Tactical Article

Key Takeaways

- Create a family code word on paper to verify identities during emergency calls involving AI voice cloning.

- Adults 60+ average ,000 in fraud losses, making targeted defenses urgently necessary for this age group.

- 30% of reported fraud losses originate on social media, where scammers harvest voice samples for cloning.

- Six specific fraud entry points each have a dedicated defense requiring under ten minutes to implement.

- Both personal finances and aging parents require separate fraud protection strategies outlined in this guide.

By Langan Financial Group | June 3, 2026

Adults 60 and older filed the most fraud complaints of any age group in 2024 and suffered the most severe losses, with an average reported loss of $83,000 according to the FBI. The schemes behind those losses are professionally designed. Each one targets a specific kind of trust. And each one has a specific defense.

Six defenses close the six most active entry points. Most take less than ten minutes. None requires technical expertise.

Many readers are protecting both their own finances and watching over an aging parent. Both situations are addressed here, and a dedicated section on how to help a parent appears near the end.

Defense 1: The Family Code Word

Protects against AI voice cloning and emergency scams

AI can now clone a human voice from a few seconds of audio pulled from a social media video. According to the Hiya State of the Call 2026 report, 1 in 4 Americans received a deepfake voice call in the past 12 months. Security researchers describe this technology as having crossed the indistinguishable threshold: human listeners can no longer reliably detect a cloned voice from the real one.

The most common version targets grandparents. A caller uses a cloned voice of a grandchild or adult child to report an arrest, accident, or emergency. The request always includes instructions not to tell other family members. The FTC’s 2025 data shows that nearly 30 percent of fraud that resulted in reported losses started on social media, which is where most voice samples are harvested.

Choose a specific word or short phrase with your immediate family. Write it on paper. Not in a phone or email.

Tell your children and grandchildren what it is and why it exists. If anyone calls with a family emergency and cannot immediately give the code word, hang up and call that person back on a number you already have. Share it with your parents too if they have grandchildren who post on social media.

The defense

Pick a family code word. Write it on paper. Share it with immediate family. Any emergency call where the caller cannot give it immediately: hang up, then call back on a number you already have.

Time required: 10 minutes. Tools needed: paper and pen.

Defense 2: The Verification Rule

Protects against investment fraud and crypto scams

Investment fraud was the largest dollar-loss fraud category in both FTC and FBI data for 2025. The most common version, pig butchering, begins not with an investment pitch but with a relationship. A text sent to what appears to be the wrong number.

A new social media connection who mentions strong returns in passing. The relationship builds over weeks to months before any investment is mentioned. By then, the victim trusts the person presenting it.

Two defenses cover this entirely. First, verify any investment firm at investor.gov or FINRA BrokerCheck before sending money. Both are free and take a few minutes.

Legitimate firms and licensed advisors can be confirmed immediately. Second, and more importantly, tell your financial advisor before any money moves. Every pig butchering scheme, without exception, tells the victim to keep the opportunity away from their advisor.

That instruction is the signal that something is wrong.

If you are already involved with a platform, attempt a small withdrawal before investing more. These platforms frequently allow small early withdrawals to build confidence. If the withdrawal triggers new fees, tax requirements, or delays, stop and do not send more money.

The defense

Verify any investment firm at investor.gov or FINRA BrokerCheck before sending money. Tell your financial advisor about any investment introduced through social media or an online connection. If the opportunity requires secrecy from your advisor, stop immediately.

Time required: 5 minutes to verify online. One phone call to your advisor.

Defense 3: The Callback Rule

Protects against IRS, Social Security, Medicare, and bank impersonation

Impersonation scams were the most reported fraud category in 2025, generating more than one million complaints and $3.5 billion in losses according to FTC data. Reports rose 40 percent in a single year. The scheme takes many forms: a suspended Social Security number, back taxes owed, a Medicare account flagged for review, or a bank fraud alert requiring immediate verification.

The call may appear to come from a legitimate number. The caller may know your name and address. Some calls now use AI-generated voices.

Every variation has the same ending: move money to a safe account, pay via gift card, provide your account code, or stay on the line while you drive to the bank. Gift cards are now the most common payment method demanded in impersonation scams, according to FTC data. Three facts eliminate nearly every variant: the IRS contacts taxpayers primarily by mail.

The Social Security Administration does not suspend Social Security numbers by phone. No bank secures your money by asking you to move it.

