Healthcare costs represent one of the biggest financial risks in retirement, yet most people dramatically underestimate how much they’ll spend on medical care.

While you’re planning for travel, hobbies, and leisure activities in retirement, healthcare expenses are quietly growing into what could become your largest expense category.

Understanding and preparing for these costs now can mean the difference between a comfortable retirement and financial stress when you’re most vulnerable.

The Shocking Reality of Healthcare Costs

According to recent studies, the average healthy 65-year-old couple retiring today will spend approximately $300,000 on healthcare costs throughout their retirement. This figure doesn’t include long-term care, which could add hundreds of thousands more to the total.

To put this in perspective, if you’re 50 years old today and planning to retire at 65, healthcare costs alone might require you to save an additional $20,000 per year just to cover medical expenses. That’s separate from all your other retirement needs like housing, food, and lifestyle expenses that are part of comprehensive financial planning.

These costs continue to rise faster than general inflation. While overall prices might increase by 2-3% annually, healthcare costs have historically grown by 4-6% per year. This means healthcare will likely consume an increasingly large portion of your retirement income as you age.

What Medicare Does and Doesn’t Cover

Many people assume Medicare will cover most of their healthcare costs in retirement. While Medicare is invaluable, it has significant gaps that can leave you with substantial out-of-pocket expenses.

Medicare Part A covers hospital stays but comes with deductibles and co-insurance. For 2025, the Part A deductible is $1,632 per benefit period, and you’re responsible for co-insurance costs for extended stays.

Medicare Part B covers doctor visits and outpatient care but requires monthly premiums, an annual deductible, and 20% co-insurance on most services. The standard Part B premium for 2025 is $185 per month, but high-income earners pay significantly more.

Medicare Part D covers prescription drugs but has its own premiums, deductibles, and the infamous “donut hole” where you pay more out-of-pocket for medications until you reach catastrophic coverage levels.

What Medicare Doesn’t Cover: Dental care, vision care, hearing aids, and most long-term care services aren’t covered by traditional Medicare. These exclusions can result in thousands of dollars in annual expenses.

The Long-Term Care Challenge

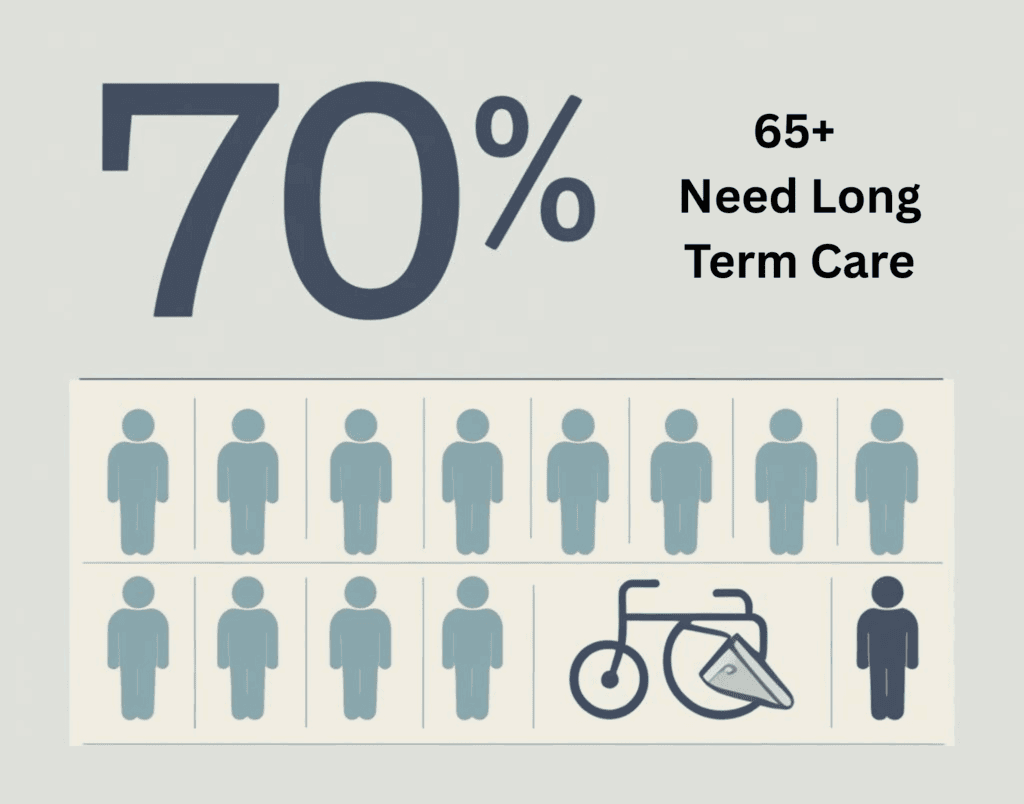

Long-term care represents the largest potential healthcare expense in retirement, yet it’s the one most people ignore in their planning. The statistics are sobering: about 70% of people over age 65 will need some form of long-term care during their lifetime.

The costs are substantial. A private room in a nursing home averages over $100,000 per year nationally, with costs much higher in expensive areas. Even home care can cost $60,000-$80,000 annually for full-time assistance.

Medicare provides very limited long-term care coverage, typically only for short-term skilled nursing care following a hospital stay. Medicaid will cover long-term care costs, but only after you’ve spent down most of your assets. This “spend-down” requirement can devastate a surviving spouse’s financial security.

