Why This Rule Can Make or Break Your Financial Legacy

Long-term care planning often comes with tough questions—about aging, costs, independence, and protecting your family. One of the most misunderstood (and costly) elements of this planning is something called the 5-year lookback rule.

This rule affects anyone considering using Medicaid to help pay for nursing home or assisted living care. And because long-term care costs can run $7,000 to $10,000 per month, even families with significant assets can find themselves facing financial stress faster than they expect.

Understanding how this rule works—and taking action well in advance—can protect not just your money, but your family’s options, peace of mind, and legacy.

What Is the 5-Year Lookback Rule?

The idea is simple, but its implications are anything but.

When you apply for Medicaid, the government reviews your financial activity over the previous 60 months (5 years). This is called the “lookback period.”

If they find that you’ve given away assets—like money, property, or valuables—or sold them for less than they’re worth during that time, you may be penalized.

The penalty? A delay in Medicaid coverage. During this penalty period, you’ll need to pay for care out of pocket—even if your assets are gone.

Why the Rule Exists

Medicaid is intended for people who truly need financial help. Without this rule, someone could simply transfer all their assets to a family member one day, and apply for Medicaid the next—effectively shifting care costs to taxpayers.

The lookback rule encourages early, proactive planning. It’s not meant to punish; it’s meant to prevent last-minute, reactive moves that can disrupt both government programs and family financial plans.

Where Families Often Get Caught Off Guard

Here are three of the most common mistakes families make when it comes to long-term care and the lookback rule:

1. Gifting Too Late

It’s not uncommon for parents to gift their home or cash to adult children when their health starts declining. The problem? If care is needed within five years, that gift triggers a penalty—even if the intent was loving and practical.

2. Moving Money Without Guidance

Sometimes people think they can “hide” assets or move them around to qualify for aid. These efforts almost always backfire, and can lead to longer penalties, legal issues, or permanent denial of Medicaid eligibility.

3. Assuming “It Won’t Happen to Me”

According to the U.S. Department of Health and Human Services, nearly 70% of people over age 65 will need some form of long-term care. That’s not a maybe—it’s a high likelihood. Planning now, while you’re healthy, offers the most options.

A Costly (and Common) Real-World Scenario

A woman in her early 70s gifted her home to her daughter to “get ahead” of long-term care planning. She felt fine at the time. But three years later, she suffered a stroke and needed nursing home care.

Because the house transfer fell within the 5-year lookback, Medicaid denied her application. The family had to cover $90,000 out-of-pocket until the penalty period expired—money that could have supported both her care and her daughter’s family.

