If you’re nearing retirement and just saw your portfolio drop by 30%, it’s hard not to feel a wave of anxiety.

You’ve spent decades building wealth—strategically investing, consistently saving, and working toward a retirement you could enjoy without worry. Now, the numbers look different. The plan feels uncertain. And the timing couldn’t feel worse.

But here’s the truth: What you do next matters far more than what just happened.

While it’s tempting to view this as a crisis, it’s really a critical moment for strategic recalibration—especially if you have $1 million or more in assets. You still have control. And with the right steps, you can protect your lifestyle, preserve your plan, and position yourself for long-term success.

Why Market Declines Near Retirement Aren’t a Death Sentence

This isn’t the first time markets have fallen sharply right as people were ready to step away from full-time work.

In 2008, just as millions of Baby Boomers approached retirement, the market crashed. According to the Employee Benefit Research Institute, the average American delayed retirement by about two and a half years. But notably, not everyone did.

Those who maintained their timelines typically had something in common: a clear, adaptable plan—and the composure to avoid reactive decisions.

That’s the key now. You don’t need to predict the market. You just need to make confident, data-informed decisions that reflect where you are today.

Step One: Understand Your Financial Starting Point

Before doing anything with your investments, you need clarity on the actual numbers. This step is often skipped, but it’s essential.

Start with your real monthly spending needs—not your ideal lifestyle, but your baseline necessities. Then identify what guaranteed income sources you already have in place. This includes Social Security, pensions, annuities, or rental income streams.

The gap between those two numbers is what your portfolio will need to cover, at least in the early years.

Let’s look at a simple example.

Tom is 61 and needs $7,000 per month in retirement. His Social Security benefit will provide $2,800. That leaves a $4,200 monthly gap—or just over $50,000 per year. If his portfolio has dropped from $1 million to $700,000, that withdrawal rate would be 7.2%.

That’s above the preferred 4% target, but it’s not catastrophic. And with a few smart adjustments, it can be brought back into alignment.

Map Out What Recovery Could Look Like

Rather than reacting to the current market, it’s more helpful to visualize how your retirement plan might perform under different future scenarios.

Consider modeling three timelines:

- A best-case scenario where the market recovers half of its losses in 12–18 months

- A moderate scenario where recovery takes 2–3 years

- A worst-case scenario where full recovery takes five or more years

Within each, evaluate what adjustments might be needed. Could you delay full retirement by a year or two? Could you work part-time for a while? Would small lifestyle shifts in the first few years give your portfolio time to recover?

This exercise turns fear into planning. It gives you options and helps you regain a sense of agency over your retirement path.

How Steady Savers Can Build a Retirement Bridge

If you’ve built your retirement plan around a more traditional structure—W-2 income, 401(k) or IRA savings, and a goal of maintaining your lifestyle—you’re what we’d call a “Steady Saver.”

Your best move right now is likely not to overhaul your plan, but to build a bridge that gets you through the recovery period without locking in losses by withdrawing too early.

One effective approach is the 3-2-1 framework:

- 3 years of basic expenses in cash, CDs, or short-term bonds

- 2 years of letting your portfolio rebound before taking larger withdrawals

- 1 extra year of part-time work to rebuild your cash buffer

You might also consider delaying Social Security. Every year you wait past age 62 increases your benefit by 6–8%. That’s a guaranteed return, something even the market can’t promise.

If part-time work is an option, even modest income—$20,000–$30,000 per year—can dramatically reduce the strain on your portfolio.

How Wealth Accumulators Can Use This as an Opportunity

For those with more complex portfolios—real estate, taxable brokerage accounts, business equity, or multiple income streams—this moment is less about defense and more about strategic positioning.

Many high-net-worth investors fall into what we call the “Wealth Accumulator” group. You’ve built a flexible financial base that supports a wide range of options. A market downturn, while frustrating, is often the buying opportunity you’ve been waiting for.

One smart approach is the barbell strategy:

Keep half your portfolio in ultra-safe assets—Treasury bonds, high-grade municipal bonds, or high-yield savings—and use the other half for carefully selected recovery plays like discounted blue-chip stocks, real estate, or private credit.

Tax-loss harvesting is another powerful tool. Realizing losses now lets you:

- Offset ordinary income (up to $3,000 per year)

- Offset capital gains this year and in future years

- Rebalance into higher-quality holdings without triggering a tax bill

This is especially useful if you’re already planning to rebalance or reduce risk. Don’t miss the chance to reset your cost basis while markets are low.

And if income is down temporarily (say you’re semi-retired), consider whether a Roth conversion might make sense while tax rates are favorable and values are temporarily suppressed.

High-Net-Worth Planning Opportunities Often Overlooked

It’s not just about your income today. A market correction is an opportunity to revisit your entire financial framework.

- Estate Planning: Are your trusts, wills, and gifting strategies aligned with new valuations? Lower asset values may open doors for more tax-efficient gifting or wealth transfer.

- Philanthropy: Do donor-advised funds (DAFs) or charitable trusts need to be adjusted? If you had planned to give, it might be worth waiting—or rebalancing how you give.

- Coordinated Advice: Are your CPA, estate attorney, and financial planner aligned on your next moves? Now is the time for coordination, not isolated advice.

High-net-worth individuals typically have the pieces — but this moment requires a thoughtful reassembly of the puzzle.

Avoiding the Three Behavioral Traps

Even seasoned investors can fall victim to cognitive biases in times like these. Be aware of:

- Recency bias: Assuming today’s losses will continue indefinitely

- Loss aversion: Focusing more on losses than the long-term value you’ve built

- Sunk cost fallacy: Holding onto poor investments to “get back to even”

The antidote is simple but not easy: Think like a business owner, not a gambler. Evaluate your financial position as a whole. Make strategic adjustments. Don’t let short-term emotions dictate long-term outcomes.

