What 40 years of investor behavior data actually shows about who comes through volatile markets with their finances intact.

Key Takeaways

- Stop trying to predict markets – build a plan with guaranteed income, cash buffer, and proper asset allocation

- Average investors lose 15% of returns annually due to poor timing decisions, not bad funds

- Hold 1-2 years of expenses in cash to avoid selling investments during market downturns

- If guaranteed income covers 80% of essential expenses, you can weather market volatility better

- Rebalance your portfolio 1-2 times yearly to maintain your target stock/bond mix

If you have spent any part of this spring feeling unsettled about your portfolio, you are not overreacting. The environment earned that response. Military conflict in the Middle East.

Oil prices surging. The S&P 500 dropping roughly 7% in a matter of days. Then a ceasefire, a fast recovery, and markets ending up roughly where they started.

The whole sequence played out in less than two months.

That is disorienting. Not because something went wrong. Markets do this. But because when you are watching your savings swing by tens of thousands of dollars in a week, it is very hard to know if you are watching a temporary disruption or the start of something larger.

Before going further: when this article uses the word plan, it means three things. How your essential monthly bills get paid when you are no longer working. How you protect against a stretch of bad markets early in retirement.

And whether your investment mix matches when you actually need the money. That is it. It does not have to be a formal document.

But those three questions need answers.

Here is what most people ask in a volatile moment:

What should I Do?

It is the wrong question. The right question comes later in this article. And the answer to it does not require predicting anything about markets.

First, the data. Because the story of what reactive decisions actually cost is not subtle, and most people have never seen it laid out clearly.

The Gap Is Not About Bad Funds. It Is About Bad Timing.

DALBAR has tracked investor behavior every year since 1985. Their research compares what investment funds actually return to what investors in those funds actually receive. The gap is almost always there. And it is almost never caused by the funds themselves.

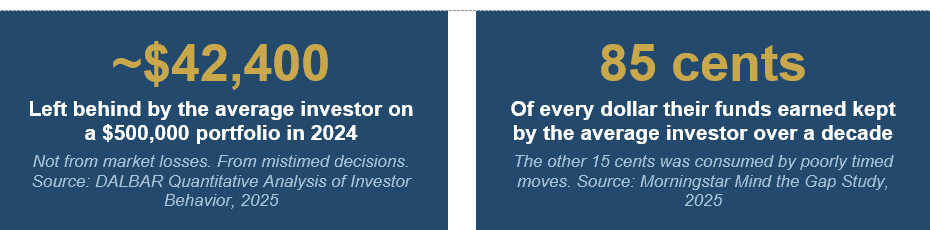

In 2024, a year when markets posted strong gains, the S&P 500 returned approximately 25%. The average equity investor earned approximately 16.5%. That 8.5 percentage point gap represents approximately $42,400 on a $500,000 portfolio in a single year.

Withdrawals from equity funds happened in every quarter of 2024. The largest outflows occurred just before the market’s biggest run-up.

Think about what that means in plain terms. Investors sold before the gains. They missed the recovery. Then they bought back in at higher prices.

Morningstar’s Mind the Gap study looked at the same pattern from a different angle. Over the 10 years ending December 2024, the average dollar invested in US mutual funds and ETFs earned approximately 7.0% per year. The funds themselves returned approximately 8.2% per year.

For every dollar those funds earned, the average investor kept about 85 cents. The other 15 cents disappeared from mistimed buying and selling. Morningstar found this gap has been consistent across five consecutive 10-year study periods.

It does not go away.

This is not a story about bad judgment or bad funds. Both studies point to the same cause: decisions made in reaction to market events rather than in response to a plan.

What That Gap Looks Like Over 20 Years

A hypothetical investor who put approximately $100,000 in the S&P 500 in 2004 and held it untouched would have ended 2024 with approximately $717,000, according to DALBAR’s analysis.

The average investor, following the behavioral patterns the same research tracks, ended with approximately $346,000.

Same starting amount. Same market. Roughly half the outcome.

The market came back in April 2026. The investors who had to sell in March did not benefit from that recovery on the shares they sold. That is the whole story.

Three Structural Decisions That Make Market Timing Largely Irrelevant

When markets are moving fast, most people ask: what is the market going to do next? Nobody reliably knows. Not analysts.

Not advisors. Not the Federal Reserve. Decades of data on market prediction are not encouraging.

The right question is this:

- If markets dropped significantly and stayed down for 12 to 18 months, could my plan continue without forcing a decision I would regret?

That question has a real answer. And finding it does not require predicting anything.

