When most people think about taxes, they think about April.

Smart planning looks much further ahead.

Because the truth is, you don’t retire on balances. You retire on after-tax income — what actually shows up in your bank account each month after the IRS takes its share.

And the way you save, invest, and structure your taxes in 2026 can quietly determine how much of your future income you get to keep for the rest of your life.

Let’s talk about what’s changing, why it matters to you, and how you can use the rules — not fight them — to build more income with less tax.

Why 2026 Is a Meaningful Planning Year

In 2026, the IRS has already raised several savings limits, and the tax landscape continues to evolve. What hasn’t changed is this:

The people who plan their taxes on purpose keep more of their money.

The people who don’t… fund the government’s retirement instead of their own.

Higher contribution limits and expanded catch-up rules mean you now have more room to:

• Lower your taxable income

• Keep more money compounding

• Shape your future tax brackets

• Build income you control later

The cost of ignoring strategy is rising.

And the reward for getting it right is growing.

How Saving More Can Actually Cost You Less

Here’s a simple idea that changes everything:

Every dollar you put into a traditional retirement account doesn’t really cost you a full dollar.

As a simple example, if you’re in roughly a 28% combined marginal tax bracket and you contribute $10,000 to your 401(k), your take-home pay might only drop by about $7,200. The IRS effectively “pays” the other $2,800 by not taxing it.

You’re not just saving.

You’re buying future income at a discount.

That’s why contribution limits matter so much.

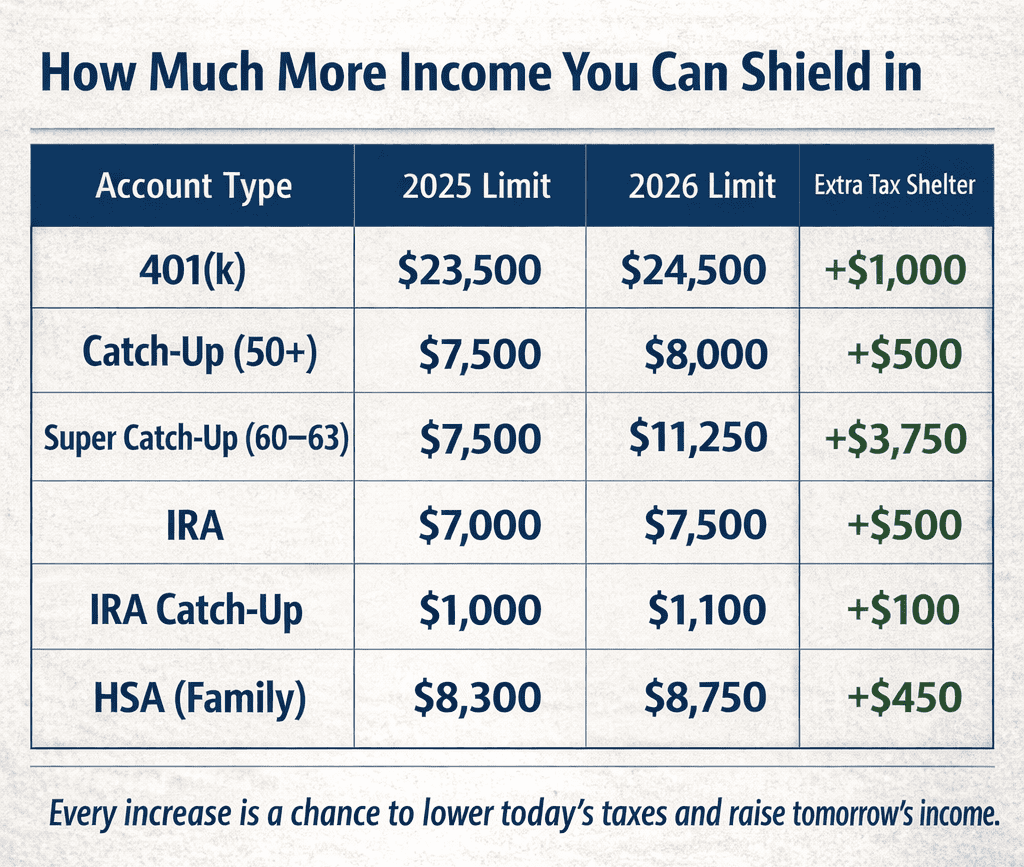

What You Can Contribute in 2026

Your 401(k) or Employer Plan

For 2026, you can contribute up to $24,500.

If you’re 50 or older, you can add another $8,000 in catch-up contributions.

And if you’re between 60 and 63, the rules allow an even larger “super catch-up” of $11,250, bringing your total as high as $35,750, if your plan supports it.

Every dollar you contribute to a traditional 401(k):

• Reduces your taxable income

• May keep you in a lower tax bracket

• Grows without annual tax drag

• Becomes future income you control

This is one of the most powerful ways to turn today’s tax savings into tomorrow’s retirement paycheck.

IRAs: Building Flexibility

For 2026, you can contribute $7,500 to an IRA.

If you’re 50 or older, you can add a $1,100 catch-up, for a total of $8,600.

A traditional IRA may lower your taxes now.

A Roth IRA can create tax-free income later.

Which one is right depends on your income, your tax bracket, and whether you’re covered by a workplace retirement plan. Often, having both gives you the most control in retirement — letting you decide where your income comes from and how much tax you pay on it.

HSAs: The Hidden Retirement Income Tool

If you have a high-deductible health plan, an HSA may be one of the most valuable accounts you own.

For 2026, you can contribute:

• $4,400 for individual coverage

• $8,750 for family coverage

• Plus a $1,000 catch-up if you’re 55 or older and not enrolled in Medicare

HSAs are unique because they offer:

• A tax deduction when you contribute

• Tax-free growth

• Tax-free withdrawals for medical expenses

Since healthcare is one of the largest costs in retirement, an HSA can become a powerful source of tax-free retirement income when used long-term.

