One Social Security Decision, Six Financial Consequences

How Your Claiming Age Affects Your Taxes, Your Healthcare, Your Investments, Your Savings, and Your Spouse

“When should I take Social Security?” is the most common question in retirement planning. But it is not one question. It is at least eight.

When you claim affects your monthly check. But it also changes your tax bill, your healthcare costs, how fast you burn through savings, what your spouse receives if you die first, and whether you have a window to reduce your lifetime taxes. Most families only look at the first one. This article walks through all of them.

How Does Taking Social Security at Different Ages Change Your Payout?

For everyone born in 1960 or later, full retirement age (FRA) is 67. That is the age when you receive 100% of the benefit you earned, according to the Social Security Administration.

Claim earlier and your benefit shrinks. Claim later and it grows. Both changes are permanent.

At age 62, your benefit is reduced by 30%. At age 70, it increases by 24% above your full benefit, bringing you to 124% of what you earned. That boost comes from delayed retirement credits of 8% per year between ages 67 and 70.

To put that in dollar terms: the maximum Social Security benefit for 2026 is roughly $2,969 per month at age 62, roughly $4,152 at full retirement age, and roughly $5,181 at 70, according to the SSA. Most people will not reach these maximums. But they show the range.

Hypothetical scenario: A person with a full benefit of $2,400 per month at 67 would receive roughly $1,680 at 62 or roughly $2,976 at 70. Over a full retirement, that gap could exceed $100,000 for someone who lives into their mid-80s, and significantly more for someone who lives longer. Individual results will vary based on earnings history and other factors.

According to the JPMorgan Guide to Retirement, the break-even age for delaying from 62 to 70 typically falls around age 80 to 82. Average life expectancy for a 62-year-old is roughly 83 for men and 86 for women (SSA actuarial tables). For most people, the math favors waiting. But the monthly check is only one piece of the picture.

How Does Social Security Timing Affect Health Insurance?

This is the connection almost nobody talks about. And it works differently before and after age 65.

Before age 65: ACA marketplace subsidies. If you retire before Medicare starts at 65, you likely need marketplace health insurance. In 2026, the expanded subsidies from 2021 through 2025 have expired. The “subsidy cliff” is back. If your household income exceeds 400% of the federal poverty level (roughly $82,000 for a couple, based on 2025 FPL guidelines used for 2026 coverage), you lose the subsidy entirely.

Here is the catch. The ACA counts 100% of your Social Security benefits as income for subsidy purposes. Not 50%.

Not 85%. All of it. The IRS only taxes up to 85% of benefits.

But the ACA marketplace uses every dollar.

That means claiming Social Security at 62 while you are on marketplace insurance can add enough income to push you over the cliff. You could lose $15,000 to $25,000 per year in premium help. In some cases, the lost subsidy costs more than the Social Security check itself. Delaying the claim and drawing from a Roth or taxable account instead may keep ACA income low enough to keep the subsidy.

After age 65: Medicare IRMAA surcharges. Medicare Part B and Part D premiums are based on your income from two years prior. For 2026, a married couple filing jointly with modified adjusted gross income above $218,000 pays higher premiums through the IRMAA surcharge. For a single filer, the threshold drops to $109,000.

Your claiming age affects IRMAA because it changes how much other income you need to pull from savings. Claiming early means a smaller check, which often means larger 401(k) withdrawals, which means higher total income. That can trigger the surcharge.

How Does Social Security Timing Affect Taxes?

Most people assume Social Security is not taxed. For many retirees, it is.

Up to 85% of Social Security benefits can be subject to federal income tax. The thresholds that trigger this have not changed since 1994. They are not adjusted for inflation. Combined income means your adjusted gross income, plus any tax-exempt interest, plus half of your Social Security benefits.

For a married couple filing jointly: below $32,000 in combined income, benefits are not taxed. Between $32,000 and $44,000, up to 50% may be taxed. Above $44,000, up to 85% may be taxed. Those thresholds are so low that most retirees with any income beyond Social Security will hit the 85% level.

This creates what is sometimes called the “tax torpedo.” In the zone between 50% and 85% taxability, each extra dollar of income can cause $1.85 in taxable income. The dollar itself, plus the added Social Security that becomes taxable because of it. That effective tax rate surprises many retirees.

Your claiming age matters here because it determines how much other income you need. If you claim early and receive a smaller check, you pull more from the 401(k) to make up the difference. Both the 401(k) withdrawal and the Social Security show up on your tax return. Together they can push you well above the 85% threshold.