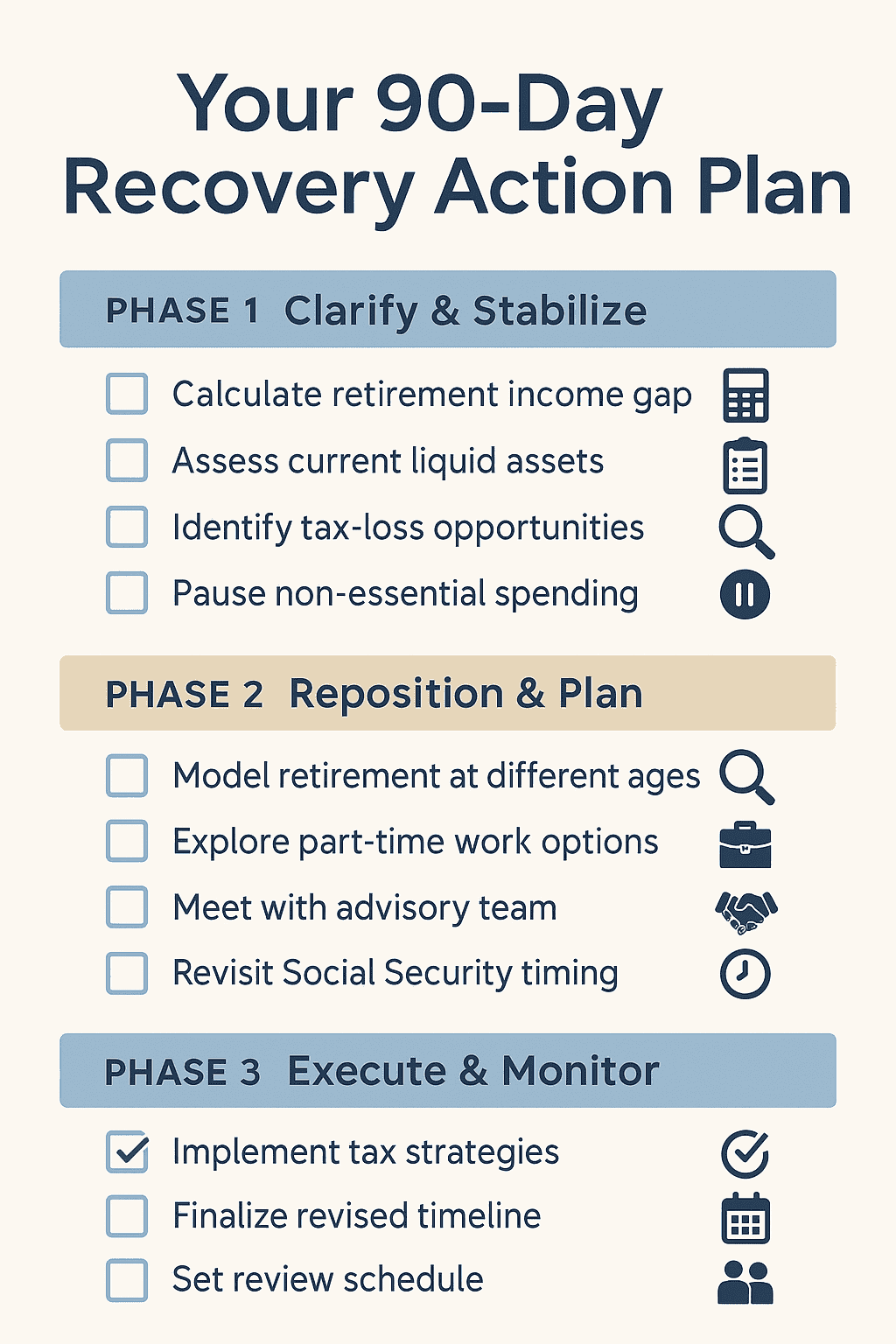

Your 90-Day Retirement Recovery Plan

It’s not about reacting overnight. It’s about creating a sequence of smart, intentional moves:

Days 1–30: Clarify and Stabilize

- Calculate your retirement income need and compare it to guaranteed income sources

- Pause non-essential spending and build liquidity if needed

- Identify tax-loss harvesting opportunities and potential Roth conversion windows

Days 31–60: Reposition and Plan

- Explore part-time work or consulting as a lifestyle and financial buffer

- Revisit Social Security timing

- Meet with your advisory team to model retirement at multiple ages

Days 61–90: Execute and Monitor

- Begin rebalancing and tax strategy implementation

- Finalize a revised retirement timeline and communicate with your spouse/family

- Set a monitoring cadence and accountability check-ins for your plan

This is your playbook—not for panic, but for progress.

Final Thought: You’re Still in Control

A 30% drop in your portfolio is significant, no question. But for most high-net-worth individuals nearing retirement, it doesn’t mean the plan is off track—it just means it’s time for an updated map.

Market volatility is part of the journey. What defines a successful retirement isn’t avoiding downturns, but having a resilient strategy that can adapt when they arrive.

You’ve worked too hard to let one market cycle rewrite your entire future. With the right plan, the next chapter can still unfold on your terms.

Want help reviewing your current plan or revisiting your withdrawal strategy? Talk with your advisor or schedule a consultation with a fiduciary planner who understands the nuances of retirement transitions.

Sources

- Employee Benefit Research Institute, 2024

- Federal Reserve Bank of St. Louis, 2024

- Vanguard, “Market Volatility and Retirement Planning,” 2024

- Social Security Administration, “Delayed Retirement Credits,” 2024

- Morningstar, “Tax-Loss Harvesting for Retirees,” 2024

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.