62% of pre-retirees are uncertain their savings will last through retirement.

But here’s the thing: it’s rarely about how much you saved.

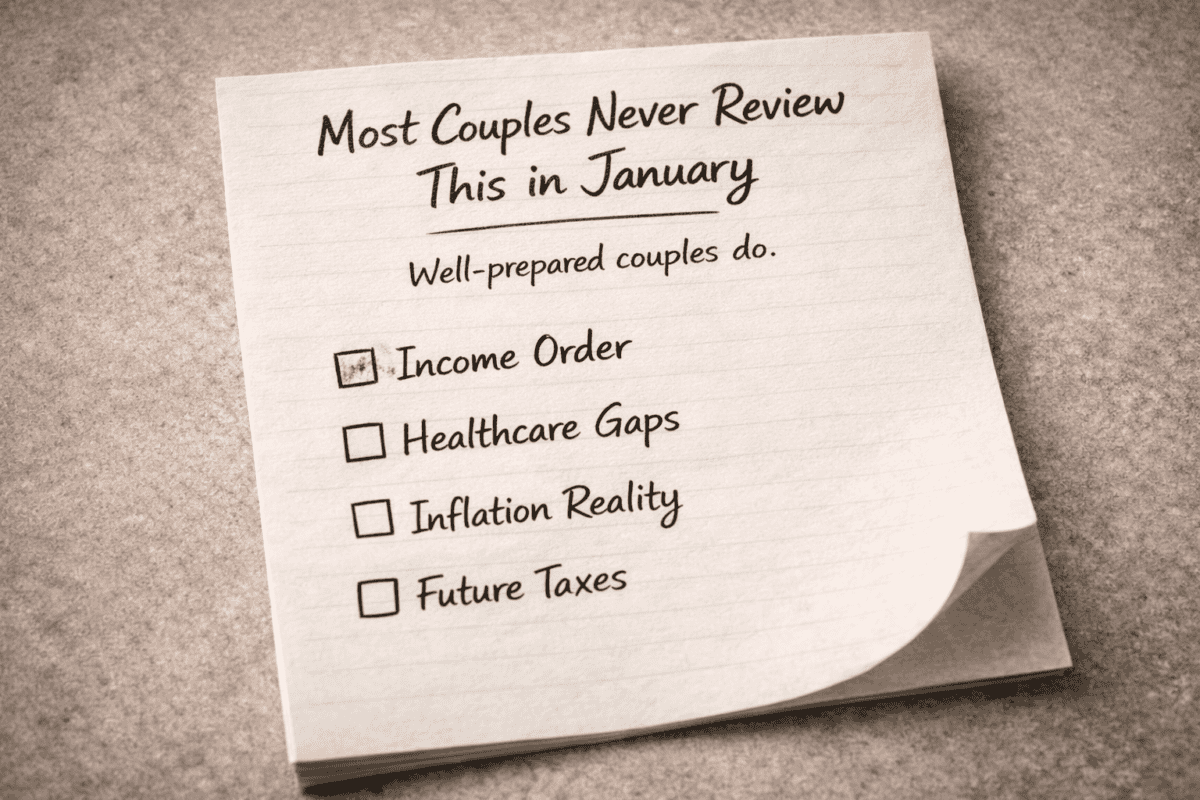

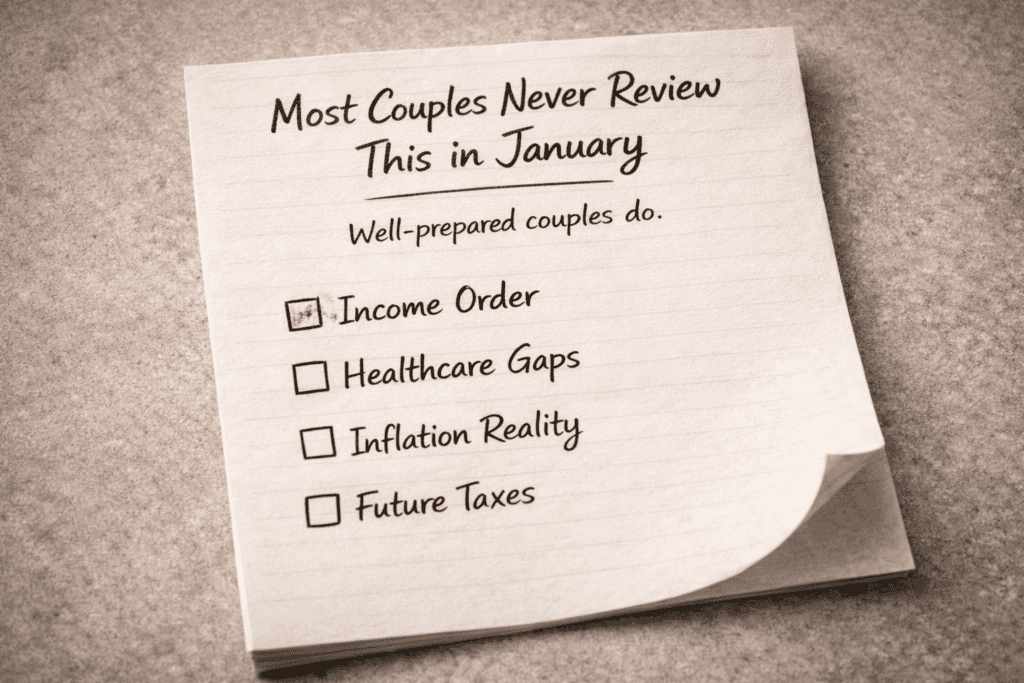

It’s about whether you’ve reviewed the five areas that actually determine if your retirement works.

Retirement issues rarely show up early. They show up later—when choices are limited, income matters more, and mistakes feel permanent.

January is the perfect time to review the whole system before retirement begins—while you still have flexibility.

Below are the five areas we encourage couples to review each January—with a simple way to start today.

1) Retirement Income Plan (and Sequence-of-Returns Risk)

Why this is important

Most people focus on how much they’ve saved. Fewer know how they’ll turn savings into a paycheck.

The first years after you stop working matter more than most people realize. If markets fall early and you’re pulling income, it can reduce the long-term staying power of a portfolio—this is sequence-of-returns risk.

