You’ve built a successful career and accumulated significant wealth, but lately, you’ve been feeling pulled in two directions.

Your mother calls about her Medicare supplement costs—$800 a month that’s stretching her fixed income. Your daughter needs help with grad school expenses. Meanwhile, your latest retirement planning projection shows you’re falling behind on your savings goals.

Sound familiar? You’re not alone in this sandwich generation financial dilemma.

The Financial Impact on the Sandwich Generation Supporting Family

If you’re in your 50s or 60s and find yourself financially supporting both aging parents and adult children, your part of what financial planners call the “sandwich generation.” And while your intentions are admirable, you might be making a costly retirement planning mistake that could derail your own financial future.

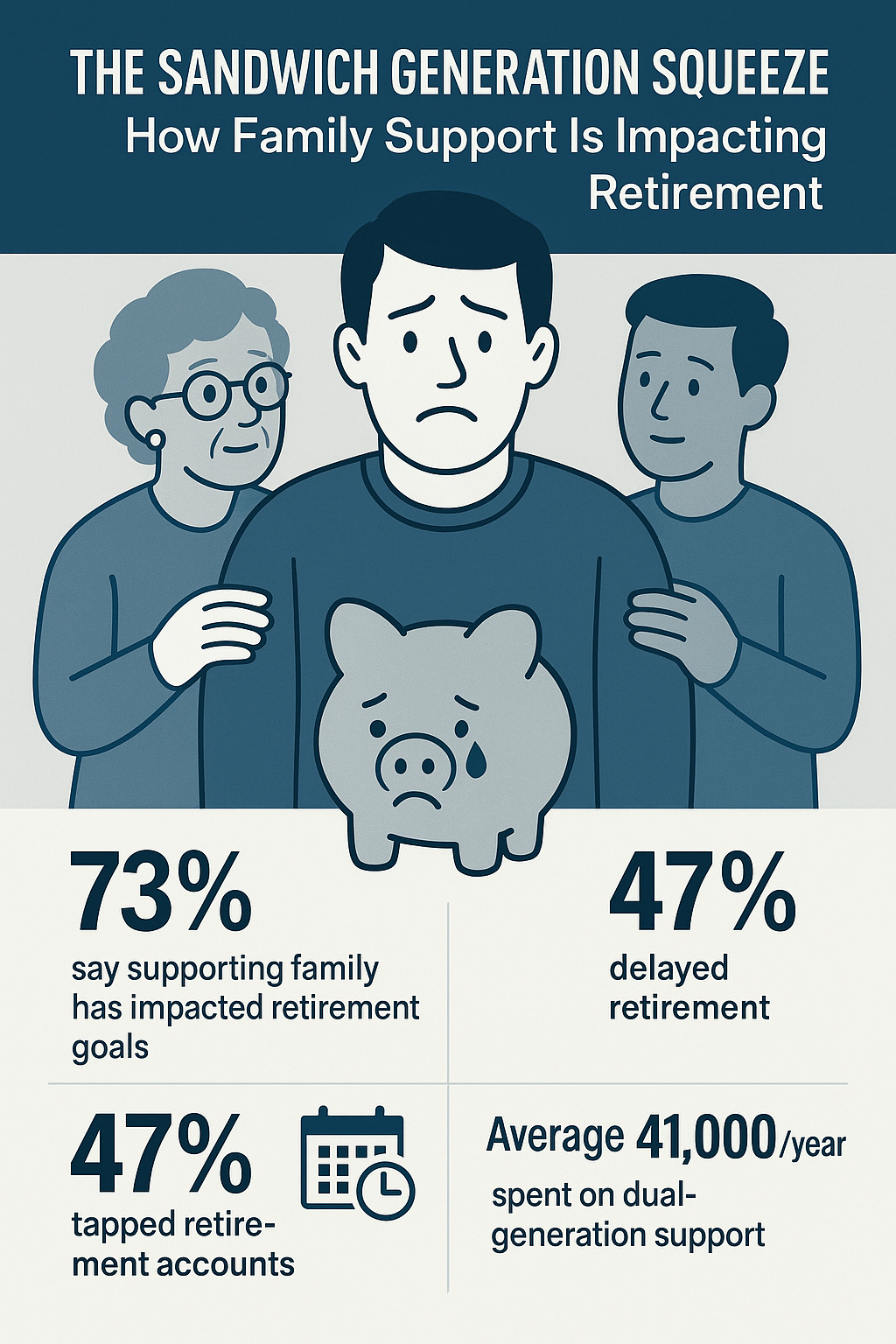

Here’s what the data shows: According to recent surveys by Athene and New York Life, 73% of sandwich generation families say supporting family has impacted their retirement goals, with 47% putting off retirement to provide financial support. Around 47% are also tapping into their retirement assets to cover these expenses.

The problem isn’t that you’re helping family. The problem is that you’re helping without a comprehensive retirement planning strategy that protects your financial future while still being the supportive parent and child you want to be.

