A practical guide for pre-retirees who want their plan to hold up — no matter what the economy does next.

Most people start thinking about retirement with a simple, logical idea: save consistently, let your money grow, and eventually you’ll have enough. It makes sense on paper. But the real path to retirement almost never follows that straight line.

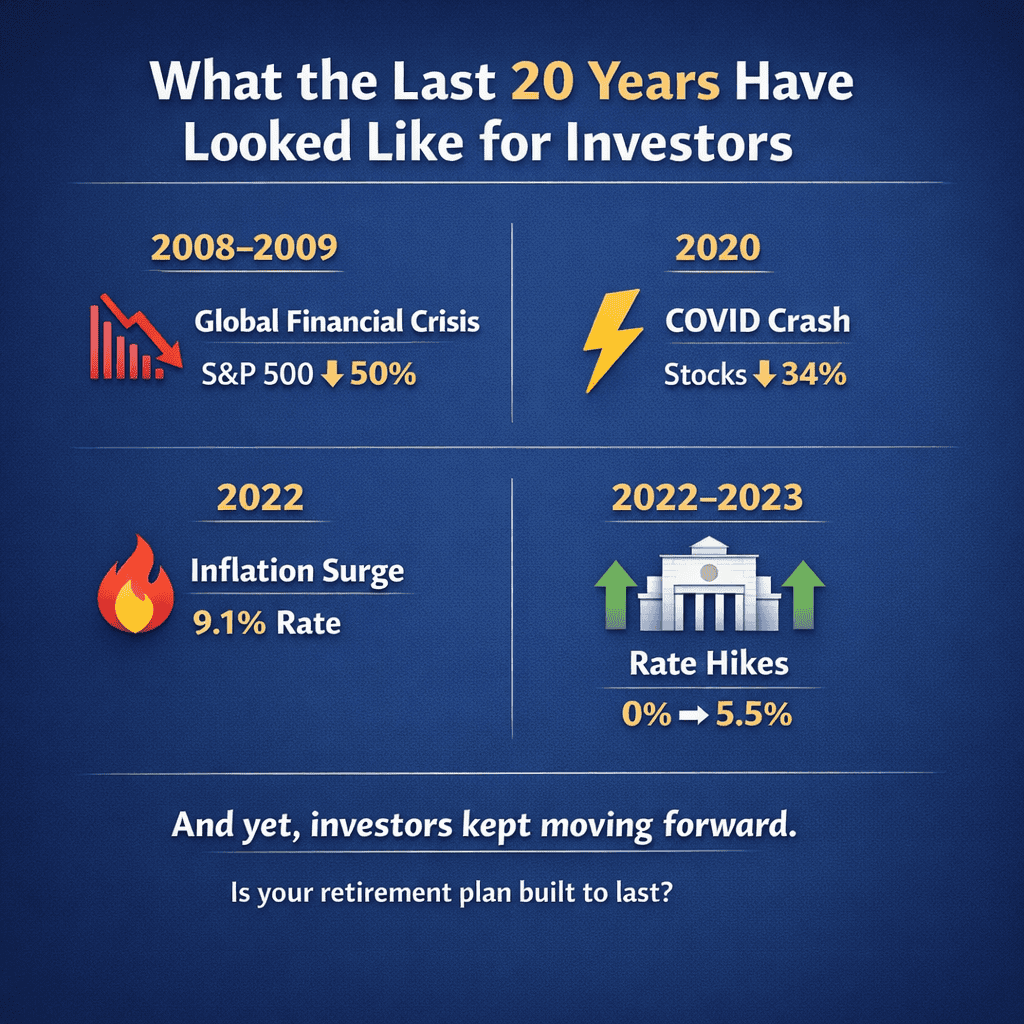

If you’ve been saving and investing for the past 20 years, think about what you’ve lived through as an investor:

- The 2008 financial crisis — the S&P 500 lost roughly 50% of its value between October 2007 and March 2009

- The brief but sharp COVID-19 market crash — stocks fell about 34% in roughly five weeks in early 2020

- Inflation reaching 9.1% in June 2022 — the highest rate since 1981, according to the U.S. Bureau of Labor Statistics

- The Federal Reserve raising interest rates 11 times in about 16 months — from near zero to 5.25–5.50% between March 2022 and July 2023

Each of those events surprised most forecasters. Each one changed the math for people who were planning their retirement at the time.