The defense

Hang up. Call the agency or bank back using a number you already have, on your card or their official website. Never call back using the number the original caller provided.

Time required: 30 seconds to hang up. A few minutes to call back.

Defense 4: The Direct Access Rule

Protects against phishing texts, fake alerts, and account takeover

The FTC reported $470 million in text-based fraud losses in 2024, more than five times the 2020 figure. The most active variants include fake package delivery notices, unpaid toll texts, fake bank fraud alerts, and what the FTC describes as wrong-number investment setups, texts apparently sent in error that lead to an investment scheme. AI has largely eliminated the typos and odd grammar that used to make phishing messages detectable. These messages now read as authentic as real ones.

Rather than trying to identify a fake message, the defense removes the risk entirely. Open the official app directly, or type the website address yourself. If the message was legitimate, the issue will still be there when you arrive through your own channel. This helps even when the message looks completely real, because the defense does not rely on being able to tell the difference.

The defense

Never use a link or phone number from an unexpected text or email. Open the official app yourself or type the address. The issue will still be there if it was real.

Time required: Seconds. No setup needed.

Defense 5: The Wire Verification Call

Protects against real estate wire fraud and business email compromise

The FBI reported $3.05 billion in business email compromise losses in 2025. The most dangerous version for this audience targets real estate closings. A hacker gains access to the email thread between a buyer, their real estate attorney, and the title company.

At the right moment, they send fraudulent wire instructions that look identical to the attorney’s real emails. The buyer wires the closing funds to a criminal account. The attorney never sent that email.

One phone call prevents this entirely. Before wiring any amount for a real estate transaction, call the title company or attorney on a phone number you already have on file, not one from any email. Confirm the wire instructions verbally.

This is relevant for anyone downsizing, buying a retirement property, or helping a family member through a home purchase. Share this rule with them before their closing, not after.

If a fraudulent wire transfer occurs, the FBI’s Recovery Asset Team reports a 66 percent success rate at recovering funds when notified within hours. That window closes fast.

The defense

Before wiring money for any real estate transaction, call the title company or attorney on a number you already have. Verify verbally. Never confirm wire instructions by email alone.

Time required: One 3-minute phone call before each wire.

Defense 6: The Remote Access Rule

Protects against tech support scams and safe account schemes

The FBI reported $2.13 billion in tech support and customer support fraud losses in 2025. The scheme typically begins with a pop-up saying your computer has been compromised, with a number to call for Microsoft or Apple support. Once remote access is granted, the caller can see every account on the device.

A related version involves a caller claiming to be your bank’s fraud department who says accounts must be moved immediately to a safe account. A growing courier variant involves someone arriving at the home to collect cash or gold the victim was told to withdraw.

Two rules apply. First, never allow remote access to your computer from an unsolicited call or pop-up. If a pop-up will not close, shut the browser down from outside the pop-up window or turn off the computer.

Second, no financial institution secures your money by asking you to move it, withdraw cash, or send a courier for anything. Those requests are the scheme itself.

The defense

Never grant remote access to your computer from an unsolicited contact. No legitimate institution secures your money by asking you to move it, withdraw cash, or hand anything to a courier. Hang up and call your bank directly.

Time required: 30 seconds to hang up.

Four Steps That Protect Across All Schemes

The six defenses above address specific schemes. These four steps help regardless of which scheme arrives first. Together they take less than an hour.

1. Freeze your credit at all three bureaus

Free. Takes about 20 minutes total.

The CFPB states that a free credit freeze is the only free option that can prevent new-account fraud before it happens. Paid monitoring services primarily alert you after a change has already occurred. Go to equifax.com, experian.com, and transunion.com and request a freeze at each. It does not affect your credit score and can be temporarily lifted when you apply for legitimate credit.

2. Turn on two-step verification for email and banking

Free. Takes about 5 minutes per account.

Wondering if your current financial protections are keeping pace with today’s fraud tactics? Schedule a conversation with our team to discuss your specific situation and explore personalized strategies for safeguarding what you’ve built. We’re here to help you and your family stay a step ahead.

Your email account is the key to every financial account that uses it for password recovery. Two-step verification adds a second layer so a stolen password alone is not enough to get in. In your email and banking apps, go to Settings, then Security, and look for two-step verification or two-factor authentication.

Turn it on. Both apps will walk you through setup. CISA recommends this as a foundational security measure.

3. Set up bank transaction alerts

Usually free. Takes about 3 minutes.