The new $6,000 senior deduction from the One Big Beautiful Bill Act (2025) may help some retirees. It applies to taxpayers 65 and older for tax years 2025 through 2028. But it does not change the underlying math. It lowers taxable income slightly, which may reduce or avoid taxes on a portion of benefits for some households.

How Does Social Security Affect Retirement Planning, Investments, and Contributions?

Social Security is the only piece of most retirement plans that is government-backed, inflation-adjusted, and lasts a lifetime. That makes it the foundation everything else is built on. The age you turn it on changes the shape of everything above it.

Savings drawdown. If you delay Social Security, you draw more from savings in the short term. But once the larger benefit starts, you draw less. Over 15 to 20 years after age 70, the lower withdrawal rate can extend how long your savings last. Research from Kitces and Pfau suggests that using savings to bridge the gap to a delayed claim can be one of the most effective strategies for extending portfolio longevity.

Portfolio allocation. The size of your Social Security benefit changes how much market risk your portfolio needs to carry. A larger benefit covers more of your fixed expenses, which means your portfolio can be more growth-oriented. A smaller benefit means the portfolio carries more weight, which may require a more conservative mix. Vanguard’s Advisor Alpha research suggests that coordinating income sources this way may add meaningful value over a full retirement.

The Roth conversion window. The years between retirement and age 73 are often your lowest-income years. If you delay Social Security, your taxable income during those years may be low enough to convert portions of a traditional 401(k) into a Roth IRA at the 12% or 22% bracket. Every dollar you convert is a dollar that does not become a Required Minimum Distribution at 73.

Smaller RMDs mean lower taxes, lower IRMAA, and more flexibility in your 70s and 80s. This window closes at 73 when RMDs begin. If you claim Social Security early, the added income fills up those lower brackets and the conversions happen at a higher rate, or not at all.

The One Big Beautiful Bill Act’s $6,000 senior deduction (65+, tax years 2025 through 2028) may create a few extra dollars of room for Roth conversions. For those in the right window, this makes the current opportunity slightly wider than usual.

Contributions before retirement. If you are still working in your late 50s or early 60s, you are in your peak earning years. The super catch-up contribution limit (for ages 60 through 63) allows up to $11,250 in additional 401(k) contributions in 2026. Every dollar you contribute now reduces your taxable income today and gives you more flexibility later.

Whether those dollars go to a traditional or Roth 401(k) depends on where you expect your tax rate to be in retirement, which depends in part on when you plan to claim Social Security. The decisions are connected.

How Does Social Security Claiming Age Affect Your Surviving Spouse?

This is the question that changes the conversation from money to people.

When one spouse dies, the surviving spouse keeps the larger of the two Social Security checks and loses the smaller one. If the higher earner claimed early, the survivor benefit is permanently capped at that reduced amount. For the rest of the surviving spouse’s life.

But the financial impact goes beyond the check. Three things change at the same time.

First, the survivor’s tax filing status changes from married filing jointly to single. The brackets for single filers are roughly half as wide. The survivor may pay a higher rate on similar income.

Second, the IRMAA threshold drops from $218,000 (joint) to $109,000 (single). Same income sources. Half the threshold. Medicare premiums may jump.

Third, expenses do not drop by half. The mortgage stays the same. Utilities, insurance, and property taxes stay the same.

Delaying the higher earner’s claim to 70 is one of the most effective forms of survivor protection available. It costs nothing except patience and a plan for the waiting years. Kitces and Pfau’s research on spousal coordination supports this approach for most married couples.

Wondering how your Social Security claiming age could affect your taxes, healthcare costs, and spousal benefits? There are at least eight financial consequences most families overlook. Schedule a conversation with our team to explore strategies tailored to your retirement picture.

The Question Worth Asking Out Loud

If you are married, ask this: if the higher earner dies first, what is the surviving spouse’s monthly income from all sources? Most couples have never asked this question. The answer often changes the claiming decision.

How Does Social Security Affect Your Total Retirement Income?

Social Security replaces less of your income than most people expect. The average benefit in 2026 is roughly $2,071 per month, according to the SSA. For someone who earned $150,000 or more, Social Security may replace only 30% to 35% of pre-retirement income. The other 65% to 70% has to come from savings, a pension, or other sources.

Your claiming age determines how much of that 65% your savings has to cover. A larger Social Security check means less reliance on the portfolio. A smaller check means more. Over 20 to 30 years, that difference changes how much you can spend, how much risk your investments need to take, and how long your money lasts.

