What every pre-retiree should know about rising costs — and how to keep your retirement plan on solid ground.

Most people think of inflation as a grocery store problem. Prices go up, the weekly shopping bill gets a little bigger, and life goes on. But for people who are five to fifteen years away from retirement, inflation is something much more consequential than that.

It’s a threat to the math that underlies your entire retirement plan.

Here’s why: retirement is essentially a long-term income problem. You stop earning a regular paycheck, and your savings (along with Social Security and any other income sources) have to cover your living expenses for potentially 25 to 30 years or more. When inflation is higher than your plan assumed, every one of those years costs more than you expected.

That reality became very concrete for millions of Americans recently. Between early 2021 and mid-2022, the U.S. Consumer Price Index (CPI) rose by more than 13% in total; a surge not seen since the early 1980s, according to the U.S. Bureau of Labor Statistics. Gasoline, groceries, housing, insurance, and healthcare all climbed sharply. For people already in retirement or close to it, that wasn’t an abstract economic statistic. It was a direct hit to their purchasing power.

| Why This Matters for Pre-Retirees Specifically During your working years, a raise or job change can help offset rising costs. In retirement, most income sources are largely fixed. That’s what makes inflation uniquely challenging for retirees — and why it deserves serious attention before you stop working. |

What Inflation Actually Does to a Retirement Plan

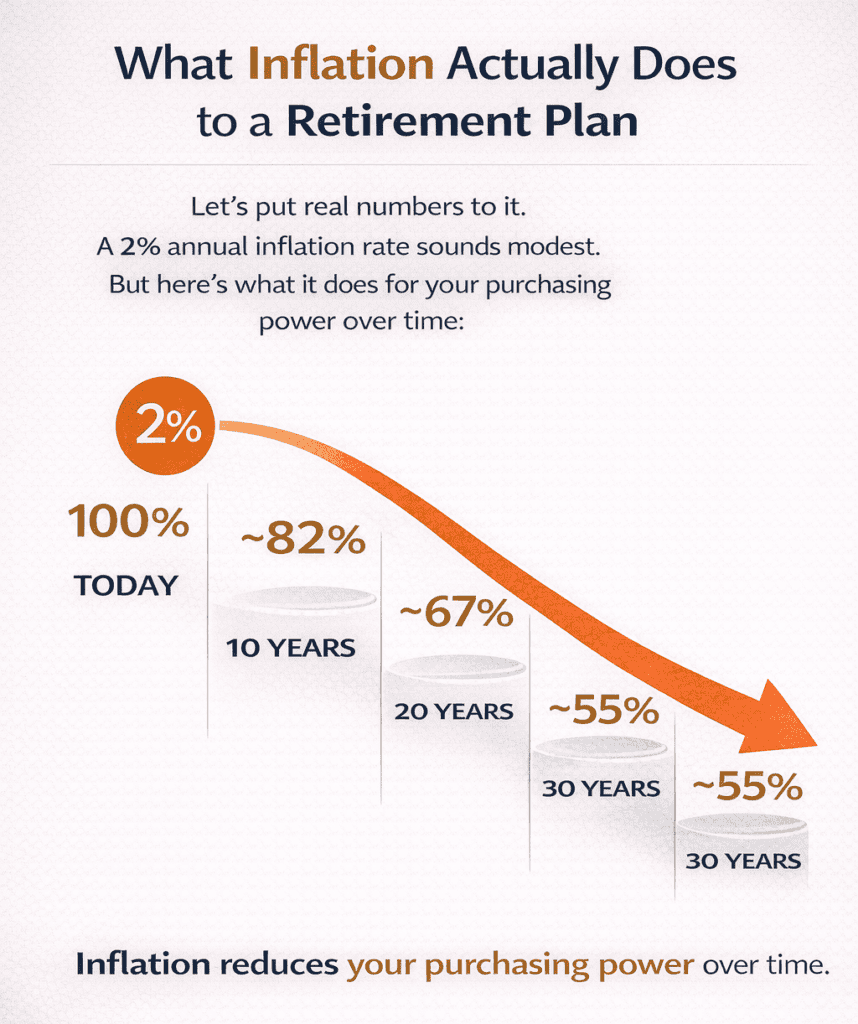

Let’s put some real numbers to it. The Federal Reserve’s long-run inflation target is 2% per year. That sounds modest. But here’s what 2% annual inflation does to purchasing power over time:

- At 2% inflation, $100,000 in purchasing power today becomes roughly $82,000 in 10 years

- Over 20 years, that same $100,000 in purchasing power drops to about $67,000

- Over 30 years, it falls to around $55,000

In other words, even “normal” inflation quietly cuts your purchasing power nearly in half over a 30-year retirement. And if inflation runs higher than 2%, as it has in recent years, the erosion happens faster.

This is why retirement plans need to account for inflation explicitly, not just assume that today’s dollars will have the same value in 20 years.

The Compounding Problem

Inflation compounds over time just like investment returns do, but in the opposite direction. A retirement plan that projects $60,000 in annual expenses today needs to account for the fact that covering that same lifestyle in year 20 of retirement may require $90,000 or more, depending on inflation.