The lesson isn’t that the future is impossible to navigate. The lesson is that economic surprises are a normal part of long-term investing — not exceptions to it. And the retirement plans that tend to hold up best are the ones built with that reality in mind from the start.

| The Core Idea You don’t need to predict the next economic event. You need a plan that doesn’t require you to get it right. |

Why the 10 Years Before Retirement Are the Most Critical

Economic changes affect investors at every stage of life. But for people in their 50s and early 60s, the stakes are different.

When you’re in your 30s and markets drop, time is on your side. You have decades to wait for a recovery. You can keep contributing, stay invested, and likely come out ahead.

When you’re 5–10 years away from retirement, that cushion shrinks. This is when financial planners talk about sequence of returns risk, and it’s one of the most important ideas most people have never heard of.

What Is Sequence of Returns Risk?

Here’s the basic idea: it’s not just how much your investments grow over time that matters; it’s also when the good years and bad years happen.

Imagine two people retire at the same time with the same account balance. They earn the same average return over 20 years. But one experiences bad years early in retirement and the other experiences bad years later. The person who faces poor returns early can run out of money significantly faster, even if the math looks identical on paper.

This risk is especially real during the five years before and after retirement, sometimes called the “retirement red zone.” A major market decline in this window can do lasting damage to a retirement plan in ways that an identical decline at age 40 simply wouldn’t.

| A Straight forward Example Suppose you retire with $500,000 and plan to withdraw $25,000 per year. If markets drop 30% in your first two years of retirement, you’re selling shares at lower prices to cover those withdrawals — shares that won’t be available to participate in the eventual recovery. That’s sequence of returns risk in action. |

This is why the planning decisions you make in the years leading up to retirement often matter just as much as (sometimes more than) the investment decisions you’ve made over your entire career.

The Right Question to Ask About Your Plan

Many people measure their retirement readiness by a single number: their account balance. There’s nothing wrong with tracking your savings, but it’s only part of the picture.

A more useful question to ask yourself right now is: “If the economy changed significantly tomorrow, would my retirement plan still work?”

This isn’t meant to cause worry. It’s a practical stress test. Here are a few scenarios worth thinking through:

- What if markets declined 20–30% in the two years before your planned retirement date?

- What if inflation stayed elevated for several more years, increasing your cost of living?

- What if you needed to retire one or two years earlier than planned due to a job change or health issue?

- What if interest rates shifted significantly, affecting the income you expected from bonds or savings accounts?

A flexible plan is one that has thought through these scenarios in advance and has built-in adjustments rather than built-in assumptions. That kind of flexibility doesn’t happen automatically. It comes from deliberate planning.