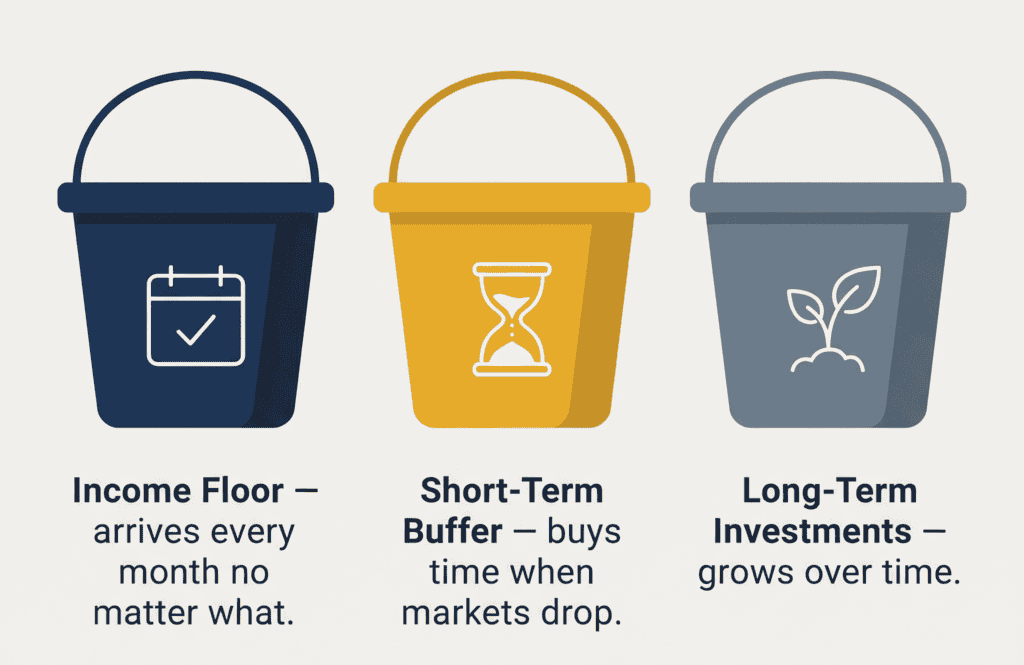

A plan that can survive a volatile market is built on three structural pieces. Each one has a specific job. Together, they make market timing mostly beside the point.

Piece 1: An Income Floor That Does Not Move With Markets

Your income floor is the portion of your monthly income that arrives no matter what the stock market does. Social Security. A pension.

Income from an annuity. This income does not drop when markets fall 7%. It does not require selling anything.

It just shows up.

The purpose of an income floor is not just financial. It is behavioral. Retirees with a solid income floor tend to make better decisions during market downturns. When the question of whether you can cover your bills is already answered, the question of whether to sell your investments becomes much easier to think through clearly.

What It Feels Like When the Floor Is Missing

Picture this: it is March 2026. Markets are down roughly 7%. Your account is red. You need to transfer money into your checking account by Friday to cover your mortgage, insurance, and groceries.

You have two options. You can sell investments now at lower prices to raise the cash. Or you can wait and hope markets recover before Friday.

Neither option feels right. One locks in a loss. The other adds risk you did not plan for.

This is the exact situation a reliable income floor prevents. When guaranteed income already covers the essentials, you are not in this position. The Friday transfer is handled. The investment account can wait.

A practical way to measure your own floor: add up your monthly income from sources that do not depend on markets (Social Security, pension, annuity income) and divide by your essential monthly expenses (housing, utilities, food, insurance, healthcare). If that number is above 80%, your basics are largely covered by income that does not move with markets. If it is below 80%, a meaningful portion of your essential spending depends on your portfolio staying healthy. That gap is worth understanding.

Piece 2: A Short-Term Cash Buffer That Buys You Time

There is a risk in retirement that most people have never heard named. It is called withdrawal timing risk, sometimes called sequence of returns risk. The concept is simple: for retirees drawing money from a portfolio, the timing of market downturns matters just as much as how severe they are.

Why Timing Matters More Than Most People Realize

Suppose two people each start retirement with approximately $500,000 and plan to withdraw approximately $30,000 per year to cover living expenses. Both average similar long-term returns over 20 years.

But one experiences a significant market decline in the first three years of retirement. To cover their $30,000 annual withdrawal, they have to sell shares at reduced prices. The money from those sales is spent. When markets recover, the recovery applies to whoever still holds shares, not to the shares that were already sold.

The person who hit bad years late in retirement never had to sell low. Their portfolio stayed invested through the recovery.

After 20 years, the second person may end up in a meaningfully stronger position, even though both averaged similar long-term returns. The difference was not the market. It was the timing of when they needed the money.