The Real Cost of Unplanned Family Support

The numbers behind multigenerational financial support are more significant than most families realize. The average sandwich generation household spends $41,000 annually supporting both generations. Invested at a 7% return over 15 years, that’s over $500,000 in retirement wealth that never gets built.

But the hidden cost runs deeper. Consider the Pennsylvania tax implications alone. If you’re earning $200,000 annually and delay retirement by three years, you’re paying an additional $18,000 in state income taxes while missing out on tax-free retirement withdrawals. Pennsylvania doesn’t tax retirement income from 401(k)s, IRAs, or pensions—making every dollar saved today worth 3.07% more in retirement.

Strategic Retirement Planning Framework for Sandwich Generation Families

High Net Worth Families Building Wealth (Under $2 Million Net Worth)

The key to successful sandwich generation retirement planning is establishing what we call the “Priority Pyramid.” Your retirement planning foundation must be secure before you can effectively help others long-term.

Start with 401k retirement planning basics: maximize your employer match and contribute at least 15% of gross income. This isn’t negotiable—it’s the foundation that prevents you from becoming a financial burden on your children later.

Next, create a dedicated family assistance fund with $50,000-$100,000. This serves two purposes: it provides immediate help when needed and creates a psychological barrier against raiding retirement accounts for family emergencies.

Finally, leverage Pennsylvania retirement tax advantages. Every dollar you save now avoids current state taxes and grows tax-free for retirement withdrawals.

High Net Worth Families Preserving Wealth (Over $2 Million Net Worth)

Wealth management strategies for higher net worth families include more sophisticated tools. The annual estate planning gift tax exclusion of $17,000 per person ($34,000 for married couples) allows you to support family members while reducing your taxable estate. For a family with four adult children, that’s potentially $136,000 in annual gifts.

Consider establishing a family bank structure—formal loan arrangements for major purchases like homes or business investments. This keeps family money within the family while maintaining appropriate boundaries and expectations.

Multigenerational trusts offer the ultimate flexibility in wealth preservation, protecting assets while allowing for family support as circumstances change over time.

Retirement Planning Strategies for Sandwich Generation Success

1. The 50/30/20 Family Financial Planning Rule

For family support expenses, allocate 50% for immediate needs (like Medicare supplements), 30% for planned expenses (education costs), and 20% for emergencies. This prevents emotional overspending while ensuring adequate support without derailing your retirement planning goals.

2. Pennsylvania Long-Term Care Planning Strategy

With nursing home costs averaging $108,000 annually in Pennsylvania, hybrid life insurance policies with long-term care benefits often provide better value than traditional long-term care insurance. They protect your retirement savings from healthcare expenses while providing death benefits if care isn’t needed.

3. Strategic Education Funding for Wealth Preservation

Helping your child through grad school? Research shows that 69% of students whose parents help financially finish their degrees, compared to just 43% who don’t get that support.

But be careful not to sacrifice your own future. A good rule of thumb is to limit education contributions to no more than 10% of your gross income to stay on track for retirement.

If you’re a Pennsylvania resident, consider using a 529 plan—you can deduct up to $15,000 per beneficiary per year from your state taxes.

30-Day Sandwich Generation Retirement Planning Action Plan

Week 1: Financial Assessment Calculate your actual monthly family support expenses. Many families underestimate by 30-40%. Verify you’re saving at least 15% for retirement planning. Review your parents’ long-term care coverage.

Week 2: Financial Structure Open a separate family assistance account. Set an annual family support limit of 10-15% of gross income. Research Pennsylvania 529 tax benefits if education funding is a priority.

Week 3: Tax Optimization Maximize 401k contributions to reduce Pennsylvania taxes. Consider Roth conversions in lower-income years. Update estate planning documents to reflect your multigenerational strategy.

Week 4: Family Communication Hold a family financial planning meeting. Set clear long-term expectations. Establish a decision-making process for major requests. This prevents crisis-driven financial decisions.

Essential Questions for Your Financial Advisor About Sandwich Generation Planning

When discussing sandwich generation financial planning with your wealth management advisor, ask these critical questions:

“How do we model different family support scenarios without derailing our high net worth retirement planning timeline?”

“What’s the most tax-efficient way to help adult children while maximizing Pennsylvania retirement tax advantages?”

“Should we consider long-term care insurance now as part of our comprehensive financial plan?”

“How do we balance current family needs with estate planning and wealth transfer strategies?”

What Those in the Sandwich Generation Should Do for Retirement Planning

The sandwich generation financial planning challenge doesn’t have to squeeze out your retirement dreams. The families who navigate this successfully understand that securing their own retirement planning isn’t selfish; it’s essential. A financially secure retirement means you won’t become a burden on your children later.

The real question isn’t whether you can afford to help your family. It’s whether you can afford not to plan for multigenerational financial support properly.

Your financial future doesn’t have to be derailed by family obligations. By creating an integrated retirement planning strategy that acknowledges your responsibilities while protecting your wealth, you can be both a supportive family member and a financially secure retiree.

The sandwich generation squeeze is real, but it doesn’t have to compromise your retirement planning goals. The key is creating a comprehensive financial plan that honors your family values while ensuring your financial independence.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.