The families who build the strongest retirement income plans are the ones who treat Social Security as the foundation and design the rest of the plan around it. Not the other way around.

What Is the Best Way to Optimize Social Security Income?

There is no single best age to claim. The right answer depends on your situation. But there is a best way to think about the decision.

Instead of asking “when should I start collecting?” ask “how does my claiming age affect everything else in my plan?” Then look at the full picture.

How does it affect my taxes? My Medicare costs? My health insurance before 65?

How fast I burn savings? What my spouse receives if I die first? Whether I have a window for Roth conversions?

The families who get this right do not pick the “optimal” age from a calculator. They look at how all six consequences interact for their specific household. And they make the decision before it becomes emotional.

If you can answer all six questions with confidence, you are ahead of most families. If even one is uncertain, that is worth a conversation before the decision becomes permanent.

What If I Am Still Working at 62?

If you claim Social Security before full retirement age and are still earning income, the earnings test applies. In 2026, Social Security withholds $1 for every $2 you earn above $24,480 (SSA). In the year you reach full retirement age, the limit rises to $65,160 and the rate drops to $1 for every $3.

The withheld money is not gone. Once you reach full retirement age, the SSA recalculates your benefit upward to account for the months when checks were withheld. But the process is confusing. For many working claimers, it may make more sense to simply wait.

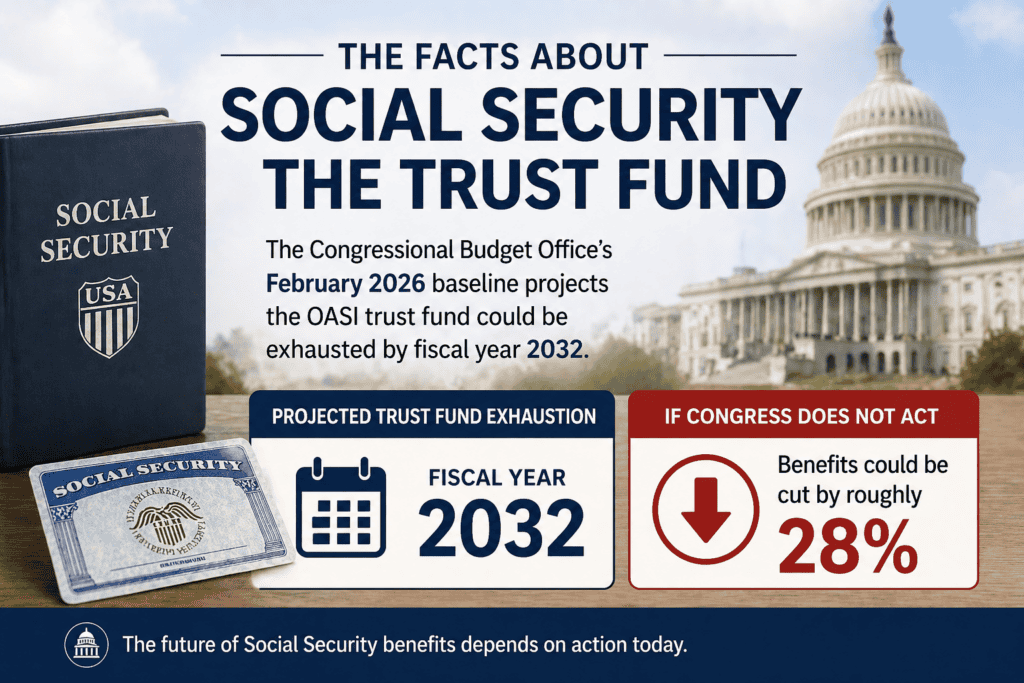

What If the Social Security Trust Fund Runs Out?

The Congressional Budget Office’s February 2026 baseline projects the OASI trust fund could be exhausted by fiscal year 2032. If Congress does not act, benefits could be cut by roughly 28%.

That concern is valid. But it rarely changes the best claiming age. A 28% cut applies equally to early and delayed benefits.

The delayed check still comes out ahead in most scenarios. The Bipartisan Policy Center and the National Academy of Social Insurance have both reached this conclusion.

Congress has faced this deadline before. In 1983, the trust fund was within months of exhaustion. Congress acted.

That does not mean the same thing will happen this time. But claiming early out of fear locks in a permanently smaller benefit based on a problem that may be solved before it arrives.

Can I Change My Mind After I Claim Social Security?

Yes, but only within a narrow window. If you claimed within the last 12 months, you can withdraw your application, repay everything you received, and restart later at a higher amount. After 12 months, that option closes permanently.

