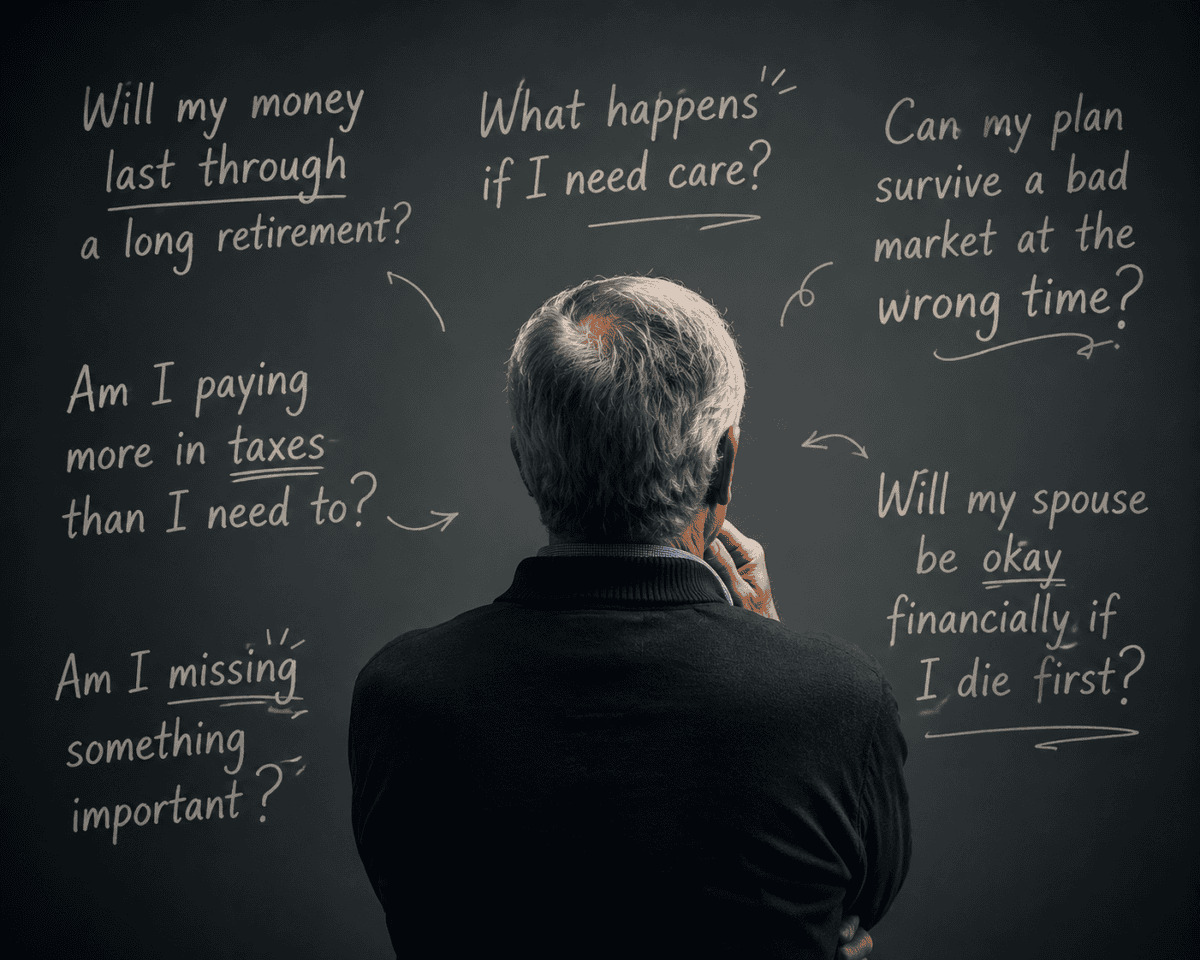

A diagnostic guide for the worries that matter most, and permission to stop worrying about the ones that don’t

Most retirement anxiety is not really about money. It is about uncertainty. Not knowing whether a given risk is actually your problem is what keeps people up at night.

Our first article in this series named the six fears that show up most often and explained the psychology behind why they persist. This one helps you go further. For each concern, we identify the honest signals that suggest a real gap. We describe what the area looks like when it is handled well. And we outline what to explore if it is not.

If a concern does not apply to your situation, that clarity is just as valuable as a solution. The goal of this article is not to give everyone something to fix. It is to help you know which problems are actually yours.

