income? Most couples are surprised by what the numbers reveal. Schedule a conversation with our team to stress-test your plan before life makes the decision for you.

What Happens to the Accounts and the House

Beyond income, there is the structural question of how assets transfer. This is where estate planning and survivor planning overlap.

Retirement accounts (IRAs, 401(k)s) with a named beneficiary pass directly to that beneficiary. They do not go through probate. Life insurance with a named beneficiary works the same way. Bank accounts with payable-on-death designations pass directly.

Real estate owned jointly with right of survivorship passes automatically to the surviving spouse in most cases. But real estate owned individually, or owned in one spouse’s name only, may need to go through probate. In Pennsylvania, probate typically takes 9 to 18 months.

The key question is whether the surviving spouse has to go through a legal process to access money they need to live on. If accounts are properly titled and beneficiary designations are current, the answer is usually no. But if any major asset lacks a designation or is titled incorrectly, it could mean months of delay and unnecessary legal costs during one of the hardest periods of a person’s life.

This is also why beneficiary designations need to be reviewed regularly. They override wills. An outdated designation could send assets to an ex-spouse, a deceased relative, or someone you did not intend.

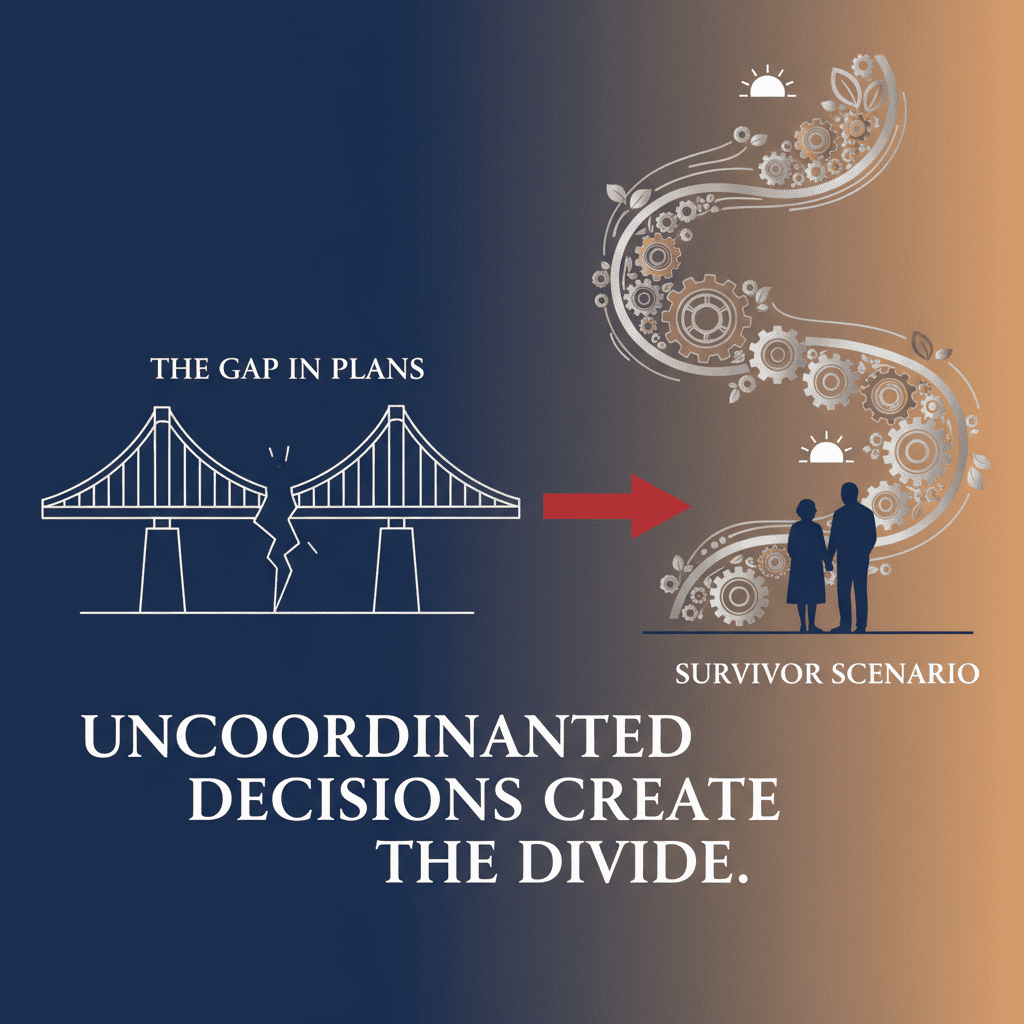

What Couples Can Do Now to Close the Survivor Income Gap

The gap between a plan that works for two and one that works for one is usually not caused by a single mistake. It is caused by decisions that were never coordinated with the survivor scenario in mind.