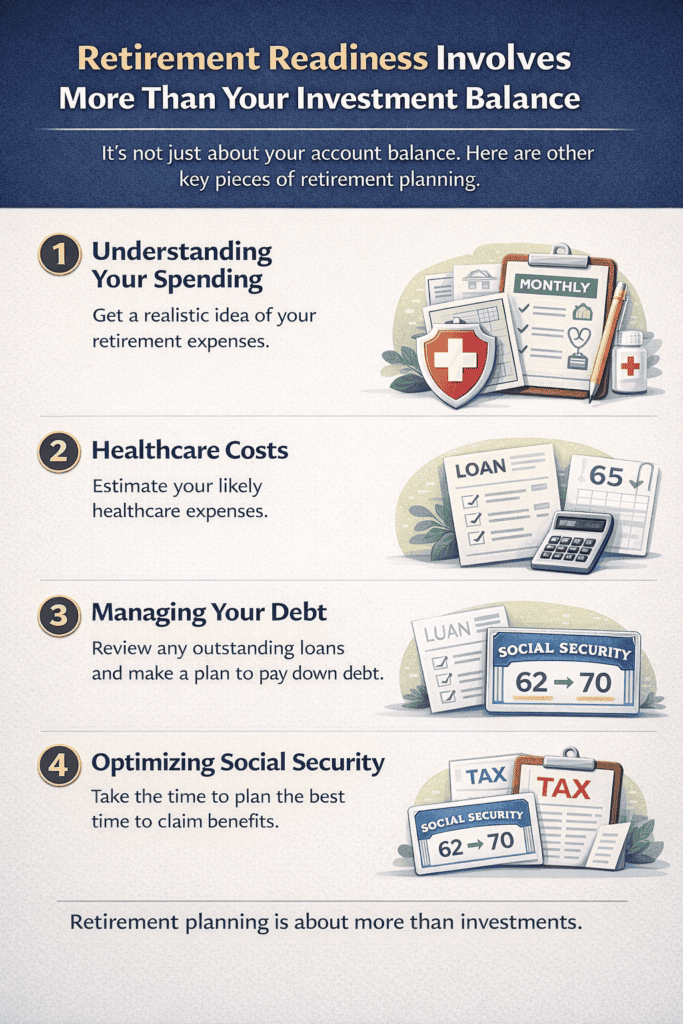

Retirement Readiness Involves More Than Your Investment Balance

One of the most common misconceptions about retirement planning is that it’s primarily an investment problem. It’s not. Your account balance is important, but it’s only one of several pieces that need to work together.

1. Understanding Your Actual Spending in Retirement

Many pre-retirees underestimate how much they’ll spend. Research consistently shows that spending doesn’t necessarily drop as dramatically as expected in early retirement, especially in the first decade, when many people are healthy and active.

Key spending areas to think about include housing, travel and leisure, healthcare, helping adult children or grandchildren, and taxes on retirement account withdrawals. Getting an honest picture of your likely expenses is foundational to every other planning decision.

2. Healthcare: The Expense Most People Underestimate

Healthcare is consistently one of the most underestimated retirement costs. Fidelity Investments’ 2023 Retiree Health Care Cost Estimate projected that a single person retiring at 65 may need approximately $157,500 — and a couple roughly $315,000 — to cover healthcare expenses throughout retirement. These are estimates, and your actual costs may be higher or lower depending on your health, the coverage you choose, and how long you live.

If you plan to retire before age 65, you also need to plan for the cost of health insurance coverage before Medicare kicks in. That gap can be a significant budget line item.

3. Debt Going Into Retirement

Carrying significant debt into retirement, including a mortgage, isn’t automatically disqualifying. But it does increase the amount of monthly income you need to draw from your savings, which increases withdrawal pressure and sequence of returns risk.

Many financial advisors suggest that pre-retirees take a close look at their debt load in the final decade before retirement and consider whether reducing it makes sense as part of their overall strategy.

4. Social Security: Timing Matters More Than Most People Realize

You can claim Social Security as early as age 62 or as late as age 70. The difference is meaningful: each year you delay past your full retirement age, your benefit increases by approximately 8% — up to age 70. Claiming at 62 versus 70 can result in monthly benefits that differ by 70–76% or more.

There’s no universally “correct” time to claim. The right decision depends on your health, your other income sources, your spouse’s situation, and your overall plan. But it’s a decision worth analyzing carefully — not making by default.

5. Tax Planning Around Your Retirement Accounts

Most traditional 401(k) and IRA withdrawals are taxed as ordinary income. Depending on how much you withdraw each year, your tax bill in retirement can be substantial. Required Minimum Distributions (RMDs) — which generally begin at age 73 under current law — can push some retirees into higher tax brackets.

Understanding the tax character of your retirement assets, and thinking about Roth conversions, withdrawal sequencing, and other strategies, can meaningfully affect how long your money lasts. This is an area where coordination between your financial plan and tax planning pays off.

| A Note on Life Expectancy According to the Social Security Administration, the average 65-year-old man today can expect to live to about age 84. The average 65-year-old woman can expect to live to about age 87. Many people live significantly longer. This is a reason to plan for a retirement that may last 25–30 years or more — not 10 to 15. |

Why Trying to Predict the Economy Usually Doesn’t Help

Every year, financial firms, economists, and media outlets publish forecasts for markets, interest rates, and inflation. And every year, those forecasts are frequently wrong in meaningful ways.

This isn’t a criticism of economists; the economy is genuinely complex. It’s simply a reminder that building a retirement plan around a specific economic prediction is risky, because the prediction may not come true.