Many people build retirement plans using “today’s dollars” without fully accounting for how their expenses will grow in nominal terms. That gap, between what you project and what you’ll actually spend, is one of the more common sources of surprise for retirees.

| A Concrete Example Suppose your retirement budget today is $5,000 per month. At 3% annual inflation, that same lifestyle costs roughly $6,720 per month in 10 years, and about $9,030 per month in 20 years. If your income sources don’t keep pace, you’re facing a real shortfall — even if your account balance is exactly where you planned it to be. |

Where Inflation Hits Hardest for Retirees

Not all expenses inflate at the same rate. Some areas tend to be especially sensitive and they happen to be the areas that matter most in retirement.

Healthcare

Healthcare inflation has historically outpaced general inflation. According to the Peterson-KFF Health System Tracker, healthcare spending per person in the U.S. has grown faster than the general economy in most years over the past two decades. Medicare premiums, prescription drug costs, dental work, vision, hearing aids, and long-term care costs all tend to rise over time — and for most people, healthcare needs increase with age.

The Employee Benefit Research Institute (EBRI) has estimated that a 65-year-old couple with median prescription drug expenses may need $296,000 or more in savings just to cover healthcare costs in retirement — a figure that assumes Medicare coverage. Without dedicated planning, healthcare inflation alone can significantly destabilize a retirement budget.

Housing Costs

Even if your mortgage is paid off, housing costs don’t stop. Property taxes, homeowner’s insurance, maintenance, and utilities all tend to rise over time. Homeowners in many parts of the country have seen property taxes increase sharply over the past decade as home values climbed. These aren’t optional expenses — they’re built into the cost of keeping a roof over your head.

Groceries and Everyday Purchases

Food inflation has been particularly noticeable in recent years. The USDA reported that grocery prices rose more than 20% cumulatively between 2020 and 2023 — a pace well above historical norms. While food prices tend to moderate over time, the base has been reset at a higher level for millions of households.

Insurance Premiums

Auto insurance, homeowner’s insurance, and supplemental Medicare (Medigap) premiums have all increased significantly in recent years. Insurance costs can be difficult to forecast because they can jump sharply based on factors largely outside your control:

- weather events

- rising repair costs

- broader market conditions in the insurance industry

Travel and Leisure

This one catches many pre-retirees off guard. Early retirement is often when people travel most. Airline tickets, hotel stays, and cruise fares have all experienced notable price increases in recent years. If your retirement plan assumed that leisure spending would be modest, but you hope to travel actively in your first decade of retirement, it’s worth revisiting those assumptions.

Does High Inflation Mean You Need to Delay Retirement?

Not necessarily, but it may mean you need to look more carefully at your numbers.

When inflation pushes projected retirement spending higher, some pre-retirees do find that their original timeline needs to be adjusted. Others find that modest changes to their plan, rather than a wholesale delay, are enough to keep them on track.

Here are some of the adjustments that planners often consider:

1. Updating Your Spending Projections

This is the most important first step. If your retirement spending estimate was built two or three years ago, it may significantly understate what you’ll actually need. Going line by line through your expected budget — with current prices in mind — gives you a much more accurate picture than a broad estimate.

2. Revisiting Social Security Timing

Social Security benefits include a built-in inflation protection mechanism: the Cost of Living Adjustment (COLA). In 2023, the COLA was 8.7% — the largest increase since 1981. In 2024, it was 3.2%. These adjustments mean that your Social Security benefit maintains purchasing power over time in a way that most other income sources do not.

This makes the timing of when you claim Social Security even more meaningful. Delaying your claim (up to age 70), not only increases your base benefit by approximately 8% per year past your full retirement age, it also increases the base on which future COLAs are calculated. For people worried about inflation, a larger, COLA-adjusted Social Security benefit can be one of the most effective long-term hedges available.

3. Reviewing Investment Allocation for Inflation Sensitivity

Some asset classes have historically provided better inflation protection than others. Equities (stocks), for example, represent ownership in businesses that can often raise their own prices over time — which can help offset inflation effects over the long run. Certain real assets, Treasury Inflation-Protected Securities (TIPS), and inflation-adjusted annuities are tools that some financial advisors use specifically to address inflation risk in retirement portfolios.

This doesn’t mean abandoning a diversified approach. It means making sure your investment strategy accounts for inflation as one of the real risks you’re managing; not just market volatility.

4. Working One or Two Additional Years

This option is worth examining without immediately dismissing. Working two additional years beyond your original target date does three things simultaneously: it adds more to your savings, it shortens the period your savings must last, and it allows more time for your investments to potentially grow. In periods of elevated inflation, this combination can meaningfully close the gap between what you had planned and what current conditions require.

5. Adjusting Spending Targets — Particularly in Early Retirement

Some retirement income strategies build in intentional spending flexibility. Rather than setting a fixed withdrawal amount, they plan for a slightly lower floor and a reasonable ceiling, with the ability to adjust based on market and inflation conditions. Being modestly flexible in early retirement spending can provide significant protection for the later years when healthcare costs are likely to be highest.

| A Note on Inflation and Fixed Income Bonds, CDs, and cash-equivalent savings accounts offer stability but generally don’t keep pace with inflation over time. A retiree who holds a large portion of their savings in low-interest fixed accounts may be in a worse position in year 15 of retirement than they were in year one — even if they never touched the principal. This is the “slow leak” effect of inflation on fixed-income-heavy portfolios. |

When Did You Last Review Your Retirement Spending Assumptions?