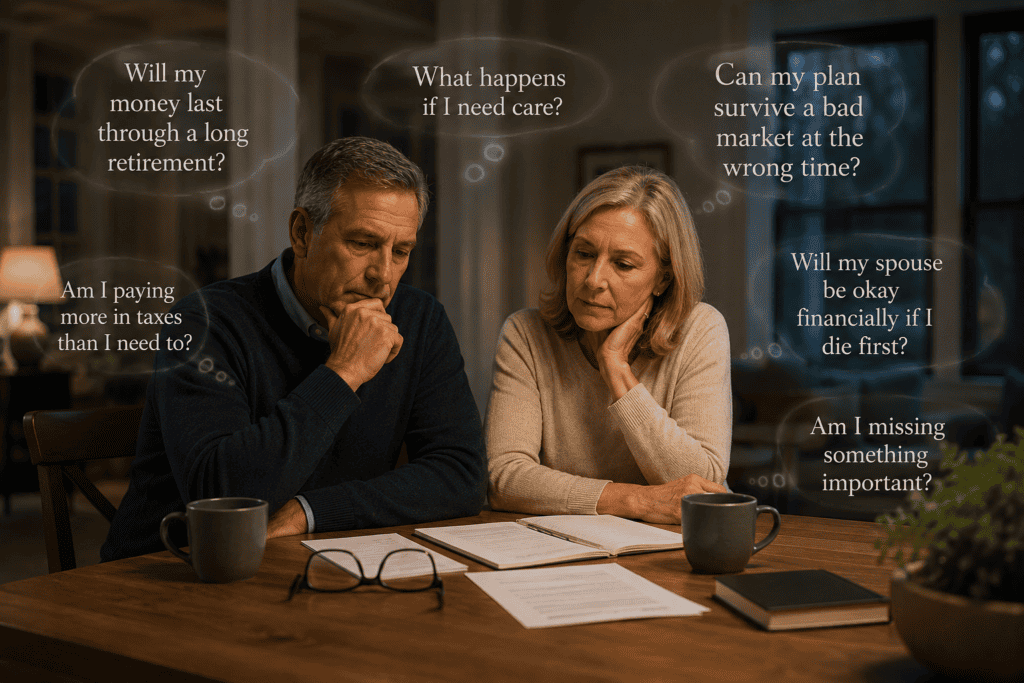

Note: Several sections reference couples and spouses because many of these concerns affect households differently depending on filing status and income sources. If you are single, widowed, or divorced, the same concerns apply; the diagnostic signals and approaches are simply applied to your individual picture.

Concern 1: Will My Money Last?

How to know if this is your problem

A few honest signals suggest this area may deserve attention:

- You cannot name your current withdrawal rate, or no one has ever calculated it.

- You have never seen a projection that shows income lasting to age 90 for both spouses individually.

- Your plan was built during a different interest rate environment and has not been stress-tested since.

If none of these apply, this area is likely in good shape.

What it looks like when it is handled: A projection runs to age 90 or beyond, models both spouses separately, accounts for inflation, and has been reviewed in the last 12 months. You know your withdrawal rate and it has been tested against a range of market scenarios.

If there is a gap, here is what to explore

A structured withdrawal strategy replaces guesswork with a tested framework. William Bengen’s research and the Trinity Study established a starting range, though the right rate depends on your specific income sources and spending needs. The value is discipline: a plan that can be reviewed and adjusted annually. For pre-retirees, this is worth modeling before leaving a paycheck. For those already retired, it is worth reviewing if the plan has not been stress-tested against today’s rate environment.

Delaying Social Security may be one of the most powerful longevity tools available. Claiming at 62 permanently reduces your benefit. Waiting past your full retirement age adds ~8 percent per year up to 70. Combined, the difference between filing at 62 versus 70 may be over 75 percent in monthly income. For couples, the claiming decision can be designed around the survivor’s long-term benefit, since the survivor keeps the higher of the two. The trade-off is funding the gap years from other assets.

For households with limited stable income, a modest income annuity can serve as a floor that may significantly reduce longevity risk. It is not right for everyone, and it trades liquidity for certainty.

Concern 2: What Happens if You Need Care?

How to know if this is your problem

- You believe Medicare covers long-term custodial care. It does not.

- You are 55 or older and have never had a specific conversation about how a multi-year care event would be funded.

- You cannot name which assets would pay for care or what your spouse would have left afterward.

If you have a funded strategy and you know the answers to those questions, this concern is likely addressed.

