You have a number in your head. A retirement age. Maybe 62.

Key Takeaways

- Healthcare costs for couples before Medicare can reach ,000-,000 over three years in premiums alone

- Drawing from Roth accounts instead of traditional 401(k)s can qualify you for ACA subsidies

- HSA funds can reimburse medical expenses years later with no time limit on reimbursements

- COBRA typically costs 2-3x more than employer coverage and only lasts 18 months

- Calculate your healthcare gap now by getting quotes at healthcare.gov for your retirement timeline

Maybe 63. You have been working toward it for a long time and you are close enough to feel it.

Then someone mentions what health insurance costs when your employer stops paying for it. And the number stops you cold.

This is not a rare conversation. According to the Employee Benefit Research Institute, half of Americans retire earlier than they planned to. The median retirement age in the United States is 62.

That means for most people, the gap between the last day of work and the first day of Medicare at 65 is not a choice. It is a reality that arrives before they are ready for it.

New research from the LIMRA Retirement Income Institute published in April 2026 found that healthcare costs rank as Americans’ top financial concern in retirement. Above market crashes. Above inflation.

Above recessions. And yet only 23% of Americans have ever discussed healthcare costs in retirement with a financial advisor, according to a D.A. Davidson survey.

This article covers what health insurance before Medicare actually costs, why the most common solution is often the wrong one, and two strategies that may help change the math in a meaningful way.

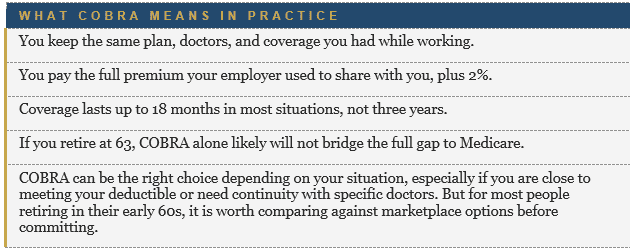

COBRA: The Option Everyone Thinks of First

When people think about health insurance before Medicare, COBRA is usually the first thing that comes to mind. It is worth understanding what it actually is before deciding whether it is the right fit.

COBRA allows you to keep your employer’s health plan after you leave your job. The coverage stays the same. The problem is the price.

While you were working, your employer likely paid the majority of your monthly premium. Under COBRA, you pay all of it yourself, plus a 2% administrative fee.

For many families, that means a bill that doubles or triples overnight. COBRA also has a time limit of up to 18 months in most cases. If you retire at 63, it may not carry you all the way to Medicare at 65.

How Much Does Health Insurance Actually Cost Before Medicare?

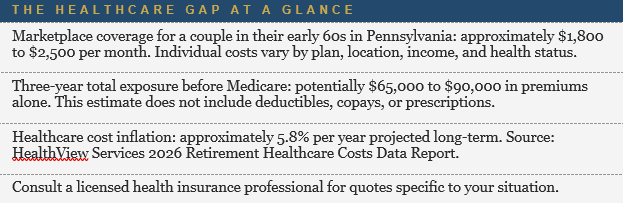

Even if COBRA is available to you, it is worth understanding what the full healthcare gap may actually cost over three years before settling on any one approach.

For a couple in their early 60s in Pennsylvania, marketplace health insurance can run between $1,800 and $2,500 per month for solid coverage. That is between $21,600 and $30,000 per year in premiums alone. Over three years before Medicare starts, the total exposure may be $65,000 to $90,000.

That does not include deductibles, copays, or prescriptions. Just the monthly bill to have coverage at all.

That number almost never appears in a retirement plan. And for families who built their timeline around retiring at 62, discovering it at 61 does not leave many good options.

Healthcare costs are also rising faster than most people’s income. According to HealthView Services’ 2026 Retirement Healthcare Costs Data Report, healthcare inflation is projected at approximately 5.8% per year over the long term. The Social Security COLA for 2027 is currently projected at 2.4%. That gap between what healthcare costs and what income grows does not close on its own.

The ACA Subsidy Strategy Most Early Retirees Do Not Know About

Here is what surprises most people. The amount you pay for marketplace health insurance is not fixed. It depends on your income. And in retirement, you often have more control over your reported income than you ever did while working.