In your banking app, go to settings or notifications and set up an alert for any transaction over a dollar amount you choose. You will see unusual activity as it happens, giving you a narrow window to flag something before more damage occurs. Most major banks offer this at no cost.

4. Use different passwords for banking and email than everywhere else

Free. Takes about 5 minutes.

If your banking or email password matches one you use on any other website, a data breach at that site puts your financial accounts at risk. Keep your banking and email passwords unique. You do not need special software for this. Write them down somewhere secure if that helps you keep them straight.

A note on paid monitoring services

Many people subscribe to paid identity monitoring services. These can be useful for detecting existing fraud, but most of them primarily alert you after a change has already been made to your accounts or credit. The CFPB is direct on this point: a free credit freeze provides more protection against new-account fraud than paid monitoring.

If you have a paid service, keep it as a secondary layer. Do the four free steps first.

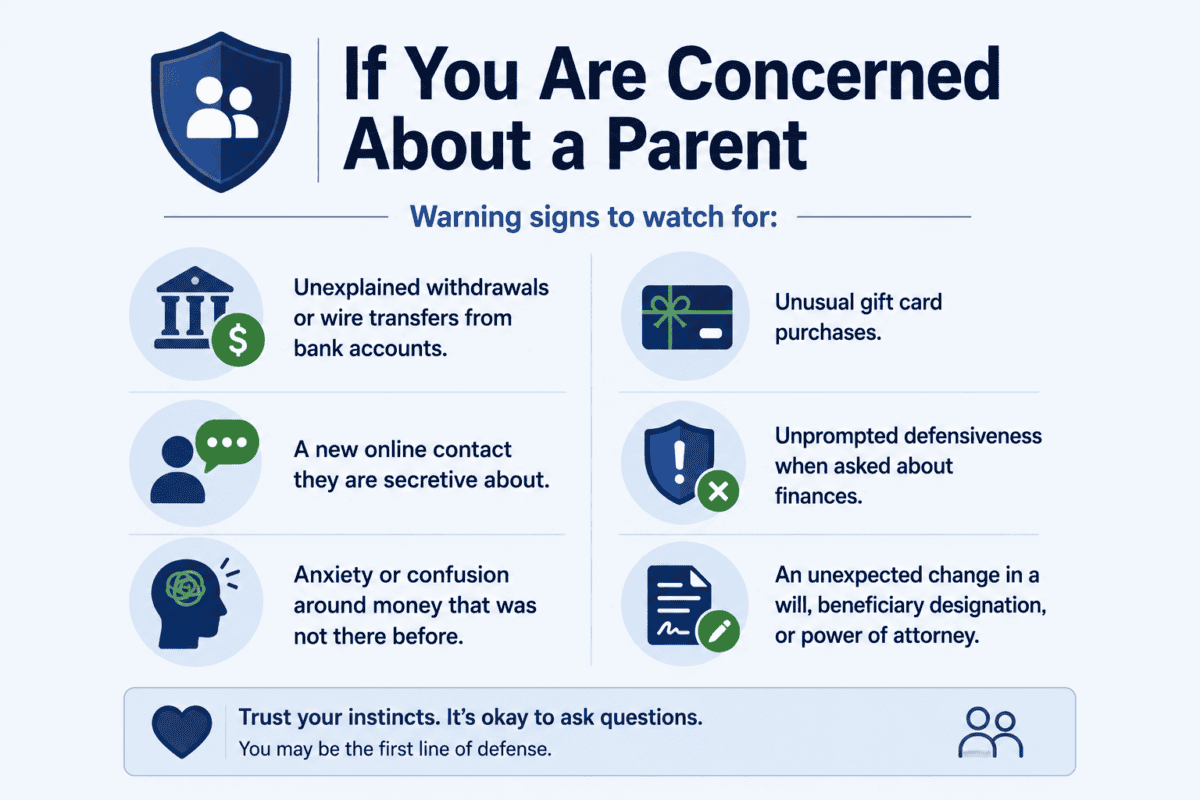

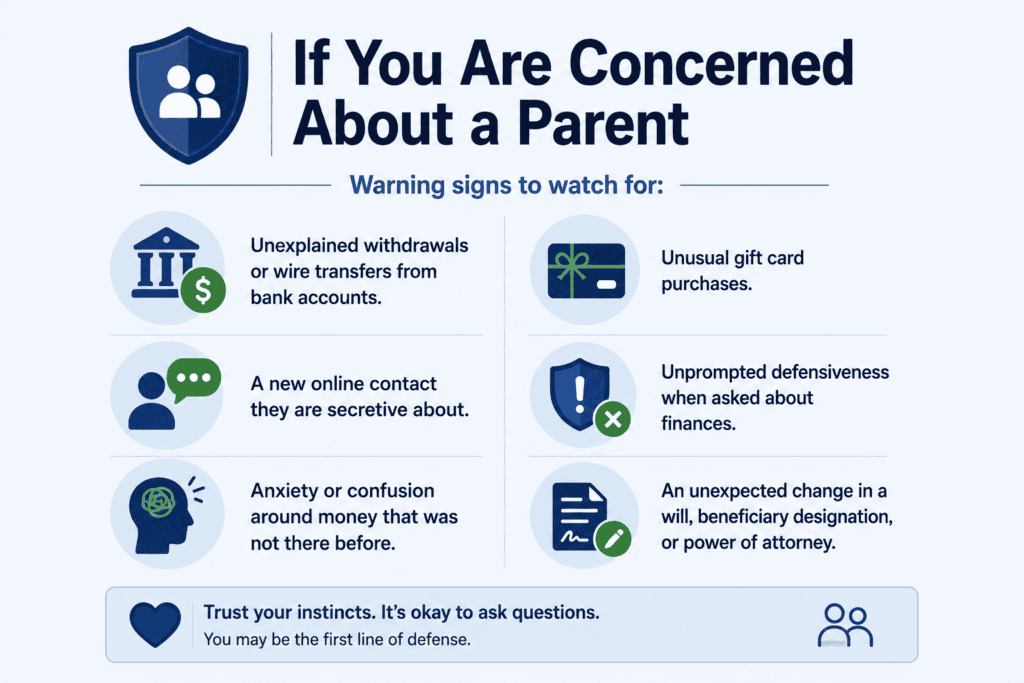

If You Are Concerned About a Parent

Many readers are navigating this from two directions at once. They are protecting their own finances and also watching for warning signs in a parent who may be more exposed. Social isolation, which often increases after retirement or the death of a spouse, is a documented risk factor for fraud vulnerability. The FTC found that adults 80 and older were disproportionately represented among victims of tech support and government impersonation scams.

Warning signs to watch for: Unexplained withdrawals or wire transfers from bank accounts. Unusual gift card purchases. A new online contact they are secretive about.

Unprompted defensiveness when asked about finances. Anxiety or confusion around money that was not there before. An unexpected change in a will, beneficiary designation, or power of attorney.

