Four profiles. One of them will feel uncomfortably familiar.

Markets are unsettled. Oil prices have surged more than 40% in two weeks. The jobs report delivered an unexpected loss of 92,000 positions. Geopolitical risk is real, ongoing, and with no clear resolution in sight. In weeks like this one, something revealing happens: investors show you exactly who they are.

The four investor types below are not personality tests. They are behavioral patterns drawn from 30 years of data on how real investors actually respond to market stress. Each pattern feels justified in the moment. Each one has a measurable long-term cost. And each one has a structural fix that works better than willpower.

Read all four. Be honest about which one sounds most like you. Then read the “What to Say to Your Advisor” line at the end of your profile; that is your starting point for the conversation that matters most right now.

8.48%

The gap between the average equity investor’s return and the market’s return in 2024. Source: DALBAR Quantitative Analysis of Investor Behavior, 2025. This gap is not caused by bad funds. It is caused entirely by behavior.

Investor Type 01: The Panic Seller

“I just need to stop the bleeding.”

What You Tell Yourself

“This is different. I’ll get back in when things settle down. I can’t watch this any longer.”

| What Actually Happens | The Long-Term Cost |

|---|---|

| You sell during the downturn and move to cash. The pain stops — temporarily. Markets don’t announce their recoveries. They happen suddenly, often while the headlines are still alarming. You miss the rebound. When things feel safe enough to re-enter, prices are higher than where you sold. You either buy back at a loss or stay out even longer, missing more of the recovery. | Seven of the ten best single-day market returns over any 20-year period happened within two weeks of the ten worst days. Missing just 15 of the best trading days over 20 years can cut total portfolio growth by more than half. The loss is locked in. The recovery belongs to whoever stayed. |

| You Might Be This Type If… | The Structural Fix |

|---|---|

| You have checked your portfolio balance more than once this week. You have thought about moving to cash until things calm down. You have described the current environment as different from past downturns. You feel more urgency to act than to review your written plan. | Build a 12 to 24 month cash buffer outside your investment accounts. This removes the financial pressure to sell investments to pay bills. Write down today what you will do if markets fall 20%; a calm decision made in advance is far more reliable than one made under stress. Commit to a 48-hour rule: before any portfolio move during a downturn, wait two days and speak with your advisor first. |

What to Say to Your Advisor

“I have been thinking about moving to cash. Before I do anything, I want to walk through what that has historically cost investors and what a better structural alternative looks like.”

Investor Type 02: The Performance Chaser

“I’m not missing the next big run.”

What You Tell Yourself

“Everything is moving into energy and defense right now. My portfolio missed the last run. I need to reposition.”

| What Actually Happens | The Long-Term Cost |

|---|---|

| You move money toward whatever has risen most recently; buying after the run has already happened. When that sector’s leadership cycle ends, and cycles always end, you are overexposed to exactly the area correcting the hardest. You then consider moving to the next thing that has been rising. The pattern repeats. | DALBAR’s 30-year research shows investors consistently underperform the very funds they own, because they buy after those funds have risen and sell after they have fallen. In 2024, the average equity investor trailed the market by 8.48 percentage points despite owning funds in a strong market year. |

| You Might Be This Type If… | The Structural Fix |

|---|---|

| You have recently thought about adding energy, defense, or gold because of current headlines. You find yourself envying returns from sectors you did not own last quarter. You have moved money based on a news story or analyst recommendation in the past year. Your allocation has drifted significantly from your original plan. | Set a rebalancing trigger based on allocation drift, not performance rebalance when a position moves more than 5% from your target, not because it has risen. Before adding any new position, write the reason in one sentence — if it includes “it has been doing well,” treat that as a warning sign, not a rationale. Ask your advisor to calculate the net effect of your last three timing decisions on actual returns versus a simple buy-and-hold baseline. |

What to Say to Your Advisor

“I want to look at the actual net return of the timing moves I have made in the past two years — and compare that to what I would have earned by not moving at all.”