Under the Affordable Care Act, households whose income falls below certain levels may qualify for subsidies that bring the monthly premium down meaningfully. In some cases, dramatically.

A 60-year-old couple with an annual income of $85,000 paid an average of approximately $7,225 for marketplace insurance in 2025, according to the Center on Budget and Policy Priorities. Without those subsidies, the same coverage would have cost approximately $31,762 for that specific income and household scenario. That is a difference of roughly 340%.

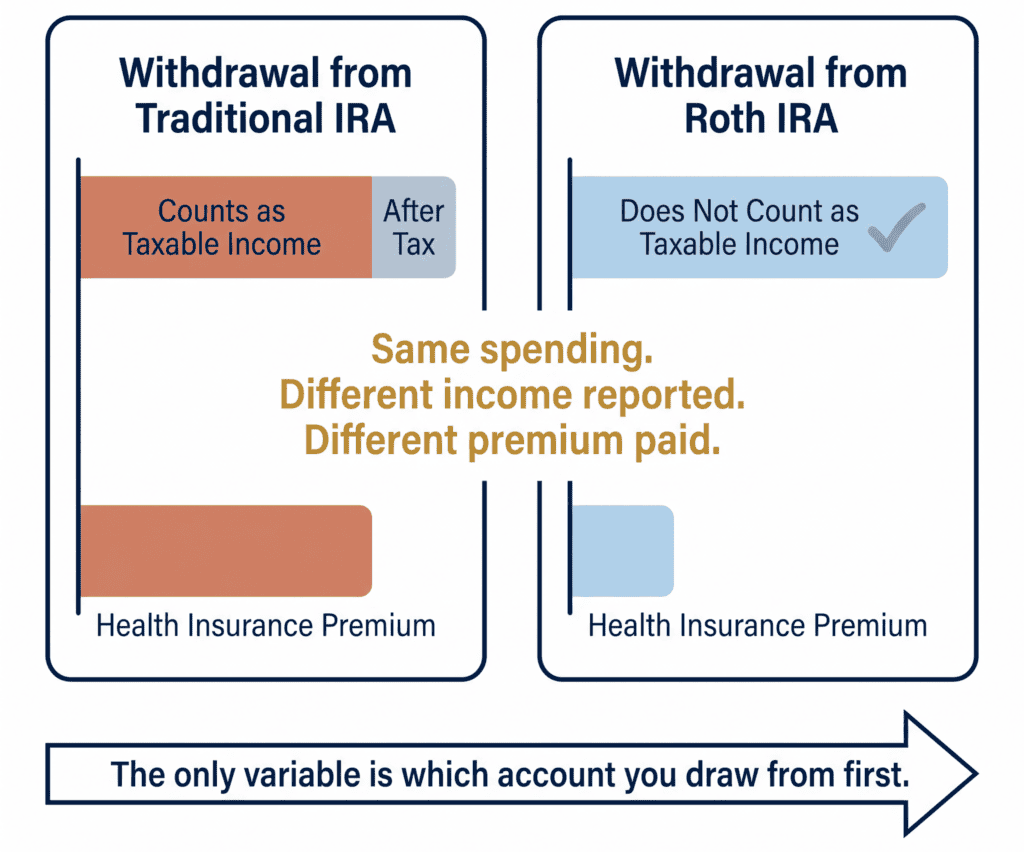

Same couple. Same plan. Different income reported.

Note that subsidy amounts vary significantly by household size, income, location, plan selected, and applicable law, which is subject to legislative change. The 340% figure represents one specific scenario and is not typical of all situations.

That statistic is worth sitting with. This is not a program designed for low-income households. It is a program that most people who shop on the marketplace benefit from, including retirees with substantial savings.

ACA subsidy rules are also subject to change by Congress. The current framework has been modified multiple times since 2010. Any strategy that depends on subsidy eligibility should account for the possibility that the rules may look different in future years.

Why the Account You Draw From First Changes Everything

Your ACA subsidy is based on your modified adjusted gross income, or MAGI. Think of it as your taxable income for the year.

