And Three Questions That Help You Know If You’re Doing It

Every April, thousands of families finish their tax returns and discover something unsettling. The numbers don’t make sense. Their income stayed about the same.

Key Takeaways

- One income decision creates multiple consequences – IRA withdrawals can trigger Social Security taxes and Medicare premium increases

- Your tax return reveals if income sources work together – look for unexpected tax increases or Medicare premium jumps

- Low effective tax rates in your 60s are temporary opportunities before required distributions start at 73

- Income swings of ,000+ between years suggest uncoordinated decisions that may be costing you money

- Delaying Social Security while taking large IRA withdrawals can accidentally push you into higher tax brackets

But their taxes went up. Or their Medicare premiums jumped. Or their Social Security got taxed more than they expected.

They didn’t do anything wrong. Each decision they made looked smart. But somehow, the pieces didn’t fit together.

Here’s what most people don’t realize about retirement income: when you pull one lever, three other things move.

Take money from your IRA. Your taxable income goes up. That makes more of your Social Security taxable.

That might trigger higher Medicare premiums. That changes your tax bracket. That affects whether other strategies would help.

One decision. Five consequences.

Most people don’t see this. They make good decisions about each piece. But the pieces don’t fit together.

The result looks like sabotage. But it’s not intentional. It’s structural.

This article shows you what sabotage looks like. More importantly, it gives you three questions to ask about your own return so you know whether you have this problem.

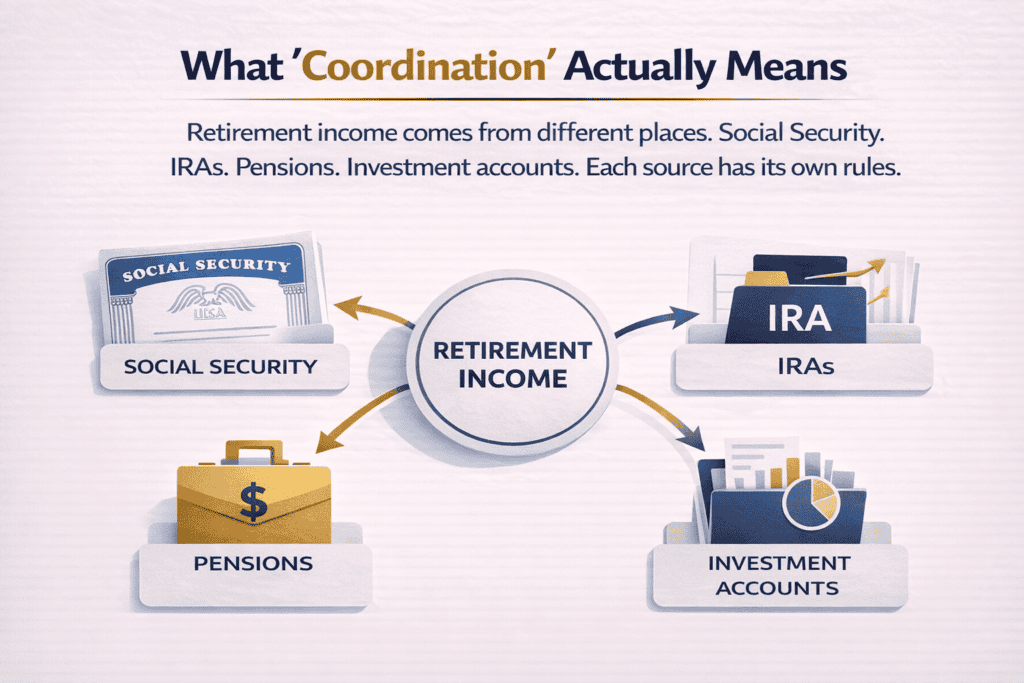

What ‘Coordination’ Actually Means

Retirement income comes from different places. Social Security. IRAs.

Pensions. Investment accounts. Each source has its own rules.

Most people manage each source separately. They follow the rules for Social Security. They follow the rules for IRAs. They follow the rules for investments.

The problem: following the rules for each piece doesn’t mean the pieces work well together.

Think of it like medicine. One prescription might be fine. Another prescription might be fine.

But take them together and they interact badly. Nobody did anything wrong. The problem is how they combine.

Retirement income works the same way. Each source can look fine on its own. But when they come together, they create problems you didn’t expect.

For retirees: Your tax return is the one place each year where you see all your income sources together. Not individually. All at once. That’s when the problems show up.

For pre-retirees: If you’re 10 years from retirement, you have time to think differently. Most retirement projections show each income source separately. Start asking how they’ll work together.