Recognize Yourself in Type 1 or Type 2?

Both patterns are common, both feel reasonable in the moment, and both have structural fixes that work better than willpower. We will review your specific situation and show you exactly what a buffer or rebalancing trigger would look like in your plan. Free, no obligation, about 20 minutes.

Schedule Your Free Portfolio Review →

Investor Type 03: The False Safety Seeker

“At least I won’t lose anything in cash.”

What You Tell Yourself

“I’m going to move most of this to money market or short-term CDs until I have more clarity. At my age I can’t afford big losses.“

| What Actually Happens | The Long-Term Cost |

|---|---|

The portfolio moves to cash or short-term instruments. The balance stabilizes and anxiety decreases. But inflation continues. Expenses keep rising. The portfolio, sitting in cash, falls behind the cost of the retirement it was built to fund. The losses are invisible — they show up not as a declining balance but as a widening gap between what you have and what you need. | At 4% inflation, $500,000 in cash has roughly $274,000 of real purchasing power in 10 years. The balance on the statement looks the same. The ability to fund retirement does not. A retiree with a 20 to 25-year horizon who moves entirely to cash is trading a visible, temporary loss for an invisible, permanent one. |

| You Might Be This Type If… | The Structural Fix |

|---|---|

| You believe preserving the stated balance matters more than preserving purchasing power. You have moved or considered moving to cash or CDs during the past six months. You describe your approach as conservative but have not calculated your real return against inflation. Your portfolio’s time horizon on paper is shorter than your actual life expectancy. | Calculate your real return: subtract your expected inflation rate from your current total portfolio return. If the result is near zero or negative, the “safe” move is producing a guaranteed real loss. Build a two-bucket structure — stable assets covering 12 to 24 months of spending needs, growth assets for the long horizon. This is different from moving everything to cash. Have a specific conversation about your actual time horizon: at age 65, a 25-year retirement is common, and that changes the math significantly. |

What to Say to Your Advisor

“I want to understand what my real return looks like after inflation and see what a two-bucket structure would look like for my specific situation.”

Investor Type 04: The Disciplined Holder

“My plan was built for weeks like this one.”

What You Tell Yourself

“The headlines are loud. My allocation is within range of my plan. I have enough in stable assets to cover near-term expenses. I don’t need to do anything.”

| What Actually Happens | The Long-Term Result |

|---|---|

| You review your allocation against your written financial plan. You confirm your cash buffer covers near-term expenses without touching investments. If allocation has drifted outside your target range, you rebalance, not because of the headlines, but because the plan says to. You do not check your balance compulsively. You are uncomfortable, but not reactive. | The Disciplined Holder is the investor type DALBAR’s research consistently identifies as the one that captures what markets actually deliver over time, not because they predicted correctly, but because they built a structure that made prediction unnecessary and held to it when everything said to abandon it. |

| You Might Be This Type If… | The Structural Fix |

|---|---|

| You have a written financial plan and can describe your target allocation. You have 12 or more months of essential expenses in stable assets outside your investment portfolio. You have already discussed what you would do if markets fell 20%; before it happened. Your last portfolio change was driven by a change in your plan, not a change in the news | Continue exactly as you are, the value of discipline compounds over time just as returns do. Review your cash buffer annually to confirm it still covers 12 to 24 months of expenses at today’s prices; inflation may have quietly changed this number. Use this article as a conversation starter with someone you know who may be in one of the other three categories |

What to Say to Your Advisor

“I want to confirm my plan is still current and make sure my buffer still covers what I actually spend today, not what I budgeted two or three years ago.”