Here’s what this looks like in real life:

Mark and Linda had $1.2 million saved. They retired in 2022, started taking $60,000/year from their portfolio, and watched it drop 18% their first year. Two years later, their balance was $890,000—not because they overspent, but because they pulled money during down markets. A different withdrawal strategy (pulling from cash/bonds in down years) could have preserved $150,000+ of their portfolio.

Morningstar’s retirement research regularly updates what “safe withdrawal” looks like as inflation and market assumptions change.

How to fix it

You don’t need a perfect plan. You need a paycheck plan:

- Decide which accounts fund Year 1–3 of retirement (cash/bonds vs. stocks)

- Use a guardrail approach (spend a little less after down years; a little more after strong years)

- Stress-test income with “bad early years,” not just average markets

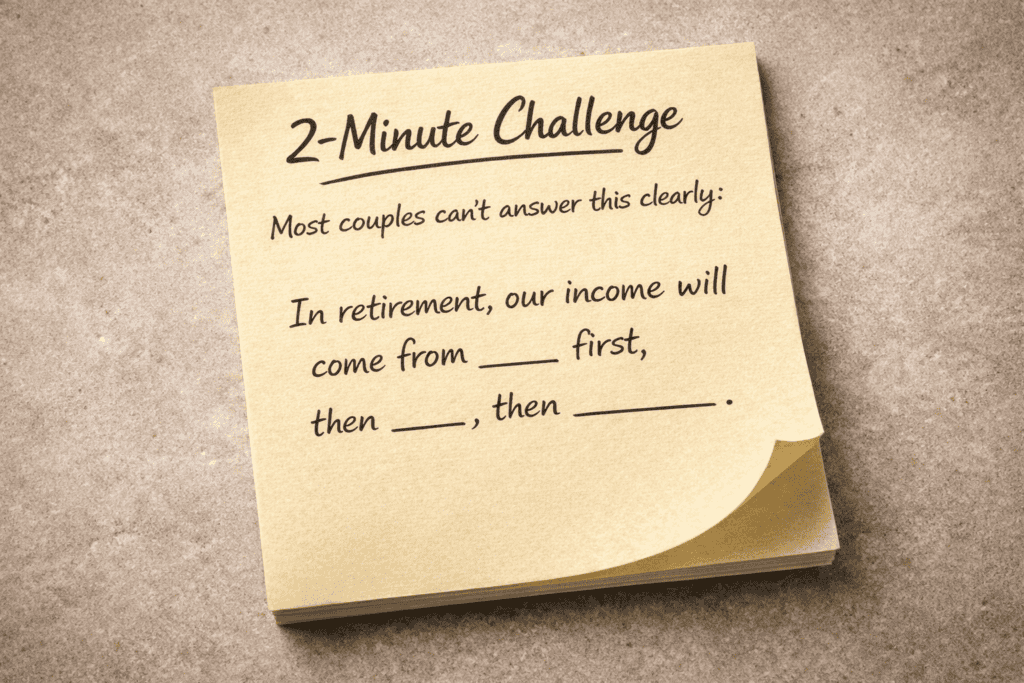

2-minute challenge

Open your notes app and answer this in one sentence:

“In retirement, our income will come from ______ first, then ______, then ______.”

