You’ve likely heard that diversification is key to investing, but how you actually allocate your assets—meaning how much of your portfolio is in stocks, bonds, and cash—can have a greater impact on your financial future than any single investment you choose.

For retirees or those nearing retirement, asset allocation isn’t just a technical term—it’s one of the most important decisions that can affect how long your money lasts, how much you pay in taxes, and how you weather market volatility.

Let’s break it down.

What Is Asset Allocation?

Asset allocation is the strategy of dividing your investments into different asset categories—typically stocks (equities), bonds (fixed income), and cash equivalents—based on your risk tolerance, time horizon, income needs, and financial goals.

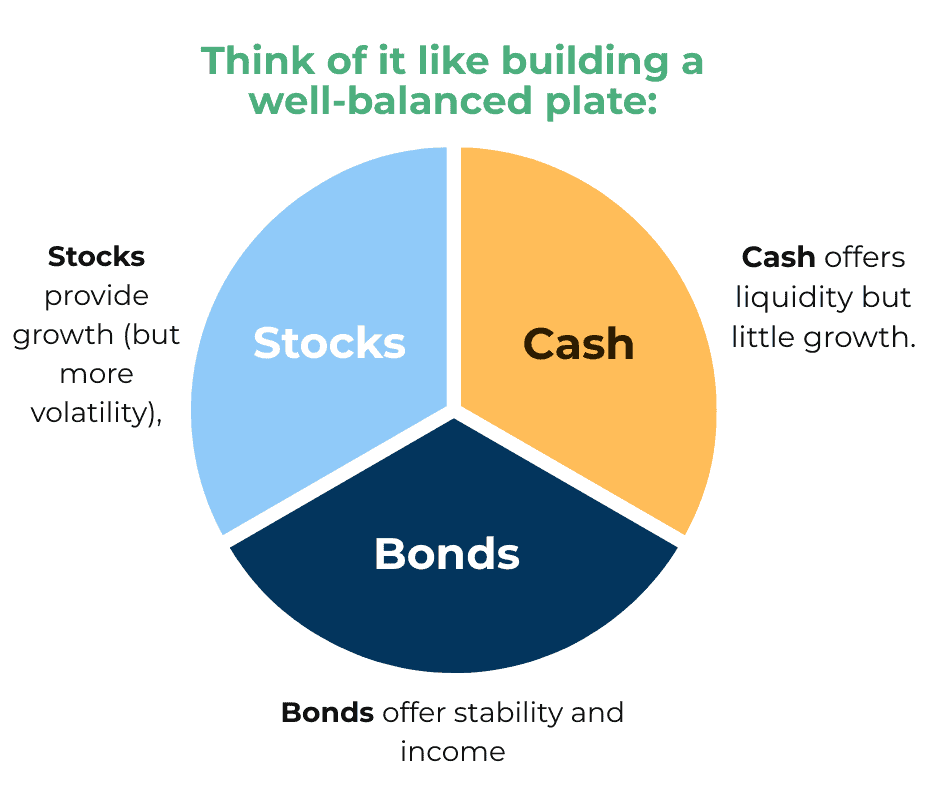

Think of it like building a well-balanced plate:

- Stocks provide growth (but more volatility),

- Bonds offer stability and income,

- Cash offers liquidity but little growth.

The right mix changes as you get older, especially as you enter and move through retirement.

Why Asset Allocation Is So Important In Retirement

When you’re working, your paycheck covers expenses and your portfolio can ride out market swings. In retirement, your investments need to fund your lifestyle—every year, through every market cycle.

That’s why your asset allocation plays a critical role in:

- How much risk you’re exposed to

- How much income you can safely withdraw

- How your money grows over time

- How your taxes stack up year to year

In fact, studies have shown that asset allocation accounts for over 90% of a portfolio’s performance over time—not which stocks or funds you pick.

Common Asset Allocations—and Why They’re Not One-Size-Fits-All

Let’s look at how different portfolios might perform over a 25-year retirement:

| Portfolio | Stock % | Bond % | Cash % | Estimated 25-Year Value* |

| Aggressive | 80% | 15% | 5% | $3.4 million |

| Balanced | 60% | 30% | 10% | $2.5 million |

| Conservative | 30% | 60% | 10% | $1.7 million |

*Based on assumed annual returns of 6.5% for stocks, 3.5% for bonds, and 1% for cash.

At first glance, aggressive investing looks like a no-brainer—higher returns, right? But it’s not that simple.