Healthcare Cost Categories to Plan For

Understanding where your healthcare dollars will go helps in planning:

Insurance Premiums: Even with Medicare, you’ll likely need supplemental coverage (Medigap) or Medicare Advantage plans. These can cost $200-$500 per month per person, depending on the coverage level you choose.

Out-of-Pocket Medical Expenses: Deductibles, co-pays, and co-insurance add up quickly. Even with good insurance, you might spend $3,000-$6,000 annually on these costs.

Prescription Drugs: Medication costs can be substantial, especially for chronic conditions. Some specialty drugs cost thousands of dollars per month, even with insurance coverage.

Dental and Vision Care: These “extras” can easily cost $2,000-$4,000 per year per person for routine and emergency care.

Long-Term Care: Whether it’s home care, assisted living, or nursing home care, these costs can quickly consume your entire retirement.

Strategies to Manage Healthcare Costs

While you can’t eliminate healthcare costs in retirement, you can take steps to manage and plan for them:

Health Savings Accounts (HSAs): If you’re eligible, HSAs offer a triple tax advantage for healthcare costs. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

After age 65, you can withdraw funds for any purpose (paying ordinary income tax), making HSAs excellent retirement accounts. This is a key component of tax-efficient investing strategies.

Stay Healthy: The best way to control healthcare costs is to stay as healthy as possible. Regular exercise, a healthy diet, preventive care, and managing chronic conditions can reduce your long-term healthcare expenses significantly.

Medicare Supplement Planning: Research Medicare supplement options before you turn 65. During your initial enrollment period, you can’t be denied coverage for pre-existing conditions. Waiting can result in higher premiums or coverage denials.

Long-Term Care Insurance: Consider purchasing long-term care insurance while you’re healthy and in your 50s or early 60s. Premiums are much lower when you’re younger, and you’ll have better coverage options.

Geographic Considerations

Where you retire can dramatically impact your healthcare costs. Some factors to consider:

Cost of Living: Healthcare costs vary significantly by region. The same procedure might cost twice as much in New York City as in rural Alabama.

Medicare Advantage Availability: Some areas have many Medicare Advantage options with competitive benefits, while others have limited choices.

Quality of Care: Consider the availability and quality of healthcare providers, especially specialists you might need for ongoing conditions.

State Medicaid Programs: If long-term care becomes necessary, some states have more generous Medicaid programs than others.

Planning Timeline: When to Start Preparing

The earlier you start planning for healthcare costs, the more options you’ll have:

In Your 40s and 50s: This is the ideal time to maximize HSA contributions, purchase long-term care insurance, and establish healthy lifestyle habits. You have time to save specifically for healthcare costs and can take advantage of compound growth.

In Your 60s: Focus on understanding Medicare options and planning your transition from employer health insurance. If you haven’t already, consider long-term care insurance, though premiums will be higher.

Approaching 65: Research Medicare plans available in your area, understand the enrollment timeline to avoid penalties, and consider working with a Medicare specialist to optimize your coverage.

The Role of Health Savings Accounts

HSAs deserve special attention in healthcare planning. For 2025, you can contribute $4,300 for individual coverage or $8,550 for family coverage if you’re under 55. Those 55 and older can contribute an additional $1,000 as a catch-up contribution.

The key to maximizing HSAs is to pay current medical expenses out-of-pocket if possible and let the HSA grow for future healthcare costs. After age 65, HSAs function like traditional IRAs for non-medical expenses, but they remain tax-free for qualified medical expenses throughout your lifetime.

Insurance Options Beyond Medicare

While Medicare is the foundation of healthcare coverage for retirees, additional insurance options can help fill the gaps:

Medigap Policies: These standardized policies help pay costs that Medicare doesn’t cover, such as co-payments, co-insurance, and deductibles.

Medicare Advantage Plans: These private plans replace traditional Medicare and often include additional benefits like prescription drug coverage, dental, and vision care.

Employer Retiree Health Plans: Some employers offer health insurance to retirees. These plans can be valuable but are becoming less common.

COBRA Coverage: If you retire before 65, you might be able to extend your employer’s health insurance through COBRA for up to 18 months, though you’ll pay the full premium.

Creating Your Healthcare Plan

When planning out your retirement expenses, healthcare should be a separate, significant category. Here’s how to approach it:

Estimate Annual Costs: Plan for $5,000-$10,000 per person annually for healthcare expenses, not including long-term care. This covers insurance premiums, out-of-pocket costs, and uncovered services.

Plan for Inflation: Healthcare costs typically rise faster than general inflation. Assume healthcare expenses will grow by 5-6% annually.

Emergency Healthcare Fund: Keep a separate emergency fund specifically for major medical expenses. This might be $25,000-$50,000 per person in easily accessible accounts.

Long-Term Care Reserve: Whether through insurance or savings, have a plan for potential long-term care costs of $100,000+ per year.

Taking Action Now

Healthcare costs in retirement are too significant to ignore or underestimate. Start by getting a realistic picture of what you might spend, then create a plan to fund these expenses.

If you’re eligible for an HSA, maximize your contributions. Research long-term care insurance options while you’re healthy. Most importantly, invest in your health now through regular exercise, proper nutrition, and preventive care.

The goal isn’t to eliminate all healthcare costs – that’s impossible. The goal is to plan for them so they don’t derail your retirement dreams. With proper planning and preparation, you can protect both your health and your wealth in retirement.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 9 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.