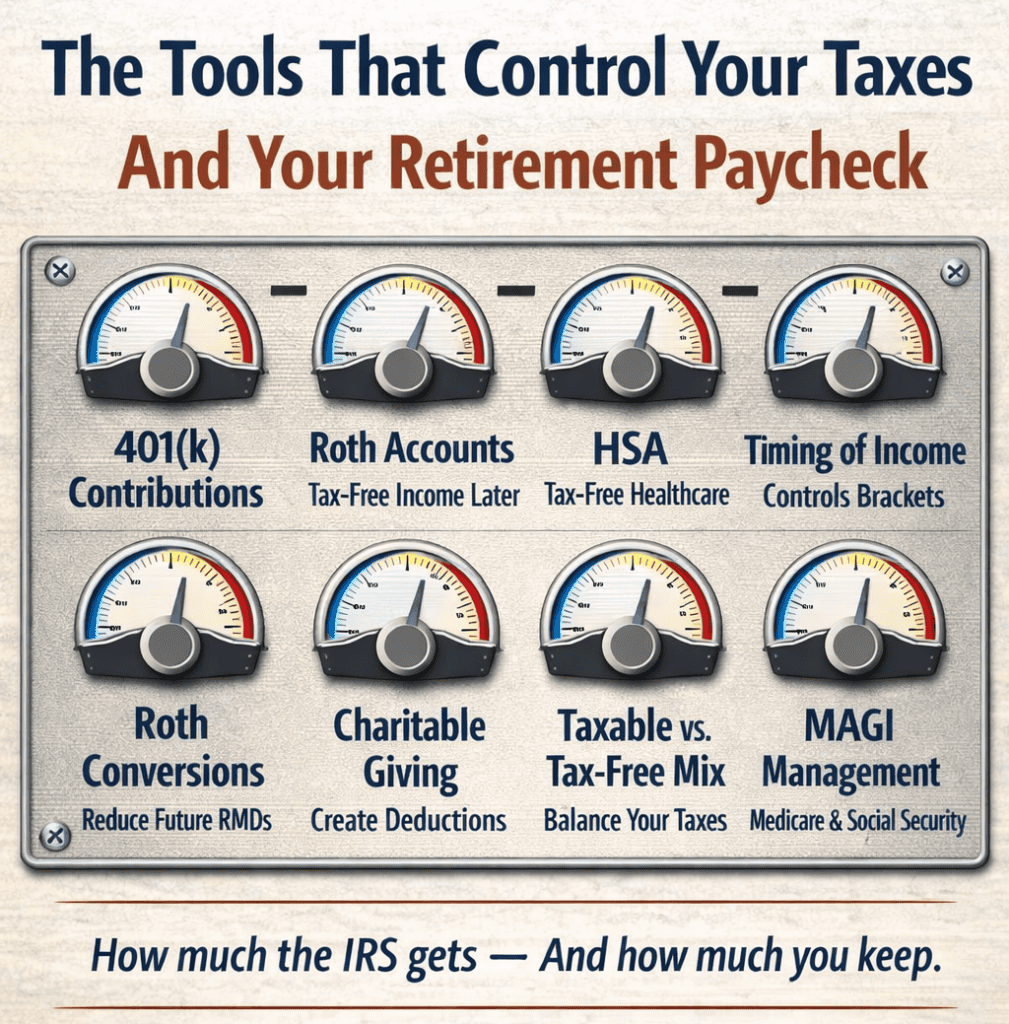

Why This Matters for Your Retirement Income

All of this connects to one simple question:

“How much income will I be able to spend every year, after taxes, for the rest of my life?”

The answer depends on where your money sits.

Some will be taxable.

Some will be tax-deferred.

Some can be tax-free.

When all your money is in one bucket, the IRS has most of the control.

When it’s spread across all three, you have the control.

That control helps you:

• Stay in lower tax brackets

• Reduce required minimum distributions

• Limit how much of your Social Security is taxed

• Avoid unnecessary Medicare premium surcharges

• Create smoother, more predictable income

This is how tax planning becomes income planning.

How Your Age Changes the Strategy

If you’re in your 40s or early 50s, your focus is on building and sheltering as much as you can while income is high and time is on your side.

If you’re in your late 50s or early 60s, catch-up years become a powerful window. You can reduce future taxes and shape how your retirement income will be taxed before required distributions begin.

If you’re approaching retirement, the conversation shifts to timing — when to take income, when Roth conversions may make sense, and how to keep taxes from quietly eating into your lifestyle.

And once required distributions start, the order you take money can matter just as much as how it’s invested.

Different stage. Same goal:

More income you keep. Less income lost to taxes.

A Simple Priority Most People Miss

If you’re wondering where to focus first, a common order that often makes sense is:

- Contribute enough to your 401(k) to get the full employer match.

- Max out your HSA if you’re eligible.

- Fund an IRA (traditional or Roth, depending on your situation).

- Then go back and increase your 401(k) contributions toward the limit.

This helps you capture free money, lower taxes, and build future income at the same time.

Bringing It All Together

Tax planning isn’t about chasing loopholes.

It’s about building a system that works year after year.

A system that:

• Lowers your taxes while you’re working

• Builds multiple sources of retirement income

• Gives you control over when and how you’re taxed

• Protects your cash flow from unnecessary erosion

When done well, it doesn’t just improve your tax return.

It improves your lifestyle.

The real question isn’t, “How big did my account grow?”

It’s:

“How much can I safely spend… and how long will it last… after taxes?”

That’s the heart of a strong 2026 tax strategy — and the foundation of a confident retirement.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

Fields marked with an * are required