Many people wonder, “Am I on track with my 401(k)?” Having a few checkpoints can help you see where you stand — and what small changes can make a big difference.

401(k) Benchmarks: What Experts Suggest

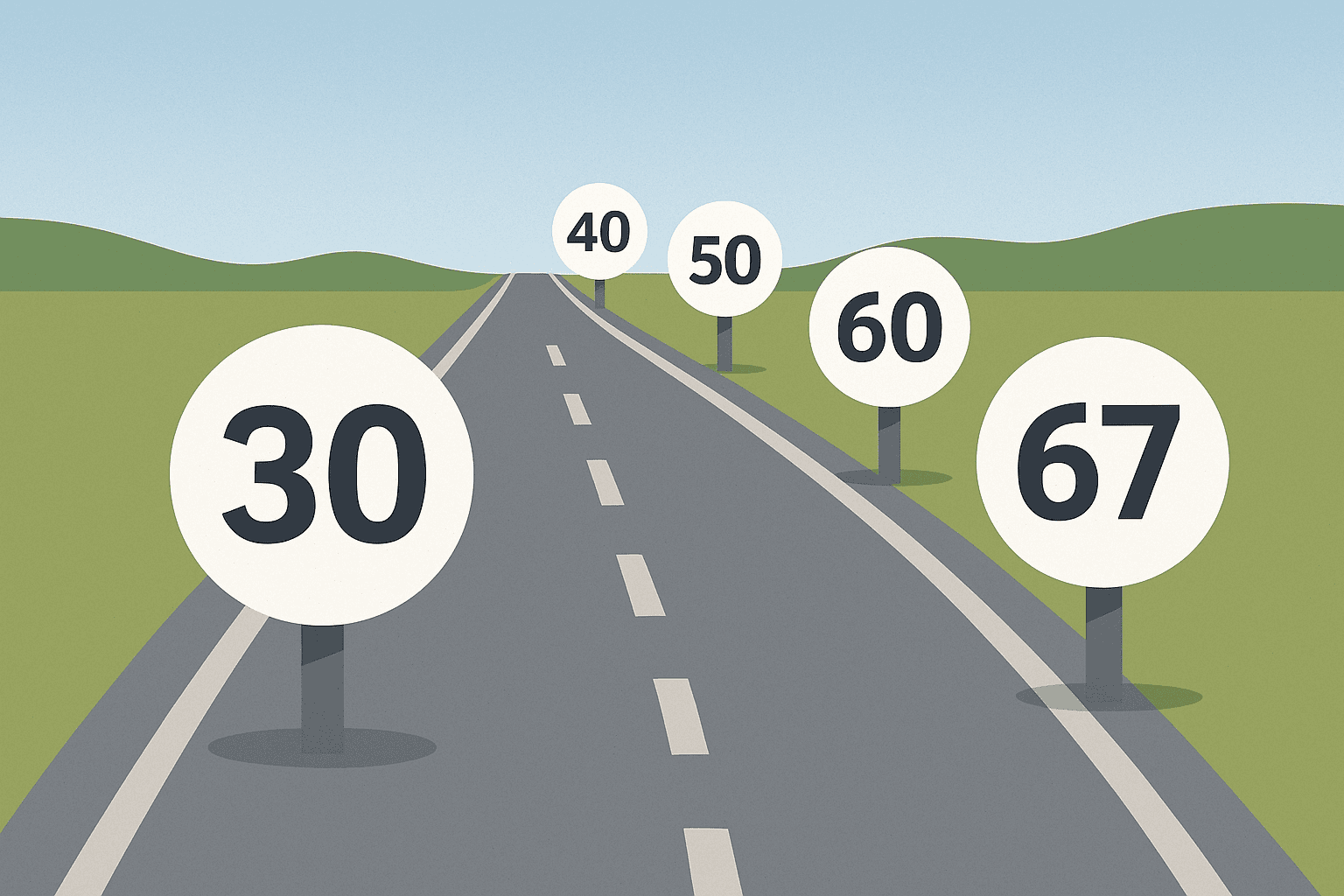

Financial planners often use income multiples as targets:

| Age | Suggested Savings Target | Why It Helps |

| 30 | 1× your annual pay | Get your footing early |

| 40 | 3× your pay | Start compounding seriously |

| 50 | 6× your pay | Catch-up years loom |

| 60 | 8× your pay | Close to replacement needs |

| 67 | 10× your pay | Aiming for retirement readiness |

(Source: Fidelity Retirement Research, 2025)

Average 401(k) Balances

Real 401(k) balances show a different picture. Here are the average balances by age group in 2025 (Fidelity data):

| Age Group | Average 401(k) Balance |

| 20s | ~$74,800 |

| 30s | ~$112,000 |

| 40s | ~$168,000 |

| 50s | ~$205,000 |

| 60s+ | ~$256,600 |

These numbers are averages — meaning some people are far above and many are below. The key is not comparison, but progress.

Forecasts: What Your 401(k) Could Grow Into

Let’s say you’re 40 years old, making $100,000 a year, with $300,000 saved:

| Growth Rate | Balance at 67 | Potential Annual Income at 4% Withdrawal* |

| 5% return | ~$1,080,000 | ~$43,200 |

| 7% return | ~$1,530,000 | ~$61,200 |

*Hypothetical illustration. Does not include Social Security or other income.

Why Use Auto-Escalation For Your 401(k)

Auto-escalation is when you set your 401(k) contribution to increase automatically by 1% each year.

Why it works:

- You raise your savings rate slowly, so it doesn’t feel like a pay cut.

- By your highest earning years, you’re putting away much more without having to think about it.

Example: If you start at 10% and add 1% each year until 15%, that extra bump could mean hundreds of thousands of dollars more at retirement, depending on your timeline, balance, and returns. The power of compound interest is truly remarkable!

Common 401(k) Saving Mistakes People Make (And Fixes)

Mistake #1: Not increasing savings after raises

- Fix: Automate 1% bumps each year, or raise contributions when your income grows.

Mistake #2: Cashing out when changing jobs

- Around 41% of people leaving jobs cash out their 401(k), which triggers taxes, penalties, and lost growth.

- Fix: If you are able to, roll the old account into your new 401(k) or an IRA instead of cashing out.

Mistake #3: Leaving multiple accounts scattered

- Old accounts left behind may be forgotten, misaligned with your needs, or stuck in high-fee investments.

- Fix: Consolidate where possible so your portfolio is easier to manage and better reflects your goals.

Mistake #4: Relying only on your 401(k)

- A 401(k) is powerful, but it may have limited investment choices or higher fees.

- Fix: Supplement with IRAs, HSAs, or taxable investment accounts for flexibility and tax advantages.

Mistake #5: Forgetting catch-up contributions

- In 2025, the limit is $23,500, and if you’re 50+, you can add $7,500 more.

- Fix: Use catch-up contributions if you’re eligible — it’s the largest ever allowed.

Remember: Numbers Aren’t the Whole Story

Benchmarks, averages, and forecasts all help. But what matters most is how your plan fits you:

- Your goals

- Your lifestyle

- Your timeline

- Your tax and healthcare picture

Two people with the same balance may live very different retirements.

Managing Your 401(k) Balance

Benchmarks give you a roadmap. Averages show where people stand today. Auto-escalation shows how small steps can add up. Put together, they can give you confidence — and remind you that the best plan is one designed around you.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.