Cash feels safe. You can see it. You don’t have to worry about stock prices. But too much cash—or too little—can hurt your long-term retirement goals. Let’s walk through how cash fits into your plan, how it changes with life stage, and how to figure out the right balance.

Why Many Retirees Hold Too Much (or Too Little)

Surveys show retirees often keep 20–30% of their portfolios in cash or cash equivalents (money market funds, CDs, etc.). Fear of market drops makes cash appealing, but it comes at a cost: inflation erodes buying power.

Not holding enough cash can be equally risky — you may be forced to sell investments in a downturn to cover expenses, locking in losses.

The Current Rate Environment (2025)

- Savings accounts, money market funds, and CDs are paying 4–5%, a major shift compared to under 1% through most of the 2010s.

- Higher yields make holding some cash more rewarding, but cash still won’t outpace stocks and bonds over decades.

How Cash Fits in a Portfolio

Cash plays three roles:

- Liquidity & flexibility: Covers daily needs and emergencies.

- Buffer in downturns: Protects against selling at the wrong time.

- Peace of mind: Helps you stick with your long-term plan without panic.

But remember: at 3% inflation, $100,000 in cash today will only buy about $74,000 worth of goods in 10 years.

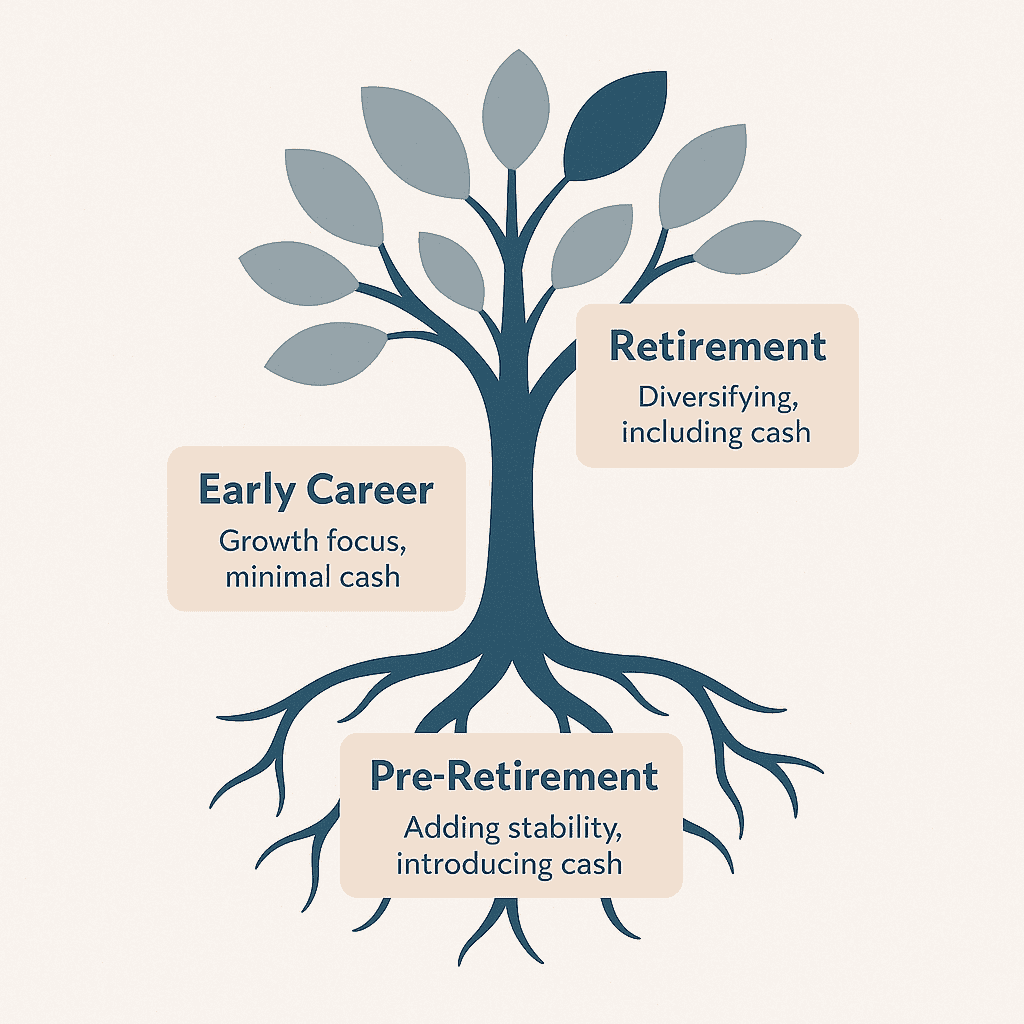

How Cash Needs Change With Life Stage

| Stage of Life | Typical Role of Cash | Example Range |

| Wealth Building (20s–40s) | Keep 3–6 months of expenses in cash. The rest should focus on growth. | 5–10% |

| Pre-Retirement (50s–early 60s) | Build a larger buffer (6–12 months of expenses) to reduce risk. | 10–15% |

| Retirement (65+) | Hold 12–24 months of expenses as a cushion. Protects against selling during downturns. | 15–25% |

These are guidelines — the right number depends on your income sources, spending, and comfort level.

How to Determine the Right Balance for You

Here are practical steps:

- Start with monthly expenses. Multiply your average expenses by 12–24 months to find your cash “comfort zone.”

- Example: If you spend $6,000/month, holding $72,000–$144,000 in cash might make sense.

- Factor in steady income. If you have a pension or rental income covering $3,000/month, you may only need to cover the gap with cash.

- Think about your risk tolerance. Some people sleep better with two years of expenses in cash. Others feel fine with less if they have strong investments.

- Check tax efficiency. Use high-yield savings, money markets, or short-term Treasuries for your cash to reduce opportunity cost.

Using Cash as a Buffer in Market Downturns

A well-known risk is sequence-of-returns risk — when you hit a downturn early in retirement and need to withdraw.

Example:

- A retiree with 18 months of cash avoids selling in a downturn, allowing stocks time to recover.

- Vanguard and Morningstar studies show this “bucket strategy” reduces volatility and the chance of running out of money too soon.

Often Overlooked Considerations

- Taxes on cash yield: Interest is taxed as ordinary income. Placing cash in tax-advantaged accounts (like part of your IRA) or using municipal bonds can sometimes improve efficiency.

- Liquidity vs. opportunity: Too much cash may feel safe, but missing out on market rebounds is one of the biggest risks.

- Behavioral bias: People tend to hoard cash after crises (like 2008 or 2020). But history shows markets recover, and sitting on the sidelines too long is costly.

- Emergency overlap: Retirees often double-count emergency funds and cash buckets. You may not need both at full size.

- Health care and long-term care: Some retirees underestimate how much cash they’ll need for sudden health costs before insurance or Medicare pays.

How Do I Manage My Portfolio Cash?

Cash isn’t the star of your portfolio, but it’s a critical supporting player. The right amount depends on your stage of life, steady income sources, and comfort level. Too much cash risks lost growth, too little risks stress and forced selling.

A balanced approach — tailored to you — helps you ride out downturns, cover surprises, and sleep better at night.

Comment Portfolio Cash in the form and we’ll send you our checklist to help you think through your portfolio cash allocation.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.