Key Takeaways

- Plan for long-term care costs before a crisis forces rushed, uninformed decisions.

- Medicare does not fully cover long-term care; understand its limitations now.

- Pennsylvania’s five-year Medicaid lookback rule requires early asset protection planning.

- Long-term care insurance exists to prevent care costs from draining retirement savings.

- Families in Harrisburg, York, and Lancaster face real, specific local care costs to budget for.

Long-Term Care in Pennsylvania:

What It Costs, What Medicare Covers, and How to Protect Your Assets

A straightforward guide to one of the most common and least planned-for costs in retirement — written for families in the Harrisburg, York, and Lancaster areas.

Many readers already know this scene.

A parent who seemed fine six months ago is now in a facility. The family is scrambling. Someone is calling nursing homes and asking about availability.

Someone else is reviewing bank statements trying to figure out how long the money will last. A third person is on hold with the county assistance office, trying to understand something called a five-year lookback.

Nobody planned for this. Not because they did not love their parent. Because no one ever walked them through what it would actually cost, or what the rules actually were, before something forced the conversation.

If that scene is familiar, this article was written for you. If it is not familiar yet, the question worth sitting with is this: when it is your turn, will your children be making those same phone calls?

Long-term care is one of the most common events in retirement and one of the least planned for. This article covers what it actually costs in Pennsylvania, what Medicare does and does not cover, how Pennsylvania Medicaid rules work, what insurance costs, and how families protect their assets before a care event turns a solid retirement plan into a financial crisis.

What Long-Term Care Actually Is

Long-term care is ongoing help with basic daily activities when a person can no longer manage them independently. Those activities are defined by insurers and Medicaid alike as the six Activities of Daily Living, or ADLs:

Bathing, Dressing, Eating, Transferring (getting in and out of bed or a chair), Toileting, and Continence.

To qualify for long-term care insurance benefits, a person typically must need help with at least two of these six activities, or must have a documented cognitive impairment such as Alzheimer’s disease or dementia. That threshold matters because it defines when a policy starts paying.

Care can happen in several settings: a home health aide coming for a few hours daily, an assisted living community, a memory care unit, or a skilled nursing facility. The setting affects cost significantly. It also affects quality of life. Planning ahead gives families a say in where care happens, rather than having that choice made by a medical emergency.

Long-term care is not just a nursing home issue. It often begins at home and progresses over time. Understanding the full spectrum matters when evaluating which funding approach fits your situation.

Why More Pennsylvania Families Are Facing This

People are living longer than any prior generation. A 65-year-old in Pennsylvania today has a reasonable chance of living into their mid-80s or beyond. The longer a person lives, the more likely a care need becomes.

Federal researchers estimate that approximately 70 percent of people who reach age 65 will need some form of long-term care. One-third will never need it. But 20 percent will need it for more than five years — and women, on average, need care for 3.7 years compared to 2.2 years for men, because they tend to live longer.

Despite those odds, fewer than 1 in 10 Americans age 55 and older have purchased private long-term care insurance to help cover it, according to data from the U.S. Department of Health and Human Services. Most families are either self-funding without a plan, relying on family caregivers, or discovering the Medicaid rules when they are already inside the five-year lookback window.

20% will need it for more than five years.

Source: U.S. Department of Health and Human Services

What Medicare Actually Covers — And What It Does Not

Most people assume Medicare will cover long-term care. It will not. This is the most important fact in this article.

Medicare covers skilled nursing care, but only under specific conditions and only for a limited time. To receive any skilled nursing benefit from Medicare, a person must first have a qualifying hospital stay of at least three days. Then they must require skilled care — meaning services from a licensed nurse or therapist, not just help with daily activities.

Most long-term care needs extend well past 100 days. The average care duration for people who need it is approximately two and a half to three years. Medicare stops paying long before that. When the bill arrives after day 100, most families are not prepared.

What Care Currently Costs in Pennsylvania

Pennsylvania care costs run above the national median. Here is what families across the Harrisburg, York, and Lancaster corridor are actually paying, based on Genworth and CareScout Cost of Care Survey 2024 data and regional sources.

In the Harrisburg area, nursing home care averages approximately $10,311 per month, according to Genworth and CareScout Cost of Care Survey 2024 metro-level data. The York area runs at a comparable level, in the $10,200 to $10,400 range. The Pennsylvania statewide private room average is approximately $11,558 per month. Lancaster assisted living runs approximately $5,100 per month.

Estimates based on Genworth/CareScout Cost of Care Survey 2024–2025, Caring.com regional data, and ElderLife Financial Pennsylvania cost data. Costs are approximate and vary by provider, location, and level of care. Hypothetical 3-year totals are for planning illustration purposes only.