The people who came through this spring’s decline with their finances largely intact often had one thing in common: they did not need to sell long-term investments to cover short-term needs.

A short-term cash buffer is typically one to two years of planned withdrawals held in short-term savings, separate from your long-term investments. When markets drop, you draw from the buffer. You leave the long-term investments alone.

When markets recover, you rebuild the buffer. No prediction required. Only the structure needs to be in place before the next downturn arrives.

The buffer is not a market prediction. It is a maintenance tool.

Its only job is to help make sure a market decline does not become a forced decision.

Piece 3: An Investment Mix That Matches Your Actual Timeline

Your investment mix is simply the percentage of your money in stocks versus bonds versus cash. Think of it as three buckets. Stocks for long-term growth.

Bonds and cash for stability and near-term needs. The mix should reflect when you need the money, not what the market did last month.

A 68-year-old drawing income from their portfolio now has a different situation than a 52-year-old with 13 years before they stop working. Both need growth. But how much risk each person can absorb before they need the money is completely different. That difference should drive the mix, not recent headlines.

Portfolios drift. A mix that was right in January 2026 may not be right today. The spring decline may have pushed you more conservative than planned.

The recovery may have pushed you more aggressive. In both cases, the question is not whether the new mix feels comfortable. The question is whether it still matches the plan.

A Simple Example of How Drift Works Against You

Suppose your target is 60% stocks and 40% bonds. Markets drop in March. You do not sell anything, but stocks fall faster than bonds, so your mix shifts to roughly 53% stocks and 47% bonds.

Markets recover in April. Your stocks bounce back, but since you now hold fewer of them than your plan called for, you capture less of that recovery than your original mix would have.

A rebalancing check, done once or twice a year, catches this. It is not a market call. It is returning the mix to the plan. Investors who do this consistently tend to capture more of the market’s long-term return than those who let the mix drift with whatever just happened.

What This Looks Like at Every Stage

These three pieces matter at every age. But what to focus on right now depends on where you are.

If you are between 50 and 57:

This is the most underestimated window in retirement planning. You likely have 10 to 17 years before you stop drawing a paycheck. That runway is a genuine advantage, and most people do not use it deliberately.

The key tasks at this stage: maximize contributions to retirement accounts, including catch-up contributions available at age 50; look at the ratio of pre-tax savings to Roth savings and consider whether diversifying across both account types before retirement would give you more flexibility later; and start modeling what your income floor will look like when you retire. The earlier you run that analysis, the more time you have to improve the number.

Many people in their early 50s are facing real competing pressures. College tuition, aging parents, housing decisions, career transitions. These are legitimate demands.

The families who arrive at 60 in the strongest position are often simply the ones who did not let those pressures crowd out retirement contributions entirely. Even partial contributions during this window compound over a long horizon.

If you are between 58 and 65 and still working:

The decisions made in the three to five years before retirement tend to matter more than almost anything that came before them. This is when you build the structure you will actually live in. That means understanding your income floor before you need it, deciding how large a cash buffer to hold in the early years of retirement, and confirming your investment mix will shift as you move from building savings to drawing income.

Social Security timing is one of the highest-impact decisions in this window. Claiming early permanently reduces the monthly benefit. Waiting locks in a larger one. That decision alone deserves a dedicated conversation with an advisor before it is made.

If you are between 65 and 73 and recently retired:

The first five to seven years of retirement carry the highest withdrawal timing risk of the entire retirement. If a short-term cash buffer is not yet in place, building one now, while markets are calm, is among the most structurally valuable steps available. This is a risk management step, not a market call.

This is also the time to measure your income floor carefully. Many retirees discover they have more guaranteed income than they thought, or less. Running the income floor calculation described in Piece 1 takes about five minutes and gives a clear picture.

If you are 73 or older and taking Required Minimum Distributions:

At this stage, how your income sources work together matters as much as how your investments perform. And the risk most people underestimate here is not market volatility. It is the tax and Medicare cost of having too much income forced into a single year.

A Common Situation at This Stage

Consider a retiree at age 74 with a large traditional IRA. Required Minimum Distributions push taxable income higher each year. Combined with Social Security, that income may cross the threshold that triggers higher Medicare premiums (called IRMAA surcharges).

A partial Roth conversion done in earlier years, before RMDs began, might have reduced the IRA balance and kept future distributions smaller. That would have meant lower RMDs, potentially lower Medicare costs, and more tax-free income available later.

The planning opportunity at 73 and beyond is not primarily about market returns. It is about whether income sources are coordinated in a way that reduces unnecessary tax and healthcare costs across a retirement that may last 20 or more years.