What it looks like when it is handled: A specific funding plan exists. You know which assets cover care costs. You have estimated what three or more years of care in your area could realistically cost. You know what income and assets the surviving spouse would have if care consumed a significant portion of the plan.

If there is a gap, here is what to explore

In Pennsylvania, a private nursing facility room may range from approximately $10,000 to over $15,000 per month according to the Genworth 2024 Cost of Care Survey. Three approaches exist, each carrying a different trade-off.

Traditional long-term care insurance pays a benefit for qualifying care. It tends to make the most sense for households with meaningful assets to protect but not enough to absorb a multi-year care event without disrupting the surviving spouse. The honest trade-off is premium cost and the reality that premiums have risen significantly in recent years.

Hybrid products combine a life insurance or annuity component with a long-term care rider. If care is never needed, the death benefit is typically not lost. These tend to work best for households that would have purchased life insurance or an annuity anyway.

Self-insuring means designating a portion of your portfolio specifically for care costs. It works for households where a care event, while expensive, would not fundamentally threaten the surviving spouse’s lifestyle. It requires discipline and a realistic cost estimate for your area.

Concern 3: What if the Market Drops at the Wrong Time?

How to know if this is your problem

- All or most of your retirement income depends on selling investments each month.

- You cannot name an income floor, meaning a set of sources that covers your essential expenses regardless of what the market does.

- During a past market decline, you felt a strong urge to sell or move to cash.

If your essential expenses are already covered by stable sources and you have not felt compelled to react during downturns, this concern may not apply to you.

What it looks like when it is handled: You can name your income floor. Essential expenses are covered by stable sources for at least two years without touching your investment portfolio. A market decline is uncomfortable, but it may not force a financial decision.

If there is a gap, here is what to explore

The bucket strategy divides assets into three pools. The short-term pool holds one to three years of stable, liquid assets. The medium-term pool holds bonds and moderate-risk holdings. The long-term pool holds growth assets. When markets fall, you draw from the short-term bucket rather than selling at a loss. Growth assets have years to recover before they need to be touched. Morningstar research suggests the strategy’s primary value may be behavioral: it may reduce the pressure to react.

Separating an income floor from a growth portfolio is a related approach. Social Security, a pension, bond income, or a modest annuity covers essential spending. The growth portfolio handles discretionary spending. A market drop may no longer trigger a financial emergency.

Dynamic withdrawal rules, developed by researchers including Jonathan Guyton, build flexibility into the annual withdrawal amount. Spending adjusts slightly in bad years and can increase in strong ones. This flexibility, agreed upon in advance, may extend portfolio longevity compared to a rigid fixed-rate approach.

Concern 4: Am I Paying More in Taxes Than I Need To?

How to know if this is your problem

- Your investment advisor and your tax preparer have never spoken to each other or coordinated on your behalf.

- You have never seen a tax projection that runs beyond the current year and covers all of your income sources together.

- You are not sure whether your 2024 income triggers higher Medicare premiums in 2026, or you have never heard of IRMAA.

If you have a multi-year projection and your advisor and tax preparer coordinate regularly, this concern is likely in good shape.

What it looks like when it is handled: A tax projection runs through at least age 80. It covers Social Security, RMDs, pension income, and Medicare premiums together, not in separate conversations. Someone is watching the interaction between all of those sources, not just the individual parts.

If there is a gap, here is what to explore

The pre-RMD Roth conversion window is one of the most time-sensitive opportunities in retirement planning. Between retirement and age 73, many households have lower taxable income before required minimum distributions begin. This window is most relevant for people roughly between 60 and 72 who are retired or semi-retired. Converting traditional IRA or 401(k) assets to Roth during this window means paying tax at potentially lower rates now. It may also reduce future RMDs. Once RMDs begin at 73, taxable income rises and the conversion math often changes significantly. The trade-off is a higher tax bill in the conversion year, which requires cash or taxable assets to cover.

Tax-efficient withdrawal sequencing determines which accounts you draw from first. The conventional order draws from taxable accounts first, then tax-deferred, then Roth. But the right answer varies by year. In some years, drawing more from a traditional IRA to fill a lower bracket reduces lifetime taxes more than strict sequencing. This is a decision worth revisiting annually, not setting once.

For people 70 and a half or older, qualified charitable distributions allow up to $111,000 per year to transfer directly from an IRA to a qualified charity. The amount counts toward the RMD but is excluded from taxable income. For households that give to charity, this may reduce taxable income, lower Medicare IRMAA exposure, and reduce Social Security taxation simultaneously.