Here are the areas worth reviewing.

Check the higher earner’s Social Security claiming age. If the higher earner has not yet claimed, delaying to 70 may increase the survivor benefit by hundreds of dollars per month for life. This is one of the most cost-effective forms of survivor protection available.

Know the pension survivor election. If either spouse has a pension, confirm which survivor option was elected. If it was a “life only” option, understand that the full pension disappears at death. If it was a reduced survivor option, know the amount.

Run the tax math as a single filer. Take your current household income, remove one Social Security check and any pension or income that would disappear, and check what bracket the remaining income falls into as a single filer. If the effective tax rate goes up, consider whether Roth conversions now could reduce future tax exposure for the surviving spouse.

Check IRMAA exposure at the single threshold. If your household income is within $30,000 of the $109,000 single-filer IRMAA threshold, the surviving spouse could be at risk of surcharges. Managing income sources proactively may help avoid crossing a tier.

Review every beneficiary designation. Confirm that every retirement account, life insurance policy, and bank account has a current, correct beneficiary. If any designation is missing, outdated, or names a deceased person, update it this week.

Confirm how real estate and major accounts are titled. Assets owned jointly with right of survivorship or with proper designations pass without probate. Assets owned individually may require probate. In Pennsylvania, this distinction could mean the difference between the surviving spouse having immediate access to funds and waiting 9 to 18 months.

Consider whether a trust makes sense for your situation. For some families, a trust may simplify the transfer of assets, provide control over how and when heirs receive them, and avoid the time and cost of probate. For others, proper titling and beneficiary designations may be sufficient. This week’s companion article, “Do You Actually Need a Trust?” walks through how to evaluate this for your specific situation in Pennsylvania.

If You Are Already a Surviving Spouse

If you have already lost a spouse, some of these decisions are in the past. But several things can still be improved.

You may be able to adjust your withdrawal sequence to manage tax bracket exposure as a single filer. You may benefit from the $6,000 senior deduction if you are 65 or older. You may be able to manage income to stay below an IRMAA threshold. And you should review your own beneficiary designations and estate documents now that your circumstances have changed.

The fact that some choices cannot be undone does not mean nothing can be done. Optimizing around the current situation is always worthwhile.

The Conversation Worth Having

This is not a comfortable topic. Most couples avoid it because it feels premature, morbid, or simply hard to talk about.

But the families who fare best are not the ones who had perfect foresight. They are the ones who sat down together, asked what would happen if one of them was not here, and made sure the plan accounted for that reality.

The gap between a plan that works for two and one that works for one is usually fixable. But it is much easier to fix while both people are at the table.

Worth Sharing

If you know a couple who has never had this conversation, or a friend who recently lost a spouse and is navigating changes alone, this article may help them see the full picture. Forward it or share the link.

Is Your Plan Built for One or Two?

If this article raised a question about how your plan would hold up for the surviving spouse, that is worth a 30-minute conversation. No cost. No obligation.

Schedule a Complimentary Conversation

Curious how Social Security, taxes, and Medicare could shift for your surviving spouse? Subscribe to The Confident Retirement Brief for weekly insights designed to help you spot gaps and explore strategies before they become crises.

Related: Do You Actually Need a Trust? A Plain-Language Guide for Pennsylvania Families

Subscribe to The Confident Retirement Brief for weekly planning insights.

About Langan Financial Group

Langan Financial Group provides personalized retirement planning, investment management, and income coordination for individuals and families in central Pennsylvania and beyond. Located at 1863 Center St., Camp Hill, PA 17011. langanfinancialgroup.com/get-started-today | 717-288-1880

DISCLOSURE: This article is provided for informational and educational purposes only and does not constitute investment advice, financial planning advice, tax advice, or legal advice. All investing involves risk, including potential loss of principal. Past performance is not an indicator of future results.

Dollar amounts in hypothetical scenarios are approximate and labeled for illustration only. Individual results will vary based on specific financial circumstances. Social Security benefit amounts depend on individual earnings history and claiming age.

Tax bracket thresholds, IRMAA thresholds, and deduction amounts are based on 2026 figures and are subject to change. Survivor benefit, pension election, and estate planning decisions should be made in consultation with qualified financial, tax, and legal professionals. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC.

Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.