Action step: If you have not reviewed how your RMDs, Social Security income, and Medicare premium costs interact, that review is worth scheduling before year-end.

Your Anxiety May Be Pointing at Something Real.

The unease many people feel right now about their portfolios is not irrational. Geopolitical tension, rising costs, a changing Federal Reserve, tax law shifts, and sharp market swings in both directions are a lot to absorb. Feeling unsettled is a reasonable response to the environment.

But anxiety and actual risk are not the same thing. Feeling anxious does not mean your plan is broken. And not feeling anxious does not mean it is solid. The only way to know which situation you are in is to look honestly at the three pieces above.

If all three are in place, the anxiety may still be present but it does not need to lead anywhere. A floor that covers the essentials. A buffer that buys time.

A mix that already accounts for the road ahead. When those three things exist, a volatile market is uncomfortable but it is not dangerous.

If one of the three is missing, the anxiety is pointing at something real and worth addressing. Finding that gap now, while markets are calm, is far more manageable than finding it during the next difficult stretch.

You Do Not Need to Be Right. You Need to Be Structured.

The investors who tend to come through volatile periods with their plans intact are not the ones who predicted what would happen. They are the ones who built a plan that did not require a prediction.

An income floor that covered the basics. A buffer that bought time. A mix that already accounted for the road ahead.

When markets dropped, they did not face a forced decision. Their structure had already made the decision for them.

The market came back in April 2026. The investors who had to sell in March did not benefit from that recovery on the shares they sold.

That is the whole argument for building a plan before you need it. Not to predict the next volatile stretch. Not to time the recovery. But to make sure the next one, whenever it comes, does not force a decision you will carry for the rest of your retirement.

If you read this and feel confident that all three pieces are in place, hold onto that confidence. If you feel uncertain about even one of them, that uncertainty is useful. It points to exactly where to focus next.

📅 Wondering which of these three structural pieces is missing from your retirement plan? Schedule a 25-minute planning review to identify gaps in your income floor, cash buffer, or investment mix specific to your situation. Visit langanfinancialgroup.com/get-started-today or call 717-288-1880.

One of these three elements is missing from many retirement plans.

We offer a planning review that identifies which one it is for your specific situation. No sales pitch. Just a picture to help you identify where your plan stands across all three. Call us at 717-288-1880.

About the Financial Planning Author

Alexander Langan, J.D, CFBS, serves as the Chief Investment Officer at Langan Financial Group. In this role, he manages investment portfolios, acts as a fiduciary for group retirement plans, and consults with clients regarding their financial goals, risk tolerance, and asset allocation.

With a focus on ERISA Law, Alex graduated cum laude from Widener Commonwealth Law School. He then clerked for the Supreme Court of Pennsylvania and worked in the Legal Office of the Pennsylvania Office of the Budget, where he assisted in directing and advising policy determinations on state and federal tax, administrative law, and contractual issues.

Alex is also passionate about giving back to the community, and has participated in The Foundation of Enhancing Communities’ Emerging Philanthropist Program, volunteers at his church, and serves as a board member of Samara: The Center of Individual & Family Growth. Outside of work and volunteering, Alex enjoys his time with his wife Sarah, and their three children, Rory, Patrick, and Ava.

About Langan Financial Group: Financial Advisors

Langan Financial Group is an award-winning financial planning firm with offices in York, Pennsylvania and Harrisburg, Pa.

With over 150+ 5-star reviews, Langan Financial Group is an independent financial planning firm established in 1985, offering a broad range of financial planning services.

With an open architecture platform, our advisors have access to a diverse range of products, free from any sales quotas.

Our team of 11 financial experts, each with unique specialties, enhances our ability to focus on delivering value to our clients.

Disclosure

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax, financial or legal advice.

Please consult financial, legal, or tax professionals for specific information regarding your individual situation.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Hypothetical and illustrative examples are for educational purposes only and do not represent the results of any specific investment or individual. Individual results will vary based on specific financial circumstances. Dollar figures in hypothetical examples are approximate and for illustration purposes only.

References to income floors, cash buffers, and investment mix strategies are general planning concepts and are not specific recommendations for any individual. The income floor percentage calculation is a planning illustration only and does not constitute a guarantee or projection of retirement income adequacy. Social Security claiming decisions depend on individual circumstances and no single strategy is appropriate for everyone.

IRMAA surcharge thresholds are subject to annual adjustment by the Centers for Medicare and Medicaid Services. Please consult a qualified financial, tax, or legal professional before making any financial decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC.

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc. a Registered Investment Advisor. Cambridge and Langan Financial Group, LLC are not affiliated.

Cambridge does not offer tax or legal advice.