If you can’t fill that in quickly, that’s your sign to prioritize this.

2) Healthcare Costs (Medicare + the “Gap Years”)

Why this is important

Healthcare is one of the biggest retirement wildcards.

Fidelity’s 2025 estimate says a 65-year-old couple may spend about $330,000 (after tax) on health care in retirement (costs like premiums, copays, and out-of-pocket expenses).

Even Medicare isn’t “free.” CMS announced the standard Medicare Part B premium for 2026 is $202.90/month (with higher costs for higher-income households due to IRMAA).

How to fix it

- If you might retire before 65: map the coverage plan for ages 57–65

- Track income carefully because Medicare surcharges (IRMAA) are based on MAGI (often from two years prior)

- Build a “healthcare buffer” line item into retirement income planning

Quick test

Ask each other this:

“If one of us retired in the next 2–5 years, what would we do for health insurance until Medicare?”

If the answer is “We’re not sure,” that’s a planning opportunity, not a problem.

3) Inflation (The Quiet Budget Killer)

Why this is important

Inflation doesn’t feel dramatic week-to-week. It compounds year after year.

A simple way to think about it: if prices rise over time, your retirement paycheck must rise too—or your lifestyle slowly shrinks. The CPI data from the Bureau of Labor Statistics tracks this long-term rise in consumer prices.

How to fix it

- Separate “must-pay” expenses from “nice-to-have” spending

- Build a plan where your income can adjust with inflation (not just a fixed number)

- Keep a strategy for “inflation protection” (often through a mix of growth assets + flexible spending rules)

Simple check

Write down two numbers:

- Your monthly must-pay expenses (housing, utilities, insurance, food)

- Your monthly choice expenses (travel, hobbies, gifts)

This one step makes inflation planning 10x easier.

4) Taxes Over Time (Not Just This Year)

Why this is important

Many retirement taxes don’t show up until later.

Social Security can surprise people: the Social Security Administration projects about 56% of beneficiary families will owe federal income tax on their benefits. And the IRS notes that up to 85% of benefits may be taxable depending on income.

Also, Medicare premiums can rise with income (IRMAA), so tax planning and healthcare costs are connected.

How to fix it

- Create a simple “tax map” of your future income sources (pre-tax, Roth, taxable)

- Plan for “tax spikes” later (like RMD years)

- Consider whether spreading income over time reduces taxes and Medicare surcharges

Fast action

Answer this quickly:

“Most of our retirement savings is in: Pre-tax / Roth / Taxable (pick one).”

If it’s mostly pre-tax, tax planning deserves extra attention.

5) Coordination (Including Beneficiaries) — The Support Beam

Why this is important

Beneficiaries shouldn’t be the whole story—but they are a perfect example of how plans drift.

Many assets transfer by beneficiary forms, not by a will or trust. And many people haven’t updated those forms in years (especially after major life changes).

This isn’t just paperwork. In real life, poor coordination creates delays, confusion, and stress—usually at the worst time.

How to fix it

- Make a list of your “big accounts” (401(k), IRA, life insurance, brokerage)

- Confirm beneficiaries are correct and consistent with your current wishes

- Make sure both spouses know where documents are and who to call

- Schedule an annual “account review” together every January

One question

Ask each other:

“If something happened to me, would you know where our accounts are and who to call first?”

If not, start a shared note titled: “If Something Happens” and add one name and one phone number today.

The 60-Second Wrap-Up

If you only remember one thing:

Retirement confidence isn’t built by predicting markets. It’s built by reviewing decisions before they become permanent.

You don’t need to tackle all five areas today. But you do need to start.

That’s why I created a simple one-page checklist that walks you through exactly what to review, what questions to ask, and what to do if you find a gap.

👉 Get the January Pre-Retirement Planning Checklist

Many couples complete it together in about 20 minutes—and walk away either feeling confident everything’s aligned, or knowing exactly what needs attention next.

Either way, you’ll sleep better.

P.S. — If you go through the checklist and realize something needs professional attention, we’re here to help. But start with the checklist first. You might be in better shape than you think—or you’ll know exactly what needs fixing.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.