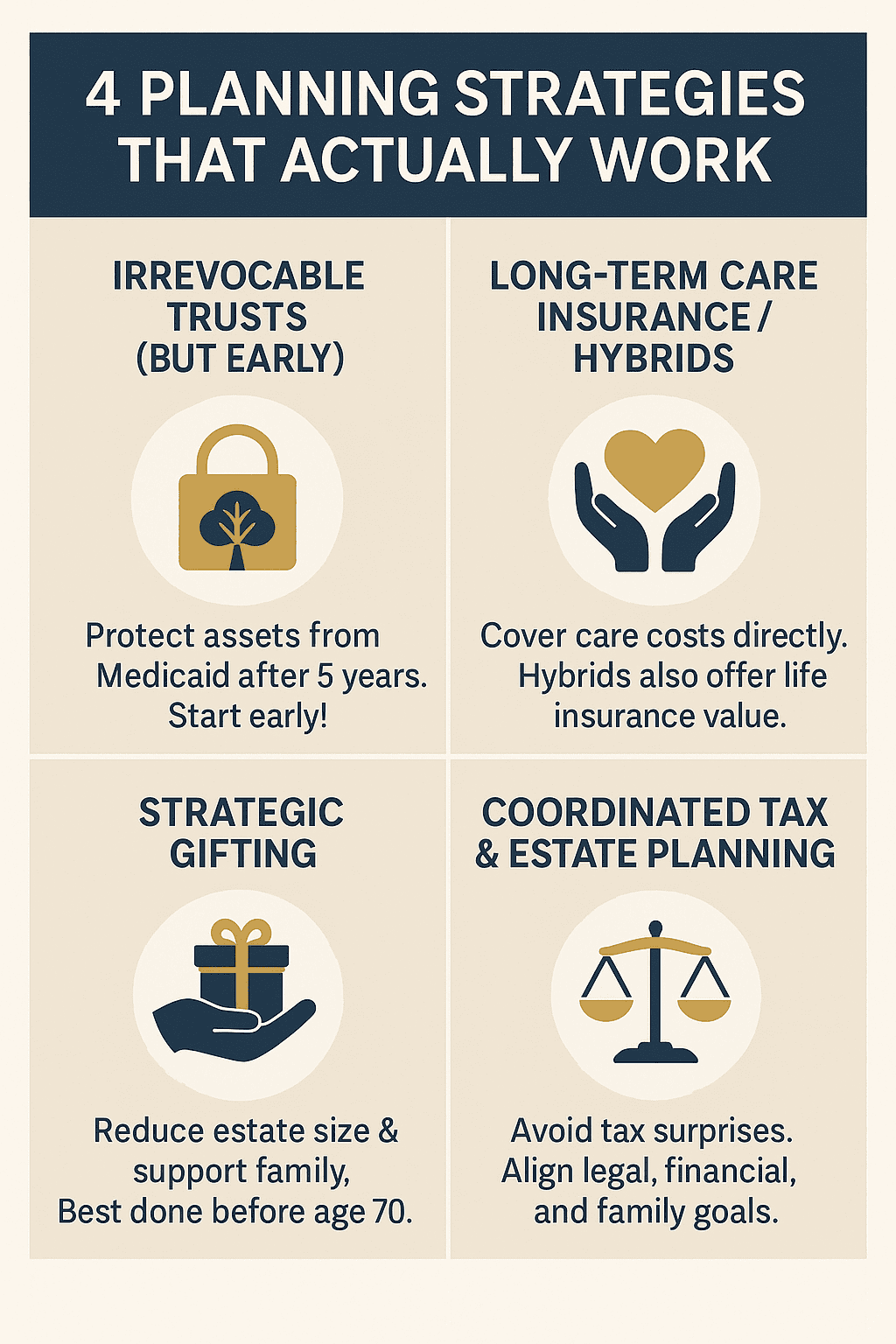

Planning Strategies That Actually Work

The good news is: there are smart, legal, and compassionate ways to plan around the lookback rule. The key is starting early and working with professionals who understand the full picture—legal, financial, and emotional.

1. Use Irrevocable Trusts (But Early)

Placing assets into an irrevocable trust removes them from your personal ownership. After five years, those assets are not counted by Medicaid. But timing is everything—the trust must be set up and funded well before care is needed.

2. Consider Long-Term Care Insurance or Hybrids

These policies can cover care costs directly, so you don’t need to spend down assets to qualify for Medicaid. Hybrid policies—combining life insurance with long-term care benefits—have become popular because they offer value even if you never use the care benefit.

3. Gift Strategically and Early

If supporting children or grandchildren is part of your plan, early gifts may reduce your taxable estate while giving you flexibility. Doing this before age 70 gives a longer cushion against potential care needs.

4. Coordinate With Tax and Estate Planning

Moving assets may impact capital gains, gift taxes, and estate taxes. A coordinated plan ensures you’re not solving one problem while creating another.

Why Even Affluent Families Should Pay Attention

There’s a common belief that long-term care planning is only for those with limited assets. But in reality, care costs can erode even large portfolios quickly.

Consider this:

- A couple with $2.5 million in retirement savings.

- One spouse enters long-term care for five years, at $100,000 per year.

- That’s $500,000 spent—20% of the nest egg—without accounting for taxes, investment losses, or inflation.

That’s money that could have supported a surviving spouse, covered healthcare for both, or left a legacy for children or charitable causes.

Questions Worth Asking Right Now

- If I (or my spouse) needed care tomorrow, how would we pay for it?

- Do I want to leave money to children or causes I care about, or am I comfortable spending down all assets?

- Do I have a strategy that combines private pay, insurance, and Medicaid planning?

- Have I talked to a professional about how long-term care might impact my spouse or heirs?

If you’re not sure about the answers, it’s time to take a closer look.

Facts and Research That Matter

- Genworth’s 2023 Cost of Care Survey: Average private room in a nursing home is now $7,908/month.

- U.S. Department of Health and Human Services: 70% of Americans age 65+ will need care.

- Forbes and Kiplinger: Both regularly warn that failure to understand the 5-year rule is one of the biggest risks to family wealth.

Next Steps to Protect Yourself and Your Family

Whether you’re 60 or 75, the best time to start planning is before care is needed. Here’s what you can do:

- Evaluate your assets and current estate plan.

- Talk to a financial planner and estate attorney—preferably ones who understand Medicaid planning and state-specific rules.

- Review your options for insurance, gifting, and trust creation.

- Create a long-term care roadmap that considers care quality, family dynamics, tax impact, and legacy goals.

Even small steps now can save your family significant stress—and money—later.

Final Thoughts: Planning Ahead Isn’t Paranoia—It’s Peace of Mind

The 5-year lookback rule is easy to overlook but costly to ignore. It’s not just about qualifying for government help—it’s about making sure you have choices, dignity, and financial security when it matters most.

By acting early, you protect not only your wealth but also the people you care about most. You’re not just preparing for the worst—you’re preserving the life you’ve worked hard to build.

Ready to Make a Confident Plan?

If you’re unsure how long-term care rules like the 5-year lookback could impact your finances, we can help. Our Retirement Reality Check™ walks you through the decisions that protect your family, your assets, and your options.

Schedule yours today.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 100+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

Please consult legal or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.