Apply the average care duration of two and a half to three years. At current rates, three years in a nursing home private room in the Harrisburg or York area may cost a family approximately $370,000 to $380,000. At the Pennsylvania statewide average, the estimate rises to approximately $410,000 or more.

Costs have also been rising faster than general inflation. Pennsylvania assisted living costs rose 35 percent over the past several years according to Genworth data. A plan that assumes care costs stay flat is built on an assumption that has not held.

“The bill that most often undoes a retirement plan that looked solid on paper is not the market. It is the nursing home.”

Use the free Pennsylvania Long-Term Care Readiness Worksheet included with this issue to calculate your own exposure based on your likely care setting and region.

How Much Does Long-Term Care Insurance Actually Cost?

This is the question most people ask and most articles skip. Here are the actual numbers from the American Association for Long-Term Care Insurance 2024 price index, based on a policy with $165,000 in benefits growing at 3 percent annually.

Source: American Association for Long-Term Care Insurance (AALTCI) 2024 Price Index. Premiums assume $165,000 in initial benefits with 3% annual inflation protection. Individual premiums vary based on health, coverage amount, benefit period, elimination period, and insurance carrier. These are sample estimates, not guaranteed rates.

Women pay more because they live longer and are statistically more likely to file a claim. Couples often receive a discount when both partners apply together.

Several factors determine your actual premium: the daily or monthly benefit amount, how long the benefit period lasts, the elimination period (how long you pay before the policy kicks in — typically 90 days), and whether you add inflation protection. A shorter benefit period and longer elimination period will reduce the premium significantly.

As the table above shows, premiums for the same coverage profile range from approximately $2,075 per year for a single male at age 55 to over $7,000 annually for couples at age 65. Women pay more than men at every age because they statistically live longer and are more likely to file a claim. At age 55, coverage is most accessible and least expensive. By age 65, the same coverage may cost roughly 40 to 50 percent more than at 55 — and obtaining coverage at all depends on health at the time of application.

Traditional long-term care insurance has a “use it or lose it” concern — if you never need care, the premiums are spent and there is no return of value. Hybrid policies, which combine a life insurance death benefit with long-term care coverage, address that concern. The tradeoff is a higher upfront cost, often in the form of a lump sum or limited-pay structure.

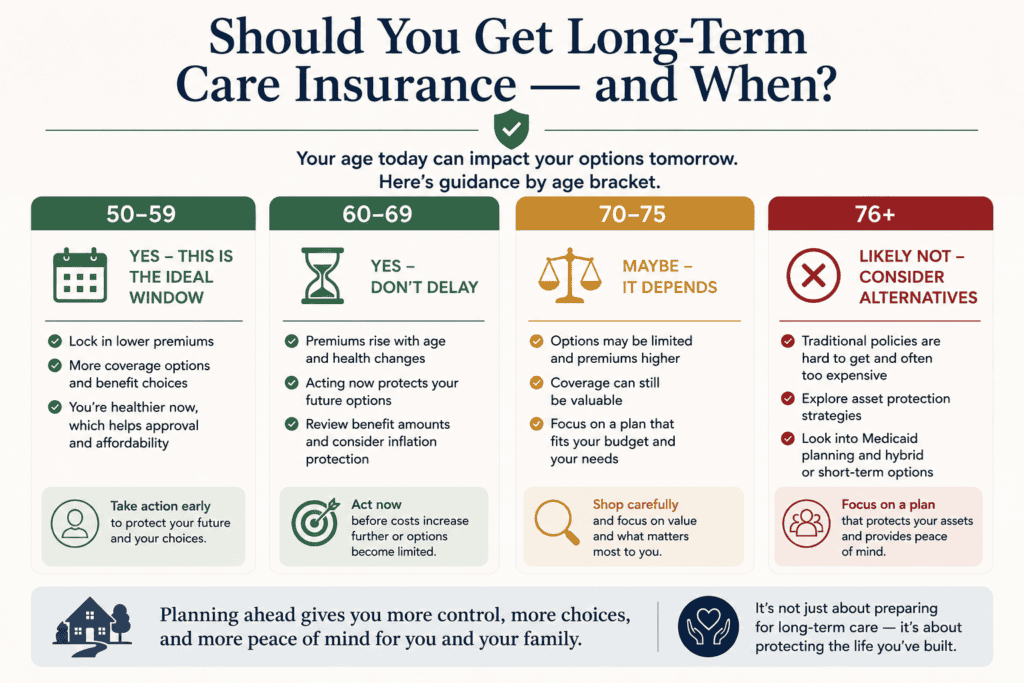

Should You Get Long-Term Care Insurance? And When?