Two Ways It Goes Wrong, One Way It Goes Right

The Social Security Tax Surprise

Hypothetical scenario: A couple delays Social Security until 70. Smart move. While waiting, they take approximately $60,000 per year from their IRA. Also smart.

At 70, Social Security starts. They receive approximately $48,000 per year. They cut IRA withdrawals to approximately $30,000. Total income stays about the same.

Here’s what happened in this example: Before age 70, their taxable income was approximately $60,000. After age 70, their taxable income jumped to approximately $70,800.

Why? The IRA withdrawals pushed them over a threshold. Now 85% of their Social Security gets taxed. Two good decisions created a bad result.

The Medicare Premium Jump

Hypothetical scenario: A 68-year-old has approximately $180,000 in income. Medicare premiums are normal. She’s approximately $14,000 below the threshold where premiums increase.

In December, she sells an investment. Long-term gain of approximately $20,000. Good decision. She’s rebalancing.

Her income for the year: approximately $200,000. She crossed the threshold by approximately $6,000. In this example, her Medicare premiums could increase by roughly $1,500 per year for two years. Total potential cost: approximately $3,000.

This scenario illustrates how a $20,000 gain could trigger approximately $3,000 in extra premiums. That’s roughly 15% gone just from Medicare. Before counting regular taxes.

When Coordination Works

Hypothetical scenario: A couple retires at 62. They have approximately $900,000 in traditional IRAs. They delay Social Security until 67. For five years, they need approximately $60,000 per year to live.

They take approximately $35,000 from taxable accounts. They take approximately $25,000 from IRAs. They convert another $20,000 from traditional IRA to Roth.

Why this approach? Their total income is approximately $80,000. That keeps them in the 12% tax bracket. They’re paying 12% now to convert money that could be taxed at 22% later when required distributions start.

At 67, Social Security starts. Their IRA balance is smaller because they’ve been converting. When required distributions start at 73, the amounts are lower. They stay in lower brackets.

Over 30 years, this approach could help them keep significantly more. Not because they earned more. Because their income sources worked together instead of against each other.

Research suggests that coordinated income strategies may improve outcomes significantly over time. When income sources work together, families may be able to keep more of what they earn. When sources work in isolation, costs tend to stack up.

Why Smart People Miss This

You’re not missing this because you’re doing something wrong. You’re missing it because the system is set up that way.

Social Security has its own rules. IRAs have different rules. Medicare has different rules.

Tax brackets have different rules. Each system operates independently.

Most financial advice focuses on one system at a time. How to maximize Social Security. How to minimize IRA taxes.

How to avoid Medicare surcharges. Each topic gets its own article.

✓ Curious if you’re accidentally sabotaging your own retirement plan? Take our 5-minute Retirement Income Coordination Assessment and find out if your current strategy creates hidden tax traps, Medicare premium increases, or other costly surprises. Get your personalized results instantly and see specific areas where coordination could help.

What’s missing: how those systems interact when you’re actually using them.

Studies on investor behavior show a pattern. People make good decisions about individual pieces. But they don’t connect those decisions.

The result is like having five different GPS apps running at once. Each gives good directions. But they send you in different directions.

For retirees: Filing your return shows you what happened when all your systems came together. Most people look at it and feel either relief or stress. What they miss is the pattern of how sources interacted.

For pre-retirees: If you’re still working, you have one income source. One W-2. One set of rules.

Retirement is different. Multiple sources. Multiple rules.

Multiple interactions. Start thinking about that now.