Concern 5: Will My Spouse Be Okay?

How to know if this is your problem

- You cannot name the specific monthly income change your household would face at the first death.

- Your spouse could not independently describe your household’s full financial picture if asked today.

- A pension survivor election was signed at retirement without modeling the trade-offs in detail.

If both of you know the numbers and have talked through the survivor scenario specifically, this concern may not require action.

What it looks like when it is handled: A written projection exists for the survivor scenario. Your spouse knows the income, the tax picture, and where every account is held. Social Security claiming and pension elections were made with the survivor’s lifetime income in mind, not just the first recipient’s.

If there is a gap, here is what to explore

For couples, Social Security claiming strategy can be designed around maximizing the survivor’s benefit rather than each individual’s benefit. The survivor keeps the higher of the two benefits. Delaying the higher earner’s filing may provide the surviving spouse with meaningfully higher income for decades. This decision is worth modeling with specific numbers before either spouse files.

The pension survivor election is one of the most permanent financial decisions a household makes. It is often treated as a formality at paperwork time. Choosing a higher pension today in exchange for a reduced or eliminated survivor benefit may leave a spouse with a significant income gap. The right election depends on other income sources, the age difference between spouses, and the health of each.

For some households, life insurance in retirement can serve as an income bridge for the surviving spouse, particularly where one spouse’s income drives most of the household’s financial picture. Whether it makes sense depends on insurability, cost, and what survivor protections are already in place.

Concern 6: Am I Missing Something?

How to know if this is your problem

- Your last comprehensive planning review covered investments but not taxes, healthcare costs, estate documents, and the survivor scenario together.

- You have not checked your beneficiary designations since a major life event such as a marriage, divorce, death, or birth.

- No single advisor or team has a complete view of your full financial picture.

If you have had a full review within the last year and your beneficiaries are current, this area is likely covered.

What it looks like when it is handled: One advisor or team has a current view of all six areas. Annual reviews cover income, taxes, healthcare, estate documents, and the survivor scenario together. Beneficiary designations have been reviewed recently and reflect your current wishes.

If there is a gap, here is what to explore

Coordinated planning means one advisor or team sees the full picture: income, taxes, healthcare costs, insurance, estate documents, and investment accounts. When planning is split across several unconnected relationships, gaps tend to live between those relationships, not within any one of them. A tax preparer who does not know your Roth conversion opportunity. An investment advisor who does not know your pension election. Coordination closes that space.

An estate document review is one of the most deferred tasks in retirement planning and one of the most consequential to skip. A will, durable power of attorney, and healthcare directive are designed to help ensure your wishes are followed if you cannot speak for yourself. A trust may also be appropriate depending on your estate. Documents set years ago may not reflect your current family situation or applicable state law.

A beneficiary audit is the simplest action on this list. Beneficiary designations on retirement accounts, life insurance, and annuities pass assets directly to whoever is named, regardless of what your will says. An ex-spouse, a deceased parent, or a child named decades ago may still be listed. It takes less than 30 minutes and costs nothing. It is also the type of error that cannot be corrected after the fact.