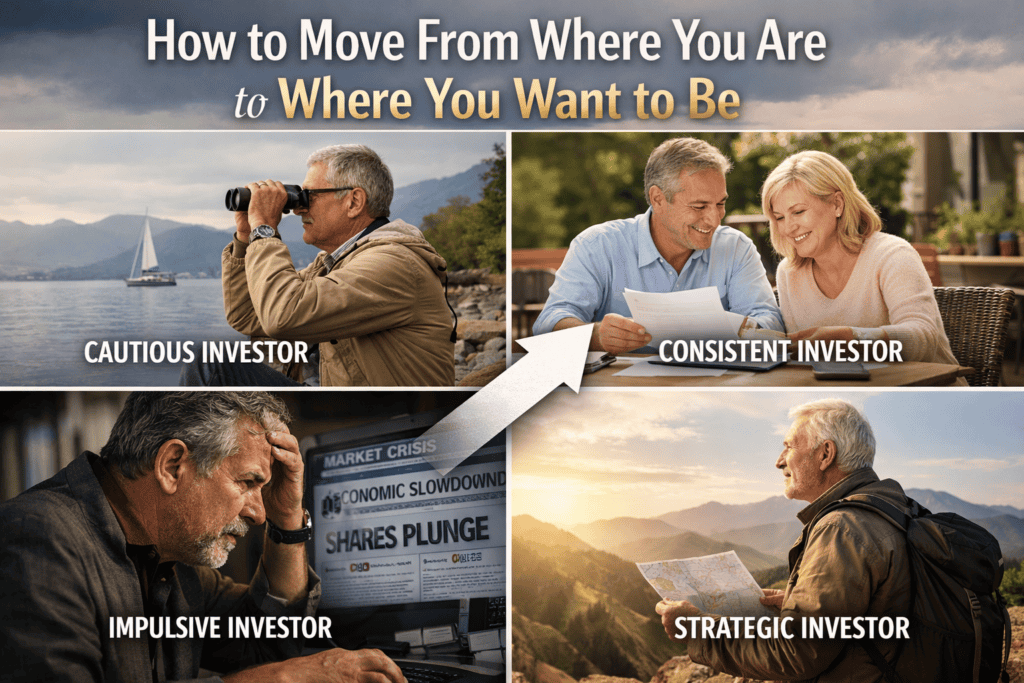

How to Move From Where You Are to Where You Want to Be

Most investors are not permanently fixed in one type. The behavioral patterns are habits, and habits change when the underlying structure changes. The research is consistent on this point: willpower is not the solution. Structure is. A plan that removes the pressure to act under stress is worth more than the discipline to resist acting.

If you recognized yourself in Types 1, 2, or 3, three structural changes address the large majority of behavioral risk and none of them require you to predict what markets will do next.

1 — Build the Buffer

Identify your monthly essential expenses. Multiply by 12 to 24. Confirm that amount exists in stable, liquid assets outside your investment portfolio. If it does not, this is the first priority. The buffer eliminates the most common source of forced selling in retirement.

2 — Write the Decision

Answer this question in writing today: if markets fall 20%, what will I do? Share that answer with your advisor. A decision made calmly and in advance is worth far more than one invented under stress. The plan becomes the decision-maker, not the emotion.

3 — Have the Conversation

Schedule a behavioral review with your advisor; not a portfolio review, a behavioral one. Discuss which type you are, what your specific triggers are, and what the plan says to do when those triggers activate. This conversation is most valuable before a crisis, not during one.

The goal is not to become someone who feels nothing during volatile markets. Volatility is uncomfortable for every investor. The goal is to build a structure that makes that discomfort irrelevant to the outcome; a plan that holds up not because you summoned the willpower to hold it, but because you removed the financial conditions that make panic rational.

“The most important question is not what type you are. It is whether your current structure reduces or amplifies the cost of being that type.”

Want to Know Which Type Your Portfolio Is Built For?

We will review your current allocation, income structure, and buffer level and tell you clearly whether your plan reduces or amplifies behavioral risk when markets get difficult. Most people are surprised by what the structure reveals. Free, no obligation, about 20 minutes.

Schedule Your Free Behavioral Planning Conversation →

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.