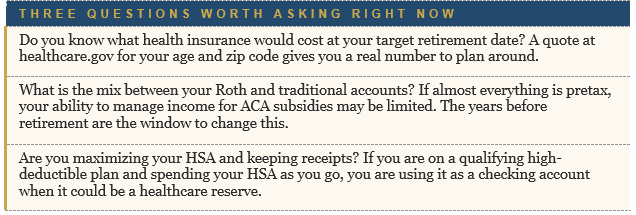

In retirement, you have choices about where your income comes from. Those choices directly affect your MAGI and, in turn, your subsidy eligibility.

Managing which account you tap first is called withdrawal sequencing.

Done thoughtfully, it may allow a couple with a mix of account types to report lower taxable income while still meeting their spending needs. That lower income may qualify them for meaningful ACA subsidies during the gap years before Medicare.

In 2026, a married couple filing jointly with a modified adjusted gross income below approximately $79,000 may qualify for premium assistance, though the exact threshold varies by household size and adjusts annually based on federal poverty level guidelines. Individual results vary based on income, family size, plan selection, and other factors that change annually. This is not a one-size-fits-all strategy, which is exactly why it benefits from a planning conversation tailored to your situation.

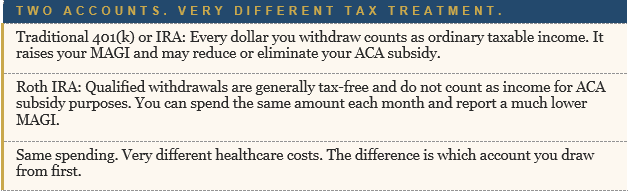

What If Most of My Savings Are in a Traditional 401(k)?

This is one of the most common follow-up questions. Many people in their late 50s have most of their savings in pretax accounts like a traditional 401(k) or IRA. If that is your situation, almost every dollar you withdraw in retirement will count as taxable income. Your flexibility to manage MAGI is limited.

There is a way to address this over time. It is called a Roth conversion. Each year, you convert a portion of your traditional account to a Roth.

You pay taxes on the amount converted in the year you do it. That is a real upfront cost, and whether it makes sense depends on your current tax bracket, your projected income in retirement, and how many years you have before you retire.

The key point is that this decision needs to happen before retirement, not after. Converting while you still have working income gives you the most flexibility. Once you have retired, the opportunity may still exist, but the window to build meaningful Roth balances before Medicare eligibility becomes much shorter.