Why It’s Not Just About Chasing the Highest Return

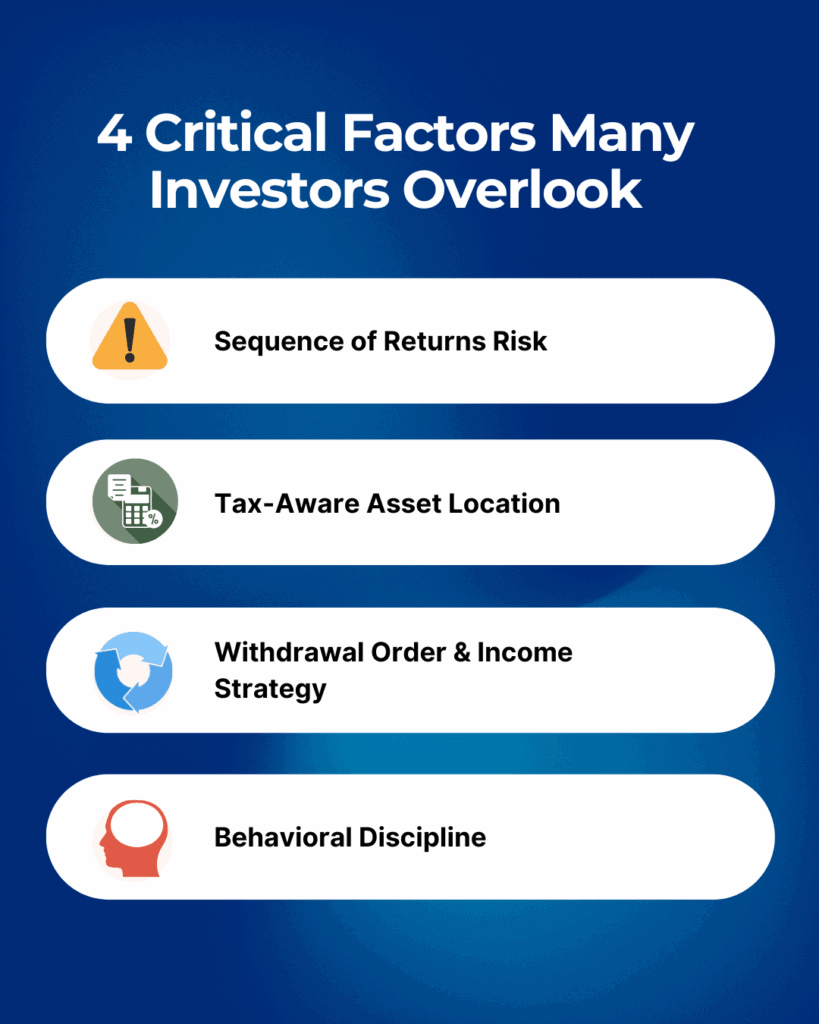

Retirement allocation isn’t about maximizing gains—it’s about balancing growth, income, taxes, and emotional comfort. Here are four critical factors many investors overlook:

1. Sequence of Returns Risk

The order of returns matters. If you withdraw money during a market downturn early in retirement, you may permanently erode your portfolio—even if average returns are strong.

Solution: Consider a “bucket strategy” that segments money by time horizon so you’re not forced to sell growth assets during down markets.

2. Tax-Aware Asset Location

It’s not just what you own, but where you own it. Placing high-tax investments in IRAs and tax-efficient assets in brokerage accounts can reduce your annual tax bill and stretch portfolio longevity.

Tip: Coordinate your allocation across accounts (taxable, tax-deferred, Roth) for maximum efficiency.

3. Withdrawal Order & Income Strategy

The order you tap your accounts—IRA, Roth, taxable—can significantly impact your tax liability and Medicare premiums.

Stat: Morningstar research shows that strategic withdrawal planning can extend portfolio life by 2–3 years.

4. Behavioral Discipline

Even the “perfect” portfolio fails if you abandon it in a downturn. The more volatile the allocation, the harder it may be to stick with during tough times.

Planning focus: Your allocation must align with your emotional risk tolerance—not just your spreadsheet.

Other Factors That Influence Your Allocation

To truly get this right, a retirement asset allocation strategy should account for:

- Longevity expectations: Living into your 90s requires more growth.

- Guaranteed income sources: Pensions or annuities reduce pressure on your portfolio.

- Spousal needs: Different ages, health, or income history may shift the allocation.

- Healthcare & long-term care needs: Unexpected costs can erode conservative portfolios.

- Legacy or charitable goals: You may need to allocate more to growth for multigenerational planning.

Putting It All Together

The best allocation is the one that:

- Provides enough growth to outpace inflation

- Generates reliable income without depleting principal

- Minimizes tax drag and surprises

- Lets you sleep at night—even during volatility

And most importantly—it evolves with you.

This isn’t something to “set and forget.” It should be revisited regularly based on changes in the market, your health, your income needs, and tax laws.

Asset allocation is the engine of your retirement plan. It’s not just about growing money—it’s about using it wisely, preserving it strategically, and aligning it with what matters most in your life.

If you haven’t reviewed your allocation in the past year—or you’re unsure how taxes, volatility, or the 2026 tax law changes may affect your plan—this is the perfect time to take a closer look.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.