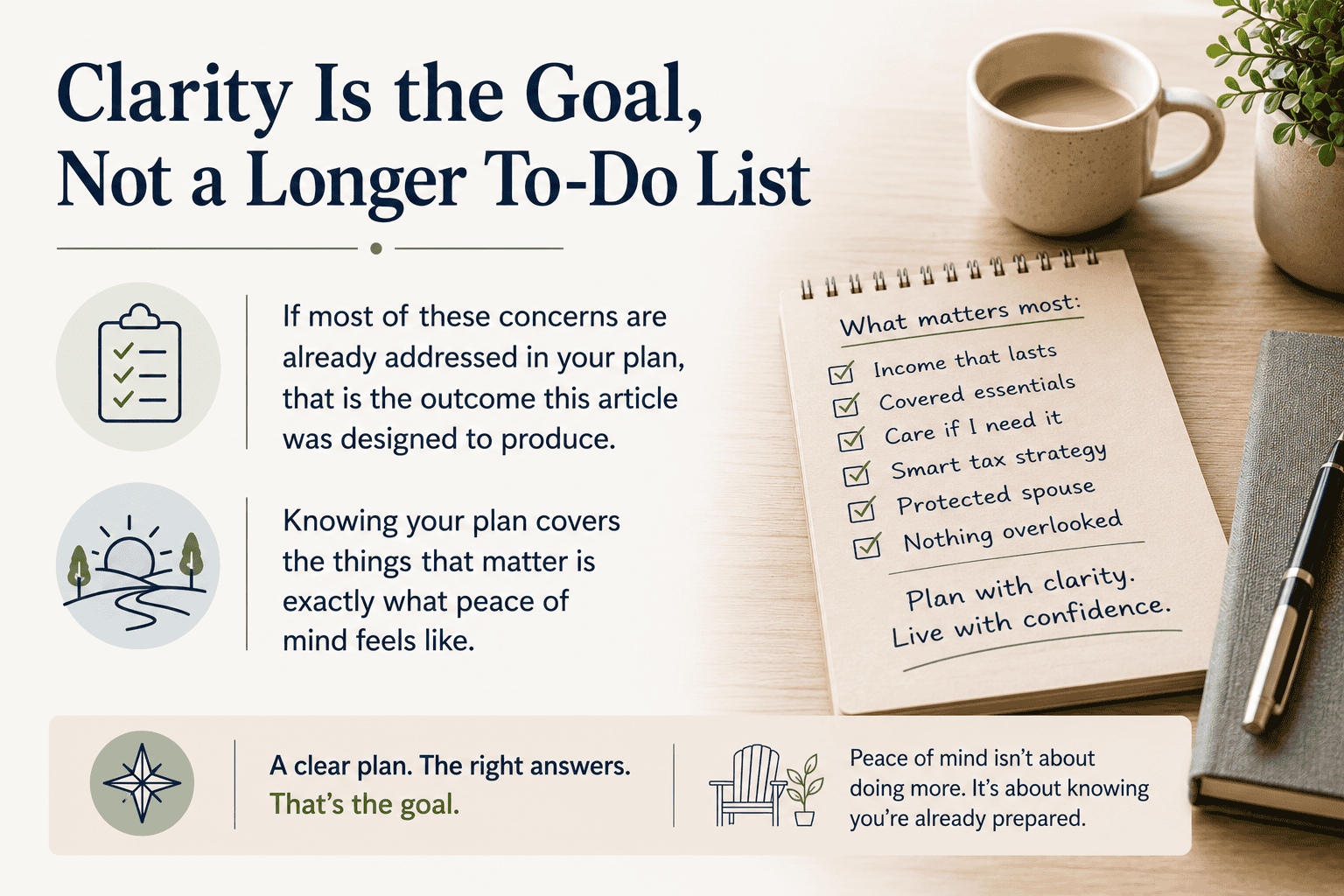

Clarity Is the Goal, Not a Longer To-Do List

If most of these concerns are already addressed in your plan, that is the outcome this article was designed to produce. Knowing your plan covers the things that matter is exactly what peace of mind feels like.

If you found one or two areas where the honest answer was “I don’t actually know,” those are worth a conversation. Not urgently. But before a health event, a tax deadline, or an irreversible election makes the decision for you.

The third piece in this series is a self-assessment tool. It helps you score each of these six areas and identify which approaches are worth exploring first.

Not Sure Which of These Apply to You?

A complimentary conversation can help identify which areas may need attention and what a more complete plan could look like for your specific situation.Schedule a Complimentary Conversation

Sources referenced in this article: Bengen, W. (1994), Determining Withdrawal Rates Using Historical Data; Trinity Study (Cooley, Hubbard, Walz, 1998); Genworth/CareScout Cost of Care Survey (annual; figures cited reflect 2024 Pennsylvania data); Morningstar research on bucket strategy and sequence of returns; Guyton, J. and Klinger, W. (2006), research on dynamic withdrawal rules; Social Security Administration, benefit rules and survivor provisions; IRS Publication 590-B, qualified charitable distributions; DALBAR Quantitative Analysis of Investor Behavior, 2025.

This article is for educational purposes only and should not be considered investment, tax, or legal advice. All strategies described involve trade-offs and may not be appropriate for all individuals. All investing involves risk, including the potential loss of principal. Tax strategies are general in nature; individual outcomes depend on specific circumstances and applicable law. Annuity and insurance products involve costs, limitations, and risks that should be reviewed carefully before purchase. Qualified charitable distribution limits are subject to IRS rules and may change. Consult a qualified financial, tax, or legal professional before implementing any strategy described here.

Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC. Investment Advisory Services offered through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.

No Fields Found.