How to have the code word conversation: Keep it practical and non-alarmist. Something like: “I’ve been reading about phone scams that use AI to clone people’s voices. Can we set up a code word for our family so we can verify it is really each other during an emergency?” Most parents understand immediately and are glad to do it.

If you believe a parent is currently being victimized: Contact Adult Protective Services in their state. APS investigates financial exploitation of older and vulnerable adults and can intervene before more damage occurs. The Eldercare Locator (1-800-677-1116 or eldercare.acl.gov) connects you to local APS and other services. If money has already moved, call their bank immediately and file at IC3.gov the same day.

If Something Goes Wrong: Act the Same Day

The FBI’s Recovery Asset Team reports a 66 percent success rate at recovering fraudulent wire transfers when notified within hours. That rate drops significantly after the first day. Every step below can be completed the same day something is discovered.

Step 1: Stop all contact with the scammer

Do not respond, negotiate, or attempt to recover funds directly.

Step 2: Call your bank on the number on your card

Ask for the fraud department. Request an immediate block, recall, or reversal. Document the time and the representative’s name.

Step 3: File at IC3.gov and ReportFraud.ftc.gov

For wire transfers and cryptocurrency, file at IC3.gov with full transaction details immediately. For all fraud types, report to the FTC at ReportFraud.ftc.gov.

Step 4: Freeze your credit at all three bureaus

Free at equifax.com, experian.com, and transunion.com. Stops new accounts from being opened in your name while the fraud is being addressed.

Step 5: Call AARP Fraud Watch Network at 877-908-3360

Available to anyone regardless of AARP membership. They help navigate next steps and connect you to additional recovery resources.

One critical caution: After a fraud, expect a second contact from someone claiming to recover your money for a fee. The FTC and FBI both document this pattern. Anyone offering to retrieve stolen funds for payment is very likely running the second scheme.

Resources

These are free, government-operated, or non-profit resources. None of them requires an attorney or a paid service to access.

