Why Understanding the Gaps Can Save Your Retirement Plan

What Most Retirees Overlook

As you enter retirement, it’s natural to assume Medicare will cover most of your healthcare needs. But here’s the truth: Medicare covers short-term medical care, not long-term daily care. This misunderstanding leads to some of the biggest financial surprises in retirement.

If you or a loved one needs help with bathing, dressing, memory care, or assisted living—Medicare alone won’t help much. That’s why understanding your options before you need them is so important.

What Medicare Actually Covers

Original Medicare (Parts A & B) includes:

- Hospital stays and surgeries (Part A)

- Doctor visits, outpatient care, diagnostic tests (Part B)

- Home health services (short-term, skilled care only)

- Skilled nursing facility rehab — but only for up to 100 days and after a qualifying hospital stay

- Hospice care for terminal illness

But it does not cover:

- Long-term custodial care

- Assisted living

- Ongoing nursing home care

- Help with daily activities (ADLs)

Adding More Coverage: Medigap & Medicare Advantage

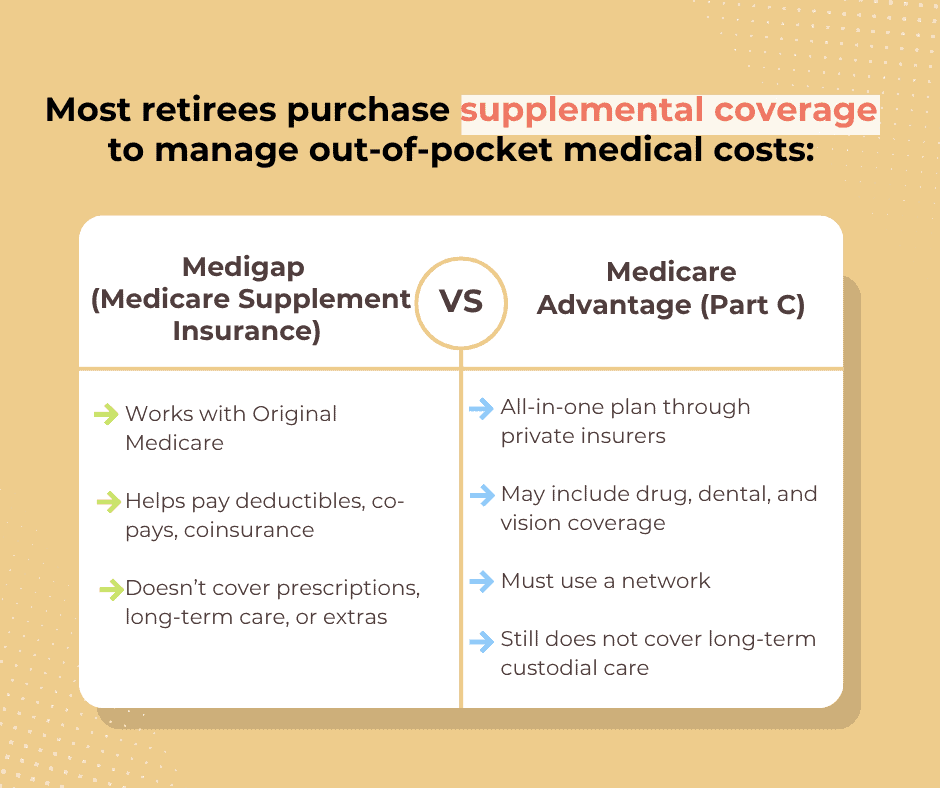

Most retirees purchase supplemental coverage to manage out-of-pocket medical costs:

1. Medigap (Medicare Supplement Insurance)

- Works with Original Medicare

- Helps pay deductibles, co-pays, coinsurance

- Doesn’t cover prescriptions, long-term care, or extras

2. Medicare Advantage (Part C)

- All-in-one plan through private insurers

- May include drug, dental, and vision coverage

- Must use a network

- Still does not cover long-term custodial care

What About Long-Term Care Insurance?

LTC insurance is the only tool specifically built to cover:

- Assisted living

- Memory care

- Nursing home stays

- Custodial in-home care

Hybrid policies that combine life insurance with LTC benefits are increasingly popular and offer more flexibility.

Comparing Your Coverage Options

| Service / Feature | Original Medicare | Medigap / Advantage | Long-Term Care Insurance |

| Hospital & outpatient medical care | ✅ Yes | ✅ Yes | ❌ No |

| Prescription drugs | ❌ (Part D needed) | ✅ Often included (Advantage) | ❌ No |

| Assisted living, nursing home, or in-home ADL care | ❌ Not covered | ❌ Not covered | ✅ Covered by most policies |

| Help with daily activities (bathing, dressing) | ❌ Not covered | ❌ Not covered | ✅ Often included |

| Hospice care | ✅ Yes | ✅ Yes | ✅ Sometimes included |

| Requires separate premium | No (but has deductibles) | ✅ Yes | ✅ Yes |

What About Medicaid?

While Medicaid is a last-resort option for low-income individuals, it comes with a 5-year lookback rule. If you transferred assets or gave large gifts within five years of applying, you could face a penalty period where you must cover care costs out of pocket—even if you no longer have the assets.

This often surprises families who assume they can “gift away” assets late in life to qualify. In reality, Medicaid planning needs to be done years in advance.

That’s why many high-net-worth families prefer to maintain control through private insurance, trust structures, or income-based planning.

Real Costs to Plan For

| Type of Care | National Median | Pennsylvania Median |

| In-home aide (44 hrs/week) | $5,720/month | ~$5,300/month |

| Assisted living (private, 1BR) | $5,350/month | ~$4,800/month |

| Nursing home (semi-private room) | $8,669/month | ~$10,000/month |

| Nursing home (private room) | $9,733/month | ~$11,200/month |

*Source: Genworth Cost of Care Survey (2024 estimates)

Why This Isn’t Just About Money

Care decisions are deeply personal. Without a plan:

- Spouses may have to drain shared savings

- Adult children may step in as caregivers or decision-makers

- You may lose the ability to choose where and how you’re cared for

A well-designed plan gives you and your family clarity, dignity, and control—no matter what the future holds.

Planning Recommendations

- Evaluate Long-Term Care Insurance Early

- More options are available when you’re younger and healthier.

- Hybrid policies can protect both income and estate.

- Stress Test Your Financial Plan

- Include real-life care scenarios: dementia, mobility loss, single-spouse need.

- Clarify Your Care Preferences

- In-home vs. facility, family involvement, care quality.

Thinking About Medicare & Long Term Care

Medicare is essential—but it’s not enough on its own. The best time to plan for long-term care is when you don’t need it yet. Because the peace of mind you’ll have later starts with the decisions you make today.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.