There is no single answer, but there are clear patterns.

People who typically benefit most from a dedicated long-term care policy are those who have enough assets to lose in a care event — generally $250,000 or more in retirement savings — but not so much that they could comfortably self-fund three to five years of nursing home costs from savings alone. For households with $2 million or more in liquid assets and a sound withdrawal strategy, self-funding may be worth evaluating. For most Pennsylvania families in the $500,000 to $1.5 million range, some form of coverage or planning makes sense.

The most important factor, though, is timing. The best age to apply is in the mid-50s, according to the AALTCI. At that age, premiums are lower, health underwriting is easier, and more coverage options are available.

By the early 60s, the window narrows. By the late 60s, health issues may make approval difficult or premiums prohibitive.

Wondering how long-term care costs could affect your retirement plan? Schedule a conversation with our team to explore strategies tailored to your family’s situation — before a crisis makes the decisions for you.

Here is how the conversation should change by where you are:

In Your 50s: The Best Window Is Open

You have the most options available right now. Traditional insurance, hybrid policies, and Health Savings Account strategies are all potentially on the table. The question is not whether you will ever need care.

The question is whether you want to address this on your own terms or wait until circumstances force the conversation. Acting in your 50s typically means the lowest premiums and the best chance of qualifying.

Ages 60 to 65: The Window Is Narrowing

Traditional insurance is still available to many people in good health, but underwriting becomes more selective. Hybrid policies are worth a closer look in this range. Health Savings Account contributions can still play a bridge role if you have an HSA-eligible health plan, but that window closes at Medicare enrollment for most people. The Medicaid five-year lookback is increasingly relevant: financial decisions made now will fall within the lookback window if care is needed in the early to mid 70s.

Ages 65 and Older: Know What Is Still Available

Traditional long-term care insurance is increasingly difficult to qualify for as health conditions emerge. For people in this range, the conversation shifts toward Medicaid planning, spousal asset protection, and working with an elder law attorney who knows Pennsylvania’s specific rules. Medicaid planning is not just for people with very few assets — it is for anyone who wants to understand how Pennsylvania’s rules apply to their specific situation and what protections still exist.

If You Run Out of Options: How Pennsylvania Medicaid Actually Works

Medicaid is the government safety net for long-term care costs when personal resources are exhausted. Qualifying for it requires spending down almost everything first.

To qualify for Pennsylvania Nursing Home Medicaid as a single applicant in 2026, a person must have countable assets of no more than $8,000 and monthly income below $2,982. For a married couple where one spouse needs nursing home care, the applicant spouse may have up to $8,000 in countable assets. The spouse who remains at home is protected by Pennsylvania’s Community Spouse Resource Allowance, which allows that spouse to keep up to $162,660 in countable assets plus a monthly income allowance of up to $4,066.50 per month.

That protection exists. Most families never know it until they need it. But it comes with a critical catch.

The Five-Year Lookback: The Rule Most Families Miss

When someone applies for Medicaid in Pennsylvania, the state reviews every financial transaction from the prior 60 months. Every gift to a child. Every transfer to a family member.

Every asset moved for less than fair value. Any transfer within that five-year window may trigger a penalty.

To understand how the penalty works: Pennsylvania calculates it using a daily divisor of $421.20 for 2026. Think of that as the state’s estimate of one day of nursing home care. For every $421.20 transferred within the lookback window, Medicaid may delay coverage by one day. The family covers that time out of pocket.

A Pennsylvania resident gave an adult child approximately $50,000 four years ago. When that resident applies for Medicaid today, the state identifies the transfer. $50,000 divided by $421.20 equals approximately 118 days of ineligibility.

At current Pennsylvania nursing home rates, the family may be responsible for approximately $44,000 to $54,000 in private-pay costs before Medicaid begins. Individual results vary. This is for planning illustration only.

There is one more thing most families do not know. The IRS annual gift exclusion, which was $19,000 per person in 2026, does not protect against the Medicaid lookback. These are two entirely separate sets of rules. A gift that is perfectly legal from a tax standpoint may still create a significant Medicaid penalty.

Pennsylvania also allows gifts of up to $500 per month without penalty. But that provision is narrower than most families assume.

After a Medicaid recipient passes away, Pennsylvania may file a claim against the estate to recover costs paid. This process, called estate recovery, can affect a home left to adult children if advance planning was not completed. An elder law attorney can explain what protections remain available and when to act.

One New Tool Worth Knowing About in 2026

A provision of the SECURE 2.0 Act became effective December 29, 2025, that most people have not heard of.