Reporting fraud

IC3.gov: FBI Internet Crime Complaint Center. Use for wire fraud, cryptocurrency, business email compromise, and investment fraud.

ReportFraud.ftc.gov: FTC fraud reporting. Use for all fraud types.

IdentityTheft.gov: FTC identity theft recovery. Creates a personalized recovery plan with step-by-step guidance.

oig.ssa.gov/report-fraud or 1-800-269-0271: Report Social Security impersonation.

phishing@irs.gov: Report IRS impersonation emails.

Verifying investments

investor.gov: SEC investor education and firm verification.

brokercheck.finra.org: FINRA BrokerCheck. Verify any investment professional or firm.

sec.gov/tcr: SEC Investor Complaint Center. Report investment fraud to the SEC.

Support and helplines

AARP Fraud Watch Network: 877-908-3360: Free helpline, available to anyone. Guidance on what happened and what to do next.

National Elder Fraud Hotline: 1-833-FRAUD-11 (1-833-372-8311): Operated by the U.S. Department of Justice. Free, confidential support for older adults and their families.

Eldercare Locator: 1-800-677-1116 or eldercare.acl.gov: Connects to Adult Protective Services and local resources in your area.

Credit freezes (free by law)

Equifax: equifax.com/personal/credit-report-services/credit-freeze

Experian: experian.com/freeze/center.html

TransUnion: transunion.com/credit-freeze

“None of these defenses requires technical expertise. The code word takes ten minutes and a piece of paper. The credit freeze takes twenty minutes and three free website visits.

The callback rule requires only the knowledge that legitimate institutions do not ask you to move money to protect it. The structure that protects against most active fraud schemes can be in place before the end of today.”

The Family Fraud Response Protocol, available as a free resource, brings this into a single printed page designed to be kept with estate documents and shared with family members. It includes the code word section, the response sequence, and the key contact numbers in one place.

If something here matches a situation you are currently dealing with, the most important step is the first one: call your bank and file at IC3.gov the same day. Time is the one variable that cannot be recovered once it is gone.

Curious how to help an aging parent put these defenses in place? Reach out to discover approaches tailored to families navigating fraud risks at every stage of life. A brief conversation could be the most valuable ten minutes you spend this week.

Questions about where your plan stands?

A complimentary conversation is available at no obligation.

We can review which of these defenses are in place and help build the ones that are not.

Schedule a Complimentary Conversation →

Langan Financial Group | 717-288-1880 | 1863 Center St., Camp Hill, PA 17011

This article is for educational and informational purposes only and does not constitute investment, tax, legal, or consumer protection advice. Individual results will vary. Defensive measures described may reduce fraud risk but do not guarantee prevention of all fraud or losses.

FBI IC3 2024 average loss of $83,000 for adults 60 and older sourced from FBI Internet Crime Complaint Center 2024 Annual Report. FTC government impersonation statistics and gift card payment method data reflect FTC Consumer Sentinel Network 2025 data. FTC text-based fraud loss of $470 million reflects FTC data for calendar year 2024.

Social media fraud loss of $2.1 billion reflects FTC 2025 Consumer Sentinel Network data. FBI 2025 BEC and tech support loss figures sourced from FBI IC3 2025 Annual Report. Hiya deepfake call statistic sourced from Hiya State of the Call 2026.

CFPB credit freeze guidance reflects published CFPB consumer advisory materials current as of 2026. CISA MFA guidance sourced from CISA Secure Our World program. FBI Recovery Asset Team 66 percent success rate reflects the FBI’s own reported figures; individual outcomes are not guaranteed and depend on the speed of reporting and cooperation of receiving financial institutions.

FTC older adult disproportionate tech support victimization reflects FTC Annual Report to Congress on Actions to Protect Older Adults, December 2025. IC3.gov, ReportFraud.ftc.gov, IdentityTheft.gov, AARP Fraud Watch Network (877-908-3360), National Elder Fraud Hotline (1-833-372-8311), and Eldercare Locator (1-800-677-1116) are third-party resources provided for informational purposes only; Langan Financial Group does not control or guarantee their availability or the content of those resources. investor.gov is a resource of the U.S.

Securities and Exchange Commission. FINRA BrokerCheck is a resource of the Financial Industry Regulatory Authority. Adult Protective Services availability and services vary by state.

Please consult qualified financial, legal, and consumer protection professionals before making any financial decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser.

Langan Financial Group and Cambridge are not affiliated.