A more practical approach is to focus on what you can control and build flexibility into what you can’t:

- Control your savings rate and spending habits

- Control when and how you claim Social Security

- Control your asset allocation relative to your timeline

- Control your debt load and cost of living

- Build flexibility around market conditions, inflation, and retirement timing

Plans that account for a range of possible outcomes, rather than assuming one specific path, tend to be more durable. This doesn’t mean being overly conservative or never taking investment risk. It means building a plan that can be adjusted without being abandoned.

A frequently cited framework for retirement withdrawals is the “4% guideline,” based on research by financial planner William Bengen in 1994. It suggests that withdrawing about 4% of your portfolio in the first year of retirement, then adjusting for inflation, has historically allowed portfolios to last 30 years in most scenarios. However, this is a general starting framework, not a guarantee. Your specific situation may support a higher or lower withdrawal rate depending on your other income sources, expenses, and timeline.

Common Questions Pre-Retirees Ask

“How do I know if I’m on track?”

There’s no single benchmark that applies to everyone. Common rules of thumb, such as having 10 to 12 times your annual salary saved by age 65, can provide a rough reference point, but they don’t account for your specific spending plans, Social Security benefit, healthcare needs, or other income sources. A personalized analysis of your situation will always be more useful than a generic target.

“What if I retire and the market drops right away?”

This is one of the most common worries for people approaching retirement and it’s a legitimate one. A few strategies can help reduce this risk: keeping 1–2 years of planned withdrawals in cash or short-term, lower-volatility assets; having a flexible withdrawal approach that allows you to temporarily pull back if markets are down significantly; and making sure your overall asset allocation reflects your actual timeline and income needs, not just your risk tolerance from a decade ago.

“How much income will I actually need?”

A traditional starting point is 70–80% of your pre-retirement income. But this varies widely. People with paid-off homes and modest travel plans may need less. People who plan to travel extensively, help family members financially, or who have significant healthcare costs may need more. The most accurate answer comes from building out a detailed picture of your expected spending, not using a percentage estimate.

“When should I start reviewing my plan more seriously?”

For most people, the five to ten years before their target retirement date is the right window to be doing more detailed, personalized planning. This is when the assumptions in your plan deserve a closer look:

- Spending projections

- Social Security timing

- Healthcare coverage

- Investment allocation

and when small adjustments can still have meaningful impact.

“Do I need a financial advisor?”

That depends on the complexity of your situation. Some people are comfortable handling retirement planning on their own, particularly if their finances are relatively straightforward. Others find that the coordination required:

- investment management

- Social Security optimization

- tax planning

- healthcare planning

benefits from working with a professional, particularly a fiduciary advisor who is legally required to act in your best interest.

A Practical Review Checklist for the Next 5–10 Years

If you’re within a decade of retirement, here are some core areas worth reviewing — ideally with a financial professional who can look at the full picture:

- Retirement spending estimate: Have you mapped out what you actually expect to spend in retirement, including healthcare and travel?

- Savings progress: Are your current balances and contribution rate putting you on a realistic track toward your target?

- Investment allocation: Does your current mix of stocks, bonds, and other assets reflect your timeline and income needs — not just your comfort level from years ago?

- Social Security strategy: Have you run the numbers on different claiming ages, including the impact on a spouse’s benefit?

- Healthcare coverage plan: Do you know how you’ll cover healthcare costs, especially if you retire before 65?

- Debt picture: What debt will you carry into retirement, and what is your plan for managing it?

- Tax strategy: Do you understand the tax treatment of your various retirement accounts and how withdrawals may affect your overall tax situation?

- Emergency and flexibility reserves: Do you have liquid assets available for unexpected expenses without having to sell long-term investments at an inopportune time?

Key Takeaways

- Economic surprises: market downturns, inflation spikes, rate changes — are a normal part of long-term investing, not rare exceptions.

- The decade before retirement is when these surprises can do the most damage, due to something called sequence of returns risk.

- Retirement readiness isn’t just about your account balance; it involves coordinating spending plans, healthcare, Social Security timing, debt, and taxes.

- The goal of retirement planning isn’t to predict the economy. It’s to build a plan flexible enough to adapt when conditions change.

- Reviewing your core assumptions in the five to ten years before retirement and adjusting where needed, can make a significant difference in your long-term outcomes.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.