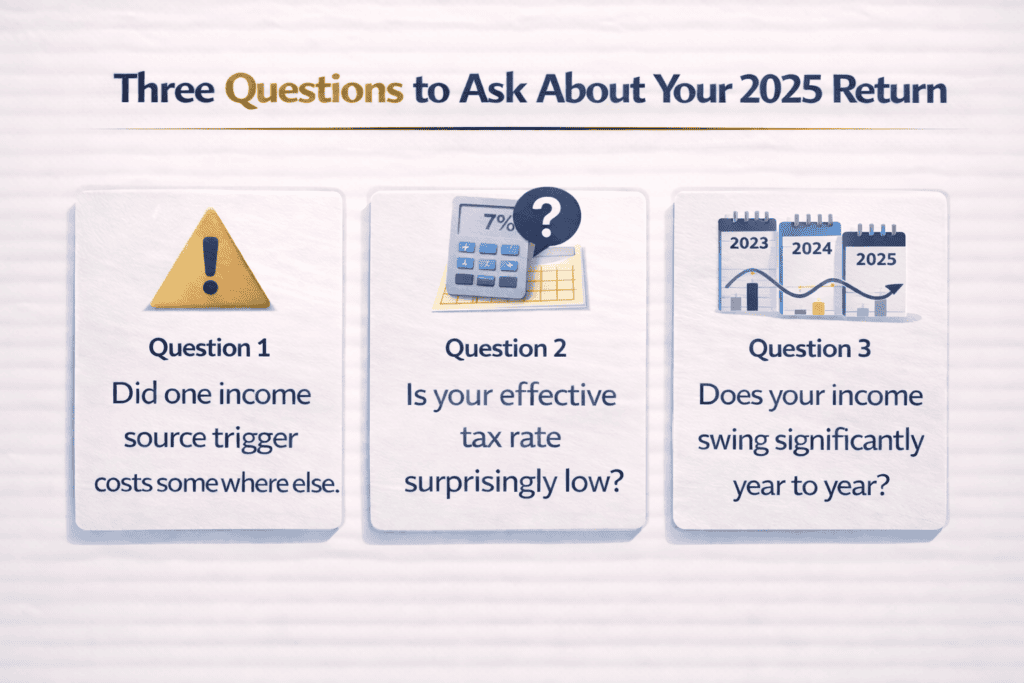

Three Questions to Ask About Your 2025 Return

Here’s how to know if your income sources are working against you. These three questions will tell you.

Question 1: Did one income source trigger costs somewhere else?

Look at your return. Did more of your Social Security become taxable this year than last year? Did your Medicare premiums go up? Did you jump into a higher tax bracket?

If yes, trace it back. What income source pushed you over? IRA withdrawals?

Investment gains? Pension payments?

This isn’t about blame. It’s about seeing the connection. One source triggered costs in another area. That’s the coordination problem.

Question 2: Is your effective tax rate surprisingly low?

Take your total federal tax. Divide it by your total income. That’s your effective rate.

If you’re retired and this number is below 12%, you’re in an unusually low-tax period. If you’re in your 60s and it’s below 15%, same thing.

Low rates aren’t bad. But they’re temporary. Once required distributions start at 73, rates usually go up. The question is whether you’re using these low-rate years strategically or just watching them pass.

Question 3: Does your income swing significantly year to year?

Compare your last three returns. Is your income within $10,000 each year? Or does it jump $20,000 or more?

Big swings without major life changes may mean decisions are being made in isolation. Maybe you took a large IRA distribution one year. Or sold investments another year.

Each decision made sense at the time. But they weren’t coordinated.

Stable income patterns suggest coordination. Volatile patterns may suggest isolation. It’s that simple.

What Good Coordination Actually Looks Like

Good coordination doesn’t mean you pay zero taxes. It means your income sources help each other instead of hurting each other.

It looks like this:

• Your Social Security taxation stays consistent year to year unless your income actually changes

• Your Medicare premiums stay predictable because you’re aware of the thresholds

• Your tax bracket is intentional, not accidental

• When you look at your return, there are no big surprises

• You’re using low-tax years strategically before distributions become required

Research suggests that families who coordinate income sources during their 60s and early 70s may keep significantly more money over 30 years. Not from better investment returns. From making sources work together.

For retirees: If your 2025 return showed coordination problems, you have eight months left in 2026. You may be able to adjust before the pattern repeats. Small changes now could help prevent costs from compounding later.

For pre-retirees: The families who retire with coordinated strategies didn’t figure it out after retirement. They built the thinking before retirement. That gives them 10-15 years of low-stress adjustments instead of reactive changes in their 70s.

The One Thing to Remember

Retirement planning isn’t just about having enough money. It’s about making sure your income sources work together when you actually start using them.

Your 2025 tax return shows you what happened last year. Look at it with one question in mind:

📅 Wondering if your income sources are working against each other like the families in this article? Schedule a 30-minute Income Coordination Review to see how your Social Security, IRA withdrawals, and other sources interact—and discover adjustments you could make before December 31st. No cost, no obligation—just clarity on whether your current approach helps or hurts your long-term plan.

Did my income sources help each other or get in each other’s way?

If the answer is ‘get in each other’s way,’ that pattern may repeat in 2026 unless something changes.

The good news: you’re not stuck. Between now and December, you may have time to adjust. The families who recognize coordination problems early may be able to address them. The families who ignore them often pay for them repeatedly over decades.

That’s the difference between accidentally sabotaging your plan and having your plan actually work.

If the three questions in this article revealed coordination problems, that may be worth addressing before 2026 repeats the pattern. We help families understand how their income sources interact and make adjustments while there’s still flexibility. A second opinion conversation can show you what your return is actually revealing.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.