Participants in certain employer-sponsored retirement plans, including most 401(k), 403(b), and governmental 457(b) plans, may now withdraw up to $2,600 per year specifically to pay premiums for a qualified long-term care insurance policy without the 10 percent early withdrawal penalty that normally applies to distributions before age 59½.

Important details before assuming this applies to you: The withdrawal is still subject to ordinary income tax. It is penalty-free, not tax-free. The amount is also capped at 10 percent of your vested account balance.

Most critically, this provision is optional for employers — your plan must be amended to allow it, and many plans have not yet done so. IRA eligibility for this provision is currently uncertain and awaiting IRS guidance. If you are considering this strategy, confirm with your plan administrator whether your plan has adopted the feature.

For someone in their 50s who is paying long-term care insurance premiums and has access to a 401(k) plan that has adopted this feature, it may offer a useful way to fund coverage from pre-tax retirement savings without penalty.

How Pennsylvania Families Protect Their Assets

There is no single strategy that fits everyone. The five approaches most commonly used in Pennsylvania are covered in detail in the companion article. In brief:

Traditional long-term care insurance works best for people in their 50s in good health who want dedicated coverage. Hybrid life and long-term care policies address the use-it-or-lose-it concern and suit people with a lump sum available. Self-funding requires significant liquid assets and a disciplined withdrawal plan.

Health Savings Accounts can serve as a limited bridge for pre-Medicare households. And Medicaid planning, with an elder law attorney, addresses asset protection for families who have not yet put other strategies in place.

The companion article — “Five Ways to Pay for Long-Term Care in Pennsylvania — and How to Know Which One Fits You” — walks through each one honestly, including who it fits, who it does not, and the four questions that help narrow down which option applies to your situation.

Three Things Worth Doing This Week

This is not a topic that benefits from waiting. Here is where to start.

Curious how Pennsylvania’s five-year Medicaid lookback rule applies to your assets? Discuss your situation with a Langan Financial Group advisor and discover approaches to help protect what you’ve built — on your timeline, not an emergency’s.

Step 1: Run your own cost estimate. Use the free Pennsylvania Long-Term Care Readiness Worksheet included with this issue. It takes approximately 15 minutes and gives you a specific number based on your likely care setting and region, not a national average.

Step 2: Check your five-year window. If you or your spouse have made significant financial gifts, transfers, or asset moves in the last five years, those transactions may be relevant to a future Medicaid application. Identifying this now leaves options open. Discovering it at application time does not.

Step 3: Have the conversation before something forces it. The families who handle long-term care best are not the ones with the most assets. They are the ones who had the conversation earlier than they needed to. If something in this article raised a question, that question is worth a 20-minute conversation with a qualified advisor before it becomes a crisis.

If you have never had a specific long-term care conversation as part of your retirement plan, we can help you start. Most conversations begin with just a few questions.

This article is for educational purposes only and does not constitute investment, tax, or legal advice. Long-term care costs are estimates and vary by provider and location. Pennsylvania Medicaid eligibility figures are current as of 2026 and subject to change.

Long-term care insurance premiums are sample estimates from AALTCI 2024 data and vary by individual health, coverage selection, and carrier. The SECURE 2.0 provision referenced applies to certain employer-sponsored plans only; IRA eligibility is pending IRS guidance; plans must opt in; distributions remain subject to ordinary income tax. Hypothetical scenarios are for illustration only.

Individual results will vary. Consult a qualified financial, legal, or tax professional before making any decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC.

Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.

-

- American Association for Long-Term Care Insurance (AALTCI), 2024 Price Index — aaltci.org

- Genworth/CareScout Cost of Care Survey 2024–2025 — carescout.com

- ElderLife Financial, Cost of Senior Care in Pennsylvania 2024 — elderlifefinancial.com

- U.S. Dept. of Health and Human Services, Long-Term Care Statistics — aspe.hhs.gov

-

- MedicaidLongTermCare.org, Pennsylvania Medicaid 2026 Eligibility — medicaidlongtermcare.org

- Medicare.gov, 2026 Medicare & You Handbook (CMS) — medicare.gov

- Centers for Medicare & Medicaid Services, 2026 Parts A & B Premiums — cms.gov

- CNBC, SECURE 2.0 Rule: 401(k) Withdrawals for LTC Insurance, Dec. 30, 2025 — cnbc.com

- TrustInsure Group, New 2026 SECURE 2.0 LTC Provision — trustinsuregroup.com

- Marshall, Parker & Weber LLC, 2026 PA Medicaid Spousal Resource & Penalty Divisor — paelderlaw.com

- Rothkoff Law Group, 2026 Medicaid Asset Limits in Pennsylvania — rothkofflaw.com

- Slutsky Elder Law, The 2026 Pennsylvania Medicaid Guide — slutskyelderlaw.com