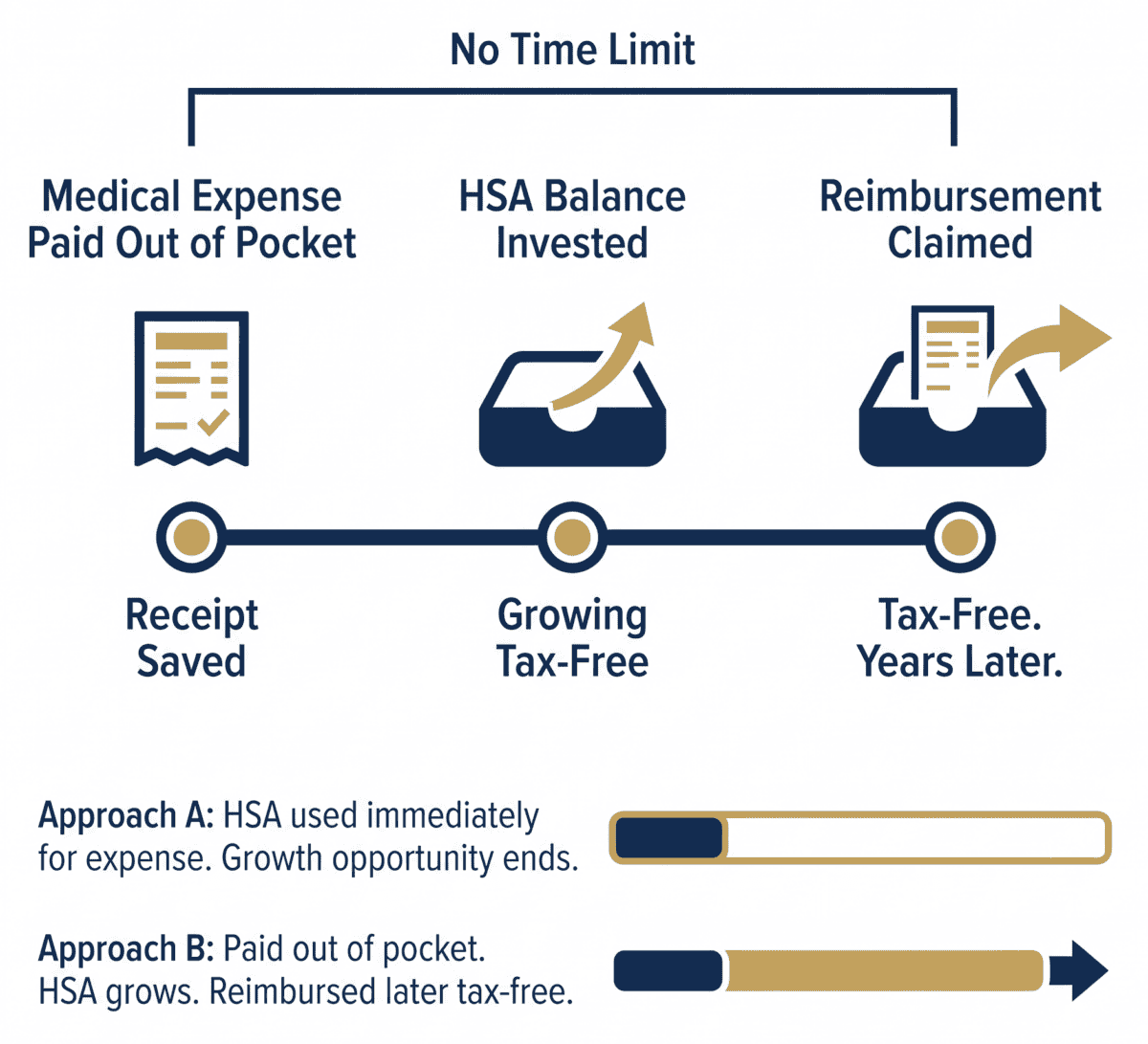

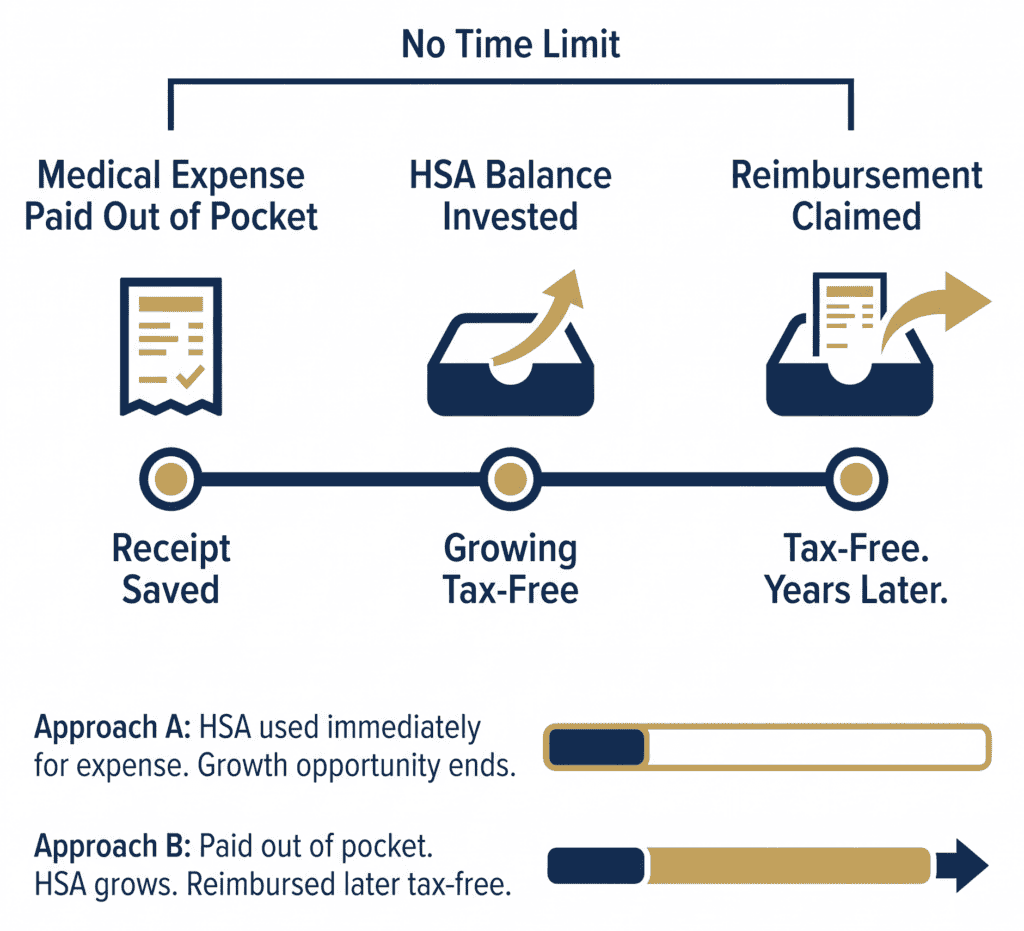

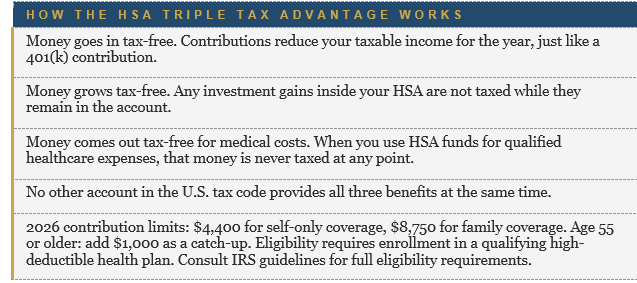

The HSA: The Account Built for This Exact Problem

There is a second strategy that addresses the healthcare gap from a completely different angle. And most people who could use it already have access to the account it requires.

The Health Savings Account, or HSA, is available to people enrolled in a qualifying high-deductible health plan. If you have one of those plans right now, you can contribute to an HSA. If you are using it mainly to cover this year’s copays and bills, you are likely leaving its most powerful benefit unused.

📅 Questions about managing your retirement accounts to potentially qualify for ACA subsidies? Book a 20-minute Retirement Income Strategy call to explore whether withdrawal sequencing makes sense for your account mix and timeline. No cost—just clarity on your options.

The Triple Tax Advantage

The HSA is the only account in the U.S. tax code that gives you three tax benefits at the same time.

The Reimbursement Strategy Most People Have Never Heard Of

Here is what makes the HSA different from almost every other account. There is no time limit on HSA reimbursements.

You can pay a medical expense out of pocket today, save the receipt, and reimburse yourself from your HSA months or years later. While you wait, your HSA balance keeps growing tax-free. When you pull the money out later to reimburse yourself, it comes out completely tax-free.

Done consistently, this approach may help build a meaningful healthcare reserve over time. It requires discipline and careful record-keeping. The IRS requires documentation for every expense you plan to reimburse, and claims without proper receipts can be questioned or disallowed. Keep receipts organized in a dedicated folder or digital file as you go, not retroactively.

One Important Rule to Know

Once you enroll in Medicare at 65, you can no longer make new contributions to your HSA. This is a hard deadline. If building your HSA before Medicare starts is part of your plan, contributions must stop when Medicare coverage begins.

The money already in the account remains available. After age 65, HSA withdrawals for qualified medical expenses, including Medicare premiums, dental, vision, and hearing costs, remain tax-free for life. Withdrawals for non-medical purposes are taxed as ordinary income, similar to a traditional IRA.

What This Looks Like for a Real Family

Hypothetical scenario for illustration purposes only. Individual results will vary significantly based on account balances, income sources, household size, plan selection, subsidy eligibility, and other factors. This example does not represent actual client results and should not be interpreted as a projection of specific outcomes.

Meet Tom and Linda. Tom is 62 and Linda is 61. They live in central Pennsylvania.