This is the most practical question in this entire article. Retirement plans are built on projections — and projections need to be updated as conditions change.

If your retirement spending estimate was built before 2022, it was likely built before the most significant inflation surge in four decades. The numbers may need to be revisited.

Here are some specific areas worth reviewing with current-day prices in mind:

- Grocery and household expenses: What does your actual monthly spending look like today vs. what the plan assumed?

- Housing-related costs: Have property taxes, insurance premiums, or HOA fees increased since your plan was built?

- Healthcare costs: Have your insurance premiums or out-of-pocket medical costs changed significantly?

- Utilities and energy: Electricity, gas, and water costs have risen sharply in many parts of the country

- Transportation: Auto insurance costs in particular have climbed significantly in recent years

Even small per-category increases can add up to a meaningful difference in your total monthly picture. A plan that assumed $4,500 per month in expenses but now looks more like $5,200 is a gap worth addressing before retirement, not after.

Common Questions About Inflation and Retirement

“Doesn’t my portfolio’s investment growth offset inflation?”

It can, but it’s not automatic. Equities have historically outpaced inflation over long time periods, which is one reason financial planners generally recommend maintaining a meaningful allocation to stocks even in retirement. However, investment returns are not guaranteed, vary from year to year, and depend heavily on your specific allocation and market conditions. Assuming your portfolio will offset inflation without specifically planning for it is a risk many people discover too late.

“Is inflation going to stay high?”

No one can say with certainty. Inflation dropped significantly from its 2022 peak, but the path forward is uncertain. The Federal Reserve’s goal is to maintain inflation near 2% over time — but the experience of 2021–2023 was a reminder that inflation can move faster and stay elevated longer than most forecasts expect. The prudent approach is to build a retirement plan that doesn’t depend on inflation returning to any specific level.

“What if I’m already retired and inflation is eating into my budget?”

This is a real challenge for many current retirees. Some options that financial advisors may explore include reviewing whether the asset allocation still makes sense given the current environment, examining whether spending in any categories can be reduced or deferred, evaluating whether part-time work or other income sources are practical, and reviewing Social Security claiming strategy if you or a spouse haven’t yet claimed. These conversations are worth having with a fiduciary financial advisor who can look at your complete situation.

“Should I rush to retire before inflation gets worse?”

This is a question worth thinking through carefully rather than acting on quickly. Rushing into retirement before you’re financially ready, because of worry about future inflation, can actually increase your vulnerability to exactly the problem you’re worried about. A retirement that starts underprepared is harder to recover from than one that starts a year or two later with a stronger financial foundation.

“How much inflation should I assume in my retirement plan?”

Financial planners commonly use assumptions in the range of 2.5% to 3.5% for general inflation, with higher assumptions (sometimes 4% to 6%) for healthcare costs specifically. These are planning assumptions — not predictions. Using a slightly higher inflation assumption than you think is likely is a form of building in a margin of safety. Your specific assumptions should be part of a conversation with a financial professional who understands your situation.

A Practical Checklist: Inflation-Proofing Your Retirement Plan

If you’re within ten years of retirement, here are specific steps worth taking:

- Rebuild your retirement spending estimate using today’s prices — not the numbers from a plan created two or more years ago

- Stress-test your plan against 3% and 4% inflation assumptions, not just 2%, to see how your projected income holds up

- Review your Social Security strategy — particularly whether delaying your claim (if feasible) could provide a larger inflation-adjusted income base

- Examine the inflation sensitivity of your current investment allocation — are you carrying more fixed, low-yield assets than may be appropriate given your timeline?

- Specifically estimate healthcare costs and build in a separate buffer, since healthcare inflation historically outpaces general inflation

- Check property taxes, insurance premiums, and other recurring fixed costs for recent increases that may not be reflected in your projections

- Ask your financial advisor whether your plan has an explicit inflation assumption built in — and what it is

Key Takeaways

- Inflation doesn’t just affect today’s grocery bill — it erodes the purchasing power of your retirement savings over a 20 to 30-year retirement.

- Even modest 2–3% inflation can cut purchasing power nearly in half over a long retirement. Higher inflation accelerates that erosion.

- Healthcare, housing, insurance, and food costs have been among the hardest-hit categories in recent years — all of which are central to retirement budgets.

- Social Security’s COLA adjustments make it one of the most effective inflation hedges available to retirees — another reason why claiming timing matters.

- Retirement plans built two or more years ago may be using spending assumptions that no longer reflect current prices and should be revisited.

- There are practical steps — updating projections, reviewing investment allocations, adjusting Social Security timing — that can strengthen a retirement plan against inflation without necessarily requiring a later retirement date.

About the Financial Planning Author

Alex Langan, J.D., CFBS

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.

No Fields Found.