If you are past full retirement age and already collecting, you may be able to voluntarily suspend your benefit. Your benefit grows by 8% per year until you restart or turn 70. This does not work for everyone, but for some households it is worth exploring.

When Should I Take Social Security?

This is the question everyone asks first. But as you have seen, it is actually the last question you should answer. Because the answer depends on all of the above.

Claiming early may make sense if your health is uncertain, you need the income now, or you have no other assets to draw from. Delaying may make sense if you are healthy, have savings or a pension to bridge the gap, want to protect a surviving spouse, or want to keep the Roth conversion window open.

The right answer is not about picking the “perfect” age. It is about understanding how your claiming age connects to your taxes, your healthcare, your investments, your spouse, and your income for the next 20 to 30 years. Then making the call from clarity rather than pressure.

Worth Sharing

Most families think Social Security is one decision about one number. It is actually one decision that affects six parts of your financial life. If someone you know is approaching their claiming age, this article may help them see the full picture before the decision becomes permanent. Share this article or forward it to someone who could use it.

Ready to See How All Six Consequences Affect Your Plan?

We help families over 50 see how Social Security connects to their taxes, healthcare, investments, and spousal protection. No cost. No obligation. Just clarity.

Schedule a Complimentary Conversation

Or call 717-288-1880

This article is part of The Confident Retirement Brief, a weekly newsletter from Langan Financial Group. Subscribe here to receive clear thinking for confident financial decisions, delivered every Thursday.

Related: How to Figure Out When You Should Claim Social Security: A Step-by-Step Exercise

ABOUT THE FINANCIAL PLANNING AUTHOR

Alexander Langan, J.D., CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual and Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

ABOUT LANGAN FINANCIAL GROUP: FINANCIAL ADVISORS

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, PA.

With over 150 five-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

DISCLOSURE: This article is provided for informational and educational purposes only and does not constitute investment advice, financial planning advice, tax advice, or legal advice. All investing involves risk, including potential loss of principal. Past performance is not an indicator of future results.

Curious how a single claiming decision could ripple across your entire retirement plan? Download our Social Security Timing Guide to discover methods for evaluating your options across taxes, savings, and more. Then discuss your situation with an advisor when you’re ready.

Social Security benefit amounts referenced are based on Social Security Administration formulas and are subject to individual variation based on earnings history, work credits, and other factors. Maximum benefit amounts are for 2026 and are subject to annual change. The hypothetical scenario presented is for illustrative purposes only and does not represent any specific individual or predict any particular outcome.

Social Security trust fund projections are from the Congressional Budget Office February 2026 Baseline and are subject to revision. Congressional action could change benefit levels, tax treatment, or program structure at any time. The 8% delayed retirement credit is set by federal law and applies to benefits claimed after full retirement age up to age 70; it is not an investment return.

Social Security taxation thresholds ($25,000/$32,000 for 50% and $34,000/$44,000 for 85%) are set by federal statute and have not been adjusted for inflation since 1994. ACA marketplace subsidy eligibility is based on Modified Adjusted Gross Income relative to the Federal Poverty Level and is subject to change by Congress; the subsidy structure described reflects 2026 rules following the expiration of expanded subsidies. The $6,000 senior deduction is a provision of the One Big Beautiful Bill Act (2025) for taxpayers age 65 and older, tax years 2025 through 2028; phase-out thresholds apply; individual tax results vary.

The super catch-up contribution limit of $11,250 for ages 60 through 63 is for 2026 and is subject to annual adjustment. The Social Security earnings test limit of $24,480 and the FRA-year limit of $65,160 for 2026 are from the SSA. IRMAA thresholds and Medicare premiums are from the Centers for Medicare & Medicaid Services for 2026 and are subject to annual change.

Research referenced from Kitces and Pfau (retirement income planning), Vanguard Advisor Alpha, the Bipartisan Policy Center, the National Academy of Social Insurance, and JPMorgan Guide to Retirement is cited for educational purposes and does not predict specific outcomes. Life expectancy estimates are from SSA actuarial tables and reflect averages; individual longevity will vary. Roth conversion strategies involve tax consequences and should be evaluated with a qualified tax professional.

Please consult a qualified financial, tax, or legal professional before making any financial decisions.

Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.

Langan Financial Group | 1863 Center St. Camp Hill, PA 17011 | langanfinancialgroup.com/get-started-today

Copyright © 2026 Langan Financial Group. All rights reserved.