Tom worked in corporate management for 28 years. Linda worked part-time for much of their marriage and returned full-time in her 50s. They have saved consistently but most of their retirement savings sit in traditional 401(k) accounts.

When they first thought about retiring at 63, their healthcare plan was simple. They would use COBRA for a year and then figure out the marketplace. Nobody had told them what the marketplace would cost for a couple their age, or that their MAGI would determine how much they paid.

After a planning review, two things changed. First, they discovered that by drawing primarily from a small Roth account Tom had built in his early 50s, and keeping other taxable income low, their projected MAGI might fall within a range that qualified for meaningful subsidy assistance. The monthly premium estimate dropped considerably from what they had assumed.

Second, Linda had an HSA through her employer plan that she had been using as a spending account. After the review she shifted to paying medical expenses out of pocket and investing the HSA balance. She kept every receipt. Over two years before retirement she built a balance intended specifically for healthcare costs in the gap years.

The point is not the specific numbers, which will be different for every family. The point is that two people who assumed the healthcare gap was a fixed cost discovered it was actually a planning variable. One that had looked very different before they understood the tools available to them.

How the Two Strategies Create Something Neither Does Alone

Withdrawal sequencing may reduce what you pay for marketplace insurance by keeping your taxable income within a range that qualifies for subsidy assistance. The HSA may build a tax-free reserve that covers the out-of-pocket costs insurance does not pay.

Here is the key insight: they work on different parts of the problem. Withdrawal sequencing works on the monthly premium. The HSA works on what you pay after the premium. Together they address both sides of the healthcare gap in a coordinated way that neither strategy achieves on its own.

Both require decisions made before retirement. Your account mix determines whether withdrawal sequencing is available to you. Your HSA balance depends on years of contributions you cannot compress into a single year. The window to act on both is now, not the morning of your last day of work.

The One Number That Belongs in Your Retirement Plan

Go to healthcare.gov and run a quote for your age, zip code, and household size. Look at a silver plan. Write down the monthly premium. Multiply it by the number of months between your target retirement date and your 65th birthday.

That is your healthcare gap number. Put it next to your retirement savings number. If it has never appeared in your plan before, now you know why this article exists.

The families that retire with genuine confidence are not the ones who had the easiest circumstances. They are the ones who found the missing numbers while they still had time to do something about them. For many people, the healthcare gap is the biggest missing number in their entire plan.

The strategies to address it may be available to many people in their 50s and early 60s, depending on their individual situation. But they require time to work. The right moment to explore them is well before the retirement date is set.

ABOUT THE FINANCIAL PLANNING AUTHOR

Alexander Langan, J.D., CFBS

Alexander Langan, J.D., CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual and Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

ABOUT LANGAN FINANCIAL GROUP: FINANCIAL ADVISORS

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, PA.

With over 150 five-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice. Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC. Investment Advisor Representative, Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor.

Cambridge and Langan Financial Group, LLC are not affiliated. Cambridge does not offer tax or legal advice. All hypothetical examples are for illustration purposes only and do not represent actual client results.

Past performance does not guarantee future results. Individual results will vary. ACA subsidy eligibility depends on household income, family size, plan selection, applicable federal poverty level guidelines, and other factors that are subject to annual change and potential legislative modification.

HSA eligibility requires enrollment in a qualifying high-deductible health plan as defined by IRS guidelines. HSA contribution limits are for the 2026 tax year and are subject to change. Roth IRA distribution rules are subject to IRS regulations and individual circumstances.

Roth conversions may increase taxable income in the year of conversion and should be evaluated with a qualified tax professional. HSA reimbursements require proper documentation and receipts as required by IRS rules. ACA subsidy and premium data sourced from the Center on Budget and Policy Priorities and Vanguard.

Healthcare cost inflation data sourced from HealthView Services 2026 Retirement Healthcare Costs Data Report. Lifetime healthcare cost data sourced from Fidelity Investments 2025 Retiree Health Care Cost Estimate. Consumer research data sourced from LIMRA Retirement Income Institute April 2026 and D.A.

Davidson. Retirement age data sourced from the Employee Benefit Research Institute. This article must be reviewed and approved by a qualified registered principal prior to use as a